Hire by Technology

SERVICES

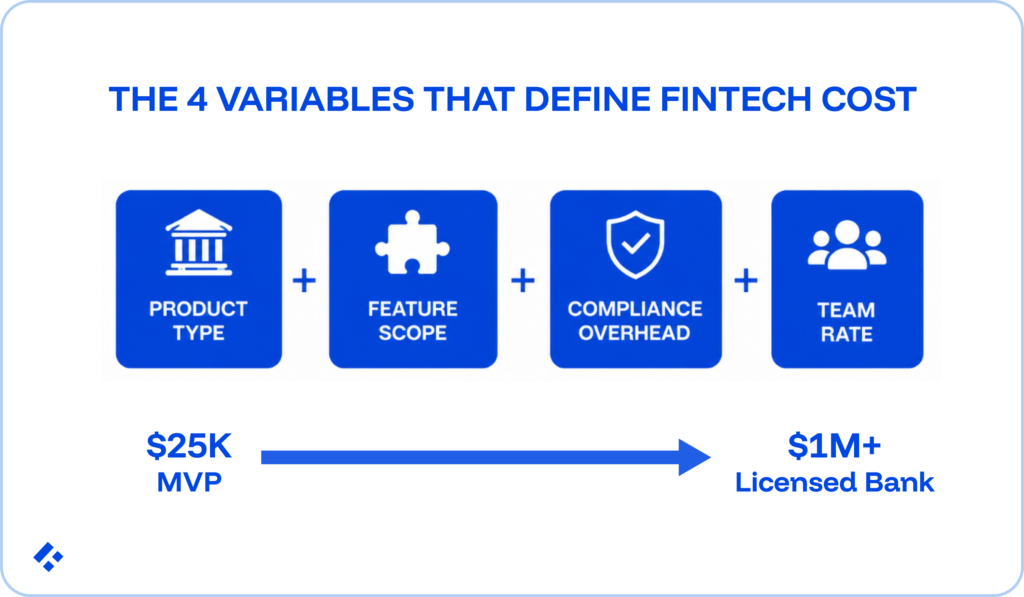

Fintech development cost is determined by product type and regulatory scope (sets the floor), feature complexity and integration count (the primary budget multiplier), team composition and geography (sets the rate), and compliance overhead (adds 30–40% to the engineering estimate).

Timelines can range from 3 months for an unregulated MVP to 18 months for a licensed digital bank.

You need to have a good understanding of the timeline and cost of your specific action, so you can plan a budget, hire a team, set a runway expectation, or present to a board. Without fairly accurate figures, you may run into issues, particularly if you are a smaller startup with limited funding and need to start creating income as quickly as possible.

What turns a fairly broad range into a number is methodology. You want a repeatable process that takes your specific product scope as input and produces a defensible estimate as output.

Let’s look at that methodology and all the factors that you need to account for. We will start from the bottom up, with the product-type baseline, applying feature multipliers, compliance overhead, team rate, and adjusting for timeline risk factors. This will provide an output that you can present in a planning meeting with the reasoning behind it.

If you want assistance estimating fintech development timelines and costs, we can assist. Our developers have several years of production fintech experience and have seen firsthand how certain factors affect budgets and development timelines.

Most fintech cost articles present ranges. For example, an MVP costs $50K–$150K, and a neobank costs $150K–$400K.

Any individual project in those categories will land somewhere within them, but sometimes these ranges span a 3× cost difference. This is the difference between determining whether or not a project is fundable, staffable, and executable with a given runway.

The methodology below produces a second number. While it may not be exact, the estimate is defensible, meaning each component can be explained, and the assumptions behind it can be validated.

Every fintech estimate starts with a product-type baseline that reflects the regulatory scope of the product.

Think of this as the minimum credible investment required to build a regulated financial product of that type, including the security, KYC/AML, and infrastructure standards required to handle live financial transactions.

| Product Type | Regulated MVP Floor | Production-Ready Range | Timeline Range |

| Personal finance/budgeting (no money movement) | $25K–$50K | $80K–$180K | 2–4 months |

| P2P payment/digital wallet (card acceptance, basic KYC) | $50K–$100K | $100K–$250K | 3–7 months |

| BNPL/consumer lending platform | $70K–$180K | $150K–$350K | 5–10 months |

| Investment/wealth management app | $100K–$250K | $200K–$450K | 6–12 months |

| Neobank/digital bank (BaaS-based, no own licence) | $80K–$200K | $200K–$400K | 6–14 months |

| Neobank/digital bank (own banking licence) | $250K+ | $500K–$1M+ | 14–24 months |

| B2B payments/embedded finance | $100K–$250K | $250K–$600K | 8–16 months |

Below the regulated MVP floor, the product cannot credibly implement the security, KYC, and infrastructure standards required for regulated financial operations, while the production-ready range represents a commercially viable product with full compliance, tested at scale.

