Hire by Technology

SERVICES

Before signing with a fintech outsourcing partner, you need to evaluate their fintech domain knowledge, IP ownership, data security, engineer continuity, regulatory change response, incident accountability, and SLA enforceability in fintech contexts.

Most fintech outsourcing partnerships fail because of things that weren't in the contract.

We often see issues related to a key engineer who leaves mid-project and takes their architectural knowledge, a data security incident where responsibility is unclear, IP ownership that becomes disputed because the contract used boilerplate language, or similar issues that could have been prevented.

None of these is unusual. Every one of them is preventable with the right questions asked before signing.

Let’s look at some different questions to ask a fintech outsourcing partner before you sign. These questions have been split into the seven categories we have mentioned to help you assess potential candidates systematically.

At Trio, we have acted as a partner for several financial technology firms, many of which have partnered with other companies before and made mistakes that led to less-than-ideal results.

If you want fintech developers who are guaranteed to have the right experience and who understand the unique nuances that come along with developing financial applications, request talent.

"We have fintech experience" covers a wide spectrum, including non-fintech development that happened to be for fintech firms, like building marketing websites.

A standard portfolio review won't always tell you which one you're getting.

The risk of misjudging this means you need to train an engineer up in things like regulatory compliance, which can take several weeks. If you don’t notice in time, you run the risk of developers making mistakes that might show up in audits later.

"Describe a specific project where your team made an architectural decision because of a compliance requirement. Not a performance requirement, and not a product requirement. What was the requirement, what decision did you make, and what would have happened if you hadn't?"

This question cannot be answered well by a team that has built fintech-adjacent software.

If teams do have production fintech experience, you can expect answers related to removing card data from debug logs, determining PCI DSS scope during architecture planning, and building idempotency keys client-side rather than server-side to reduce double-charge risk.

Specificity here is what you need to look for.

"Which fintech regulatory frameworks have your engineers worked under? Name the engineers on your current team with PCI DSS implementation experience. Who has built KYC/AML workflows?"

Here, you need to look for named frameworks, named engineers, specific implementation decisions made because of those frameworks, and reference clients in regulated financial verticals.

A generic answer is a major red flag. "We're familiar with compliance requirements and follow all applicable regulations," can’t be verified, and signals that no one on the team has implemented fintech compliance in production.

Also watch for: "our compliance team reviews all work.”

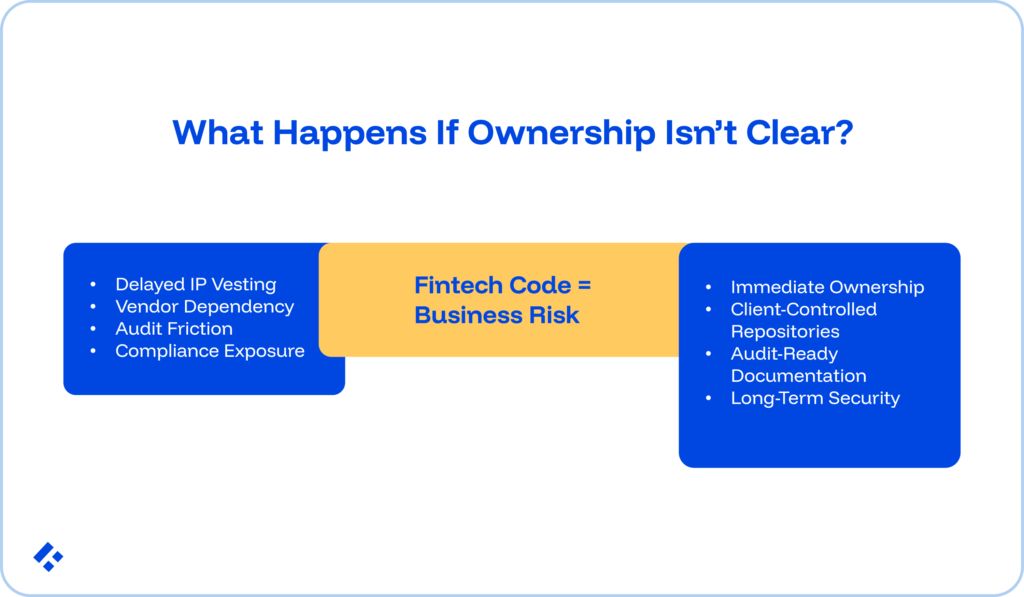

In fintech, the stakes of getting IP ownership wrong are considerably higher than in generic software development.

