Hire by Technology

SERVICES

When problems arise or a new product is developed, it’s not uncommon for business leaders to suggest big consulting firms, since they have an industry reputation and a long client list.

While consulting firms may advise on strategy, they do not provide software development services themselves, and an overwhelming majority of fintech engineering problems are execution problems, not enterprise transformation problems.

This doesn’t mean that the MBB firms (McKinsey, Bain, BCG), the Big Four (Deloitte, PwC, EY, KPMG), and Accenture are bad options. They are just priced and structured for an entirely different category of business case.

Let’s dive into the difference between Trio vs Big Consulting, and what growth-stage fintechs actually need.

If you need personalized advice or want developers on your team as soon as possible, schedule a complimentary consultation to compare options.

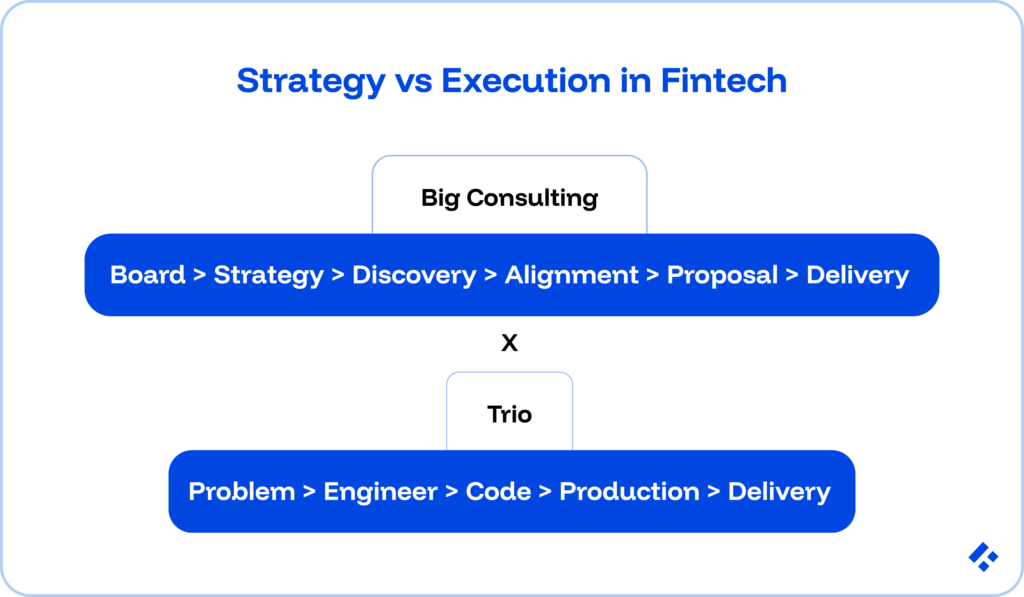

The term gets used loosely, so before getting straight into our comparison, let’s make sure we clarify what we are actually talking about.

We are a fintech-exclusive engineering partner providing nearshore staff augmentation and dedicated teams via LATAM engineers in Brazil, Argentina, Colombia, and Chile.

Our pool also provides some options for developers from Africa, in the event that you need an alternative time zone.

Every engineer that we have here at Trio gets vetted for domain-specific experience in the financial services industry. That includes things like KYC/AML, payment rails, SOC 2, PCI DSS, and core banking APIs.

Since the vetting has already been done, all we need to do is match you with the right people. Engagements start in days, not months.

Taking advantage of offshore and nearshore cost-of-living rates, our prices range between $40–$90/hr for senior fintech engineers. No discovery fees. No vendor PM layer between you and the engineers.

The fundamental difference between Trio and big consulting firms is that the latter get paid for advice and project delivery.

Trio gets paid for engineering execution.

Related Reading: Fintech Recruiting Agency Alternatives

Cost is a massive factor, but timeline may ultimately matter more, and tends to get less scrutiny up front.

A realistic big consulting engagement timeline for a senior fintech build looks like this:

These increased timelines simply reflect the structural reality of how large consulting engagements work. Multiple stakeholder reviews, procurement cycles, and discovery billing are features of the enterprise consulting model, built for clients who can absorb them.

The Trio timeline works in an entirely different way:

If you are a growth-stage fintech or in the very early stages of building your financial application, the timing problem means big consulting isn’t an option, even if you have the funds available.