Personal finance products usually display financial data via aggregation APIs without actually moving money.

The result is a dramatically lower compliance floor with no PCI DSS scope, no KYC/AML obligations, and no payment rail integration, drastically reducing compliance costs.

A banking licence adds regulatory capital requirements, compliance infrastructure specific to the licence type, and the operational overhead of being the regulated entity rather than operating under a BaaS sponsor's licence.

The cost and timeline are not feasible for most fintech startups, so they usually begin with a BaaS-based service and only pursue their own licence at Series B or beyond.

Once you have a product-type baseline, the feature scope determines where within the range your project lands. We see several categories consistently push fintech estimates toward the upper end:

Every third-party integration adds engineering scope. You need to work with the connection itself, and the additional error handling, webhook management, sandbox testing, production certification, and reconciliation infrastructure.

From what we have seen, the first PSP integration typically adds $15K–$30K of engineering work, including fault-tolerant retry logic and idempotency handling. Each additional PSP adds roughly half the cost of the first, since the shared infrastructure is already built.

Multi-rail payment support, in contrast, roughly doubles the payment infrastructure scope.

Native iOS and Android increases cost by 30–40% over a single-platform build. On the other hand, React Native and Flutter reduce that premium by 20–30% versus full native dual-platform development.

For fintech-specific native bridging where you may require biometrics, NFC tap-to-pay, and hardware security modules, native code is often required even in a cross-platform architecture, which narrows the cost gap.

Multi-currency support requires conversion logic, settlement currency tracking, FX rate management, and multi-currency reconciliation.

Cross-border rails each require their own integration, compliance review, and settlement logic.

From experience, you can estimate $30K–$80K incremental for multi-currency support, depending on currency count and rails involved.

Real-time transaction feeds, live fraud scoring, and instant balance updates are all real-time features that require streaming infrastructure (WebSocket, Kafka, or equivalent).

This infrastructure increases both infrastructure cost and engineering complexity. Our recommendation is to estimate 15–25% incremental cost for real-time versus batch-processed equivalents.

Fraud detection models, credit scoring, AI-powered financial insights, and embedded chatbots each add model training, serving infrastructure, explainability engineering, and ongoing monitoring.

For models that influence regulated financial decisions, SR 11-7 compliant governance documentation adds further scope.

You should estimate $30K–$80K for a basic ML feature with compliance-appropriate governance.

Compliance and security engineering is an infrastructure layer that governs how every feature gets built.

We consistently see this underestimated or excluded from initial fintech development estimates, but compliance alone often accounts for 25–40% of total project cost.

A good practical rule is to take the total engineering estimate from Steps 1 and 2.

Multiply by 1.35 to produce the compliance-adjusted engineering estimate. If the product touches card data, operates in EU markets under DORA or GDPR, or deploys AI/ML for regulated decisions, apply 1.40 rather than 1.35.

An accurate estimate will require you to convert engineering time into an hourly rate. It is simplest to consider the blended hourly rate of the engineering team multiplied by the estimated hours.

Rate benchmarks by geography (2026):

| Region | Senior Engineer Rate | Mid-Level Rate | Typical Blended Rate |

| US domestic (in-house or onshore) | $120–$200/hr | $80–$130/hr | $150–$180/hr |

| LATAM nearshore (Trio) | $60–$80/hr | $40–$60/hr | $50–$70/hr |

| Eastern Europe | $55–$75/hr | $35–$55/hr | $50–$70/hr |

| India / Southeast Asia (offshore) | $25–$45/hr | $15–$30/hr | $25–$40/hr |

Fintech specialists with production compliance experience often charge a premium of as much as 10–15% above standard software engineering rates across all regions. This can be attributed to the domain knowledge component.

Total build cost = engineering hours × blended rate

For a 1,200-hour project (roughly 30 engineer-weeks is typical for a payment app MVP):

The LATAM nearshore rate at $40–$80/hr presents incredible cost savings due to the efficiency and timezone-productivity overlap, which are simultaneously optimised.

Offshore rates can appear 40–50% cheaper, but they are often not the most cost-effective, as you will need to deal with the productivity overhead of timezone-driven decision latency, rework rates, and compliance domain gaps.