Your KYC state machine, your payment processing system, and your ledger infrastructure are all representative of your compliance posture, your banking partner relationships, and your regulatory standing.

If IP ownership turns out to be an issue later, you could struggle with major compliance issues.

"Under your standard contract, when does IP ownership of code vest? What happens to IP ownership if we terminate the engagement mid-project?"

The only option is that IP vests immediately upon creation and belongs to the client from the moment it is written.

If it only bests at final payment, your partner ends up with a lot of leverage, and if they leave mid-project, you are going to run into issues.

"Does your standard contract include any residual knowledge or background IP carve-outs? If so, what exactly do those cover, and how do they interact with the fintech-specific code your team writes?"

Residual knowledge clauses also let the partner retain and reuse knowledge, techniques, or approaches developed during the engagement.

In fintech, general approaches can overlap dangerously with proprietary compliance architecture. If there is this kind of clause, you need to make sure that it is very specific in what it covers.

"If a regulatory audit requires us to produce all code, documentation, and commit history within 48 hours, can you produce that immediately?"

Affirmation here is the only option, too.

When an outsourced engineer accesses your production database to debug a payment issue, they enter your PCI DSS cardholder data environment.

You can’t have them doing anything that will take data out of your controlled environment.

Some of the most common issues we have seen are when a logging configuration error puts a customer name and transaction amount into a shared log aggregator, which means that PII has potentially breached GDPR data residency requirements.

"What controls prevent your engineers from copying production PII or card data to a local machine or personal cloud storage? What does your production access approval and audit log process look like?"

What you need the partner to do here is to describe specific technical controls.

Common controls include production access that requires explicit client approval for each request, all production access creates an immutable audit log, test environments that use synthetic data by default, and alerts that are triggered when data is transferred outside approved systems.

"Your engineers are located in [country]. Does their access to our EU customer data comply with GDPR international transfer requirements? What legal mechanism governs that transfer?"

This is important to ask, as you may need Standard Contractual Clauses or another legal transfer mechanism.

Look for answers that indicate the partner knows what mechanism applies.

"Can you produce your most recent SOC 2 Type II report or ISO 27001 certificate today? What was the observation period covered?"

They need to provide actual documentation here. For SOC 2 Type II, verify the observation period covers at least six months, and the report is less than twelve months old.

"What is your incident response process if one of your engineers causes a data breach in our systems? What are your breach notification obligations to us, and within what timeframe?"

Here, you’ll want a specific incident response plan that includes breach notification within 24–48 hours of detection.

We have already mentioned how an engineer who has built your compliance systems takes that knowledge with them when they leave.

The reality here is that, no matter how diligent your developers try to be, it is impossible to get all your knowledge from a git history or the documentation. There is a lot of regulatory context that shapes decisions.

"What is your engineer attrition rate on client engagements specifically? Do engineers rotate between clients on short assignments, or do they commit to a single client for the engagement duration?"

Ask for the specific number. High rotation or short assignment cycles are one of the largest institutional knowledge risks that you’ll face when considering outsourced fintech development.

"If the engineer primarily responsible for our payment system or KYC implementation leaves mid-engagement, what does your knowledge transfer and replacement process look like? What is the contractual replacement timeline?"

The answer should include things like documented knowledge transfer requirements before any engineer departs an engagement, a specific handoff process, a replacement timeline expressed in days, and a contractual obligation to maintain continuity. "As soon as possible" is not a timeline.

"What prevents a departing engineer from using knowledge of our financial system architecture at a competitor engagement?"

Specific confidentiality provisions covering financial system architecture knowledge post-engagement are essential here.

Fintech regulations change on specific timelines that don't adjust for anybody.

DORA, for example, took effect in January 2025. PCI DSS 4.0 introduced requirements with a March 2025 compliance deadline.

Requirements change all the time, and your systems need to be designed to meet those requirements going forward, without a full redesign. This responsibility falls on you, even if you employ an outsourcing partner.