Launch timeframes and audit deadlines don’t allow for months of delay,

Consulting billing rates vary significantly by firm, seniority mix, project scope, and client relationship history.

It’s difficult to give an exact value for cost, but we can estimate based on market practice benchmarks that we see pretty consistently.

A big reason for these high prices is that you essentially need to cover brand, bench, infrastructure, training overhead, and margin.

What you end up getting is likely a team that is partly composed of the firm's most experienced partners and delivery staff who are junior.

The easiest way to compare Trio vs. Big Consulting is to look at a real example. Here is a table covering a scenario where a fintech needs three senior engineers for 6 months.

| Engagement Type | Setup Cost | Monthly Cost | 6-Month Total |

| Big Four implementation team | $75K–$150K (discovery) | $100K–$200K | $675K–$1.35M |

| McKinsey advisory engagement | $500K minimum | N/A (not execution) | $500K+ (no code written) |

| Trio (LATAM nearshore staff augmentation) | $0 | $21K–$42K/month (3 engineers) | $126K–$252K |

Most readers assume big consulting wins on security by default. The sheer number of employees, combined with a global risk practice and certifications that cover entire industries, signals amazing security.

But sometimes you need to think more practically.

Which partner will produce engineers whose coding practices, data access patterns, and compliance documentation standards protect my fintech product's actual security posture?

Every engineer in Trio's bench gets screened for actual hands-on exposure to PCI DSS implementation, SOC 2 controls, or KYC/AML system design, not just general security awareness.

Our engineers work directly in your tools and repositories from day one, meaning compliance documentation lives in your environment regardless of what happens to the engagement.

And, since these employees are often full-time at Trio, with a 95% developer retention rate, even if you decide to scale your team down, it is likely that you will be able to access the same people later if you need them.

Access controls, environment separation, and incident escalation protocols get documented at onboarding.

Related Reading: In-House vs Staff Augmentation for Fintech

There are definitely some scenarios where Deloitte, McKinsey, or BCG is genuinely the better choice. Some of these scenarios include:

Not sure what the right fit is for your company? Consider this decision framework to help you make an informed decision.

| Your Situation | Right Partner |

| Need engineers in your sprint within 1 week | Trio |

| Pre-IPO, Big Four audit required by underwriters | Big Four (Deloitte, PwC, EY, KPMG) |

| 3 engineers needed for 6-month compliance build | Trio |

| Enterprise core banking modernization, $100M+ program | Accenture or Deloitte |

| Regulatory strategy before the SEC examination | Oliver Wyman / Deloitte Risk |

| Post-funding scale-up, 5–15 engineers needed | Trio (nearshore LATAM) |

| M&A strategy, board-level transformation roadmap | McKinsey / BCG |

| KYC flow needs to be SOC 2 auditable in 8 weeks | Trio |

| $500K+ strategy engagement with 12-month timeline | Big consulting firm |

| Fintech engineering execution at 40–60% below US rates | Trio |

In the most basic form, the pattern boils down to the fact that big consulting firms solve problems at the strategic and institutional governance level. Trio solves problems at the engineering execution level.

Trio and big consulting serve two entirely different purposes. Choosing the wrong one can lead to massive issues down the line. The question is whether the problem you're solving calls for what they're actually selling.

For growth-stage fintechs building and scaling products, the needs tend to look specific: engineers who are familiar with the industry and have transparent rates.

If you are ready to connect with those developers and get someone who can start producing real code in the next 3-5 days, book a decision call.

When you compare Trio and Deloitte for fintech development, you quickly realize they address different problems. Deloitte handles enterprise transformation and regulatory advisory; Trio handles engineering execution.

Yes, Trio is significantly cheaper than Accenture for fintech projects. Accenture's blended senior fintech engagement rate runs $2,000–$4,500/day; Trio's LATAM nearshore engineers cost $7,000–$14,000/month per engineer.

You should use McKinsey and BCG when you need board-level strategy, M&A advisory, regulatory positioning, or institutional transformation, and you should use Trio for engineering execution.

Compared to big consulting firms, instead of just providing institutional governance and audit services, Trio vets every engineer for fintech-specific security experience (PCI DSS, SOC 2 controls, KYC/AML), conducts background checks, enforces access controls, and keeps compliance documentation in the client's own tools.

Yes, Trio and big consulting firms can work together on the same fintech project. A McKinsey or Oliver Wyman engagement might define the regulatory strategy or product roadmap, while Trio engineers handle the actual build.