In reality, this narrows the actual cost gap to something closer to 15–25% once modelled honestly.

Related Reading: Fintech Outsourcing Cost Guide

An engineering estimate in hours does not convert directly to calendar weeks, because fintech projects carry specific calendar multipliers that you will need to account for.

Calendar weeks = total engineering hours ÷ (team size × productive hours per engineer per week)

In fintech, productive hours per engineer per week run 30–32 rather than 40.

Sprint ceremonies, code reviews, and coordination consume 4–6 hours, while compliance-related activities like security reviews, documentation updates, and regulatory testing consume roughly 3–5 hours per week.

To account for this in your estimates, your sprint velocity calculations should apply a 20–25% compliance overhead reduction to raw available hours.

Fintech projects have external dependencies that add calendar time without adding engineering hours. These need scheduling, not estimating, and they need to start on day one:

| External Dependency | Typical Lead Time |

| KYC provider sandbox (Jumio, Onfido, Veriff) | 1–3 business days |

| PSP/BaaS sandbox provisioning | 3–8 weeks |

| Penetration test scheduling | 4–6 weeks |

| PCI DSS QSA engagement | 6–14 weeks total |

| Banking partner compliance review | 6–16 weeks |

| Card program approval (Visa/Mastercard) | 8–12 weeks after BIN |

We have estimated these standbox provisioning timelines from our own fintech development timeline research, as well as Gemba's 2026 BaaS launch analysis.

If started on day one, these dependencies can run in parallel with engineering. However, if your teams begin them after engineering is complete, you can add them sequentially.

There are three common issues in estimations that we notice our clients making. Being aware of them can help you to avoid them.

Two fintech products with identical feature lists can cost twice as much depending on their architecture.

Building a custom payment processing infrastructure where Stripe or Adyen would serve the same function adds months and significant budget.

Many assume that the build cost is a one-time investment. However, recurring costs can exceed the build cost within 18 months.

Here are some estimates based on our findings:

| Recurring Cost Category | Typical Annual Range |

| API fees (KYC, fraud, banking data) | $24K–$96K/year |

| Cloud infrastructure and hosting | $24K–$120K/year |

| Compliance audits (PCI DSS, SOC 2) | $10K–$50K/year |

| Product maintenance (bug fixes, updates) | 15–20% of build cost/year |

| Regulatory updates (DORA, PCI DSS 4.0 changes) | $10K–$30K/year per significant change |

An engineering team without fintech domain experience requires 4–8 weeks to reach compliance-aware productive velocity.

This cost should appear as an explicit line item in any estimate that involves engineers without prior fintech experience.

Alongside a thorough understanding of the above-mentioned factors, you can apply this worksheet to your specific scope to produce a defensible number.

Step 1 — Product type baseline

Product type: _______________

Regulated MVP floor (from table): $___K

Target build tier (MVP / production-ready): ___

Step 2 — Feature multipliers

Integration count × $15K–$30K per PSP: $___K

Cross-platform premium (+30–40% if native dual): $___K

Multi-currency (+$30K–$80K): $___K

Real-time infrastructure (+15–25%): $___K

AI/ML features (+$30K–$80K per feature): $___K

Feature subtotal: $___K

Step 3 — Compliance overhead

Engineering total (Step 1 + Step 2): $___K

Compliance multiplier × 1.35

(or 1.40 if AI, EU markets, or card data): $___K

Compliance-adjusted total: $___K

Step 4 — Team rate

Engineering hours: ___hr

Blended hourly rate (by geography): $___/hr

Build cost: $___K

Step 5 — Timeline

Engineering weeks (hours ÷ 30–32 productive hrs/wk): ___wk

External dependency buffer

(sandbox, pen test, banking partner): +___wk

Total calendar timeline: ___months

Step 6 — Post-launch annual recurring

API fees + cloud + compliance + maintenance: $___K/year

Validation check: If your Step 4 total falls below the regulated MVP floor for your product type, either the feature scope is incomplete, or the compliance overhead is underestimated and should be revisited.

Let’s look at three different examples where the above methodology has been applied to create a defensible number.

Three staffing decisions carry the most impact on whether the estimate holds.

At Trio, we place pre-vetted senior fintech engineers with production experience in payment systems, KYC/AML, PCI DSS compliance architecture, and ledger engineering in 3–5 days.

These LATAM-based engineers go for $40–$80/hr, with no additional staffing costs.