Active regulatory awareness is a major indicator of whether or not they will set you up for success.

"How does your team track regulatory changes that affect fintech products in production? Give me a specific example of a regulatory change you flagged to a client proactively before it affected their production system."

A partner with genuine ongoing fintech regulatory awareness should be able to give you a specific example, like a PCI DSS 4.0 requirement flagged before the deadline, a DORA implementation question raised ahead of the effective date, etc.

We’ve noticed that partners without awareness tend to describe a general monitoring process without a single concrete example.

"If a regulatory change requires modifications to the code your team built, is that remediation in scope for ongoing support, or does it require a new engagement? Who bears the cost?"

The answer here needs to be that there is a potential for adjusting scope, and the partner needs to be the one looking for changes.

The gap between what an outsourcing partner's sales team promises and what their standard contract actually commits to tends to be wider in fintech than in general software development. You need to make sure that you are careful and perhaps even negotiate the terms.

"Will your contract include a commitment to support a compliance audit or regulatory examination? Specifically, can you commit to providing code documentation, commit history, and access to engineers for audit interviews within a defined timeframe?"

Regulators examining your payment system may want to speak with the engineers who built it. If those engineers work for your outsourcing partner, that cooperation requires a contractual basis.

"What are your SLA commitments for critical financial system incidents, especially for incidents involving data exposure, compliance violations, or payment processing failures? What are the remediation timelines, and what are the penalties for breach?"

Most outsourcing contracts express SLAs in uptime percentages and response-time hours.

In fintech, however, this requires specific commitments like notification within N hours of a data exposure, remediation plan within M hours, with financial penalties that reflect the actual regulatory and reputational cost of a compliance incident.

"What professional liability insurance do you carry, and what coverage level applies to fintech engagements?"

Ask for the specific coverage amount and policy terms. A partner building your payment infrastructure should carry E&O insurance at a level commensurate with the financial exposure of a failure.

Every outsourcing partner's reference list is curated. It’s only natural that the clients who agreed to be references had good enough experiences to agree.

The clients who terminated early, discovered compliance issues, or had data incidents are probably not on the list.

"Did this partner proactively identify a compliance requirement or security issue before you did? Can you describe a specific instance?"

Partners with genuine fintech domain expertise flag compliance issues before their clients surface them. Partners who are technically capable but domain-deficient wait to be told. A reference who can describe a specific proactive flag is a strong signal.

"Did you have any disagreement about IP ownership or what happened to data after the engagement ended? How was it resolved?"

A reference with a smooth IP experience answers this directly and quickly. A reference who hesitates or begins describing a resolution process is revealing something worth exploring further.

"If you had a security incident involving code this partner wrote, how did they respond? What was the notification timeline and their level of engagement in remediation?"

Even minor incidents like a misconfigured staging environment or a briefly exposed debug endpoint reveal how the partner behaves when something goes wrong, which is incredibly informative.

"Tell me about an engagement that ended earlier than planned or where the client wasn't fully satisfied. What happened and what did you learn?"

If they can’t give you an example of something that went wrong, chances are that they either lack a sufficient track record or aren't being candid.

Domain knowledge:

IP ownership:

Data security:

Engineer continuity:

Regulatory change:

Contract and SLA:

References:

When it comes to domain knowledge, we pre-vet our engineers for fintech domain competency across PCI DSS, KYC/AML, payment system idempotency, and regulatory framework awareness.

We also make sure that every developer is senior-level, with real-world production experience in similar projects, and that they have the skills and resources to be able to keep up with regulatory changes.

In terms of IP ownership, all custom code vests as client-owned from the moment it gets written. Our engineers work in your repositories, as if they were in-house developers, so there are no residual knowledge carve-outs.

Since our engineers are so familiar with industry best practices, they always work under your access controls. Production data access will require your approval and will create an audit log.

They also stick to strict incident notification periods.

We have also been able to maintain a 95% engineer retention rate and 97% placement success rate across client engagements.

Work is clearly outlined in the contract and SLA. We often provide monthly contracts with clear termination rights. No 12-month minimum like many other hiring firms.

You are also welcome to enquire about client references, including regulated fintechs across payment systems, KYC/AML infrastructure, and neobank builds.

For more information or to get started, book a discovery call.