Hire by Technology

SERVICES

Most fintech hiring processes screen for the wrong things, which leads to developers working on systems they really don’t have the skills for, and mistakes that may not be identified until critical moments, like regulatory audits.

Vetting fintech developers requires five domain-specific screening areas beyond standard technical assessment:

Let’s go over how to vet fintech developers in a structured way, addressing each of the domain-specific screening areas mentioned. We’ll cover specific questions, what a genuinely experienced answer sounds like, and the red flags that reveal domain gaps before they become production problems.

At Trio, we do all of this screening for you, so you can access these fintech specialists in as little as 3-5 days, instead of spending weeks or even months trying to find the right person for your financial application.

Standard technical screening, like coding challenges, system design interviews, and even behavioural questions, is a good starting point. They are more than enough to evaluate general engineering competence; however, the problem is that none of this evaluates fintech domain competence, because fintech domain competence doesn't surface in general software problems.

This means that you might miss fintech-specific knowledge or compliance gaps.

If these issues don’t show up in the pre-hiring vetting process, they inevitably show up when the developer starts writing fintech code. We often pick up on issues around 2–4 weeks in, when the first code review surfaces a data type error or a security review surfaces a PCI DSS scope problem that shouldn't exist. The cost at that point includes compliance review delays, architectural rework, and the timeline slippage.

And that’s if you catch the issue. If you miss it, you might run into issues during regulatory audits and might face massive fines as well as a loss in customer trust.

Storing monetary amounts as floating-point numbers (FLOAT, DOUBLE) creates rounding errors that compound at transaction volume. A FLOAT representation of 0.1 + 0.2 doesn't equal 0.3 in IEEE 754 arithmetic.

This doesn’t really matter if you are only dealing with a handful of transactions, but if you scale to millions, as most banks do, then it produces a reconciliation gap that triggers a finance team investigation and potentially draws regulatory attention.

Our senior engineers who have worked on a variety of production fintechs cite this as one of the first things they check when reviewing financial code from engineers new to the domain.

The screening question: "What data type would you use to store a monetary amount in a database, and what would you use in a JSON API response? Why?"

For the database, you are going to want them to answer NUMERIC or DECIMAL with defined precision and scale, because these are fixed-precision types that don't introduce rounding errors.

Alternatively, store in integer minor units (cents for USD) and convert at the display layer.

For the API response, you want them to mention a string, not a float. This is because floating-point serialisation and deserialisation across different languages and frameworks can introduce precision loss at the boundary.

The candidate should be able to explain why.

Follow-up questions you should ask here include, "Have you ever encountered a rounding error in a financial system? What caused it and how was it resolved?"

Engineers with genuine production experience give specific answers. Engineers who haven't built financial systems give theoretical responses about what they would do.

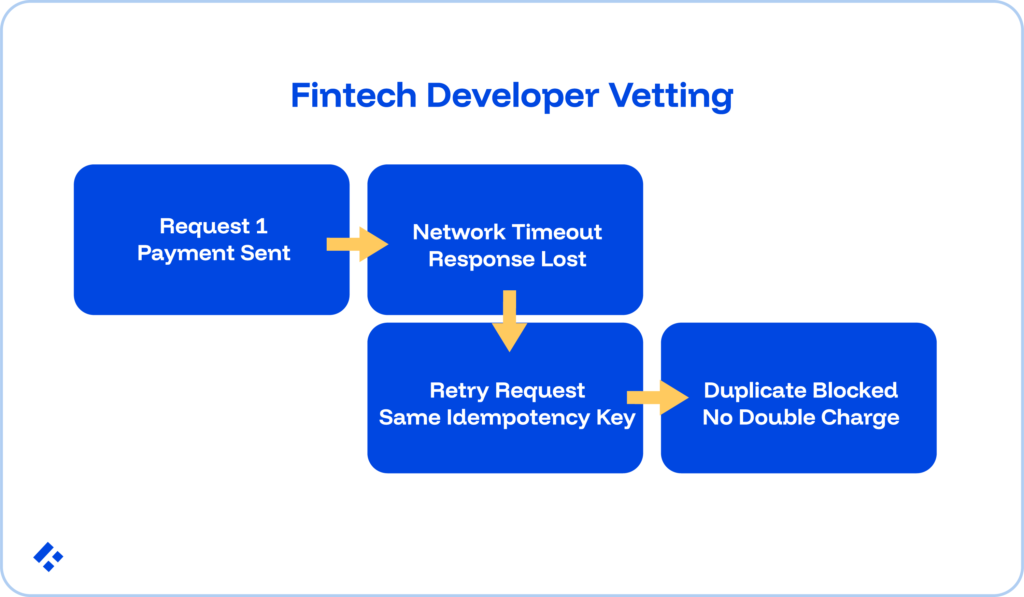

A user taps "Pay." The payment processes. The response gets lost in transit. The user taps "Pay" again.

Without idempotency enforcement, the payment processes twice, and the customer gets double-charged. This failure mode surfaces in production at every fintech that handles payments with engineers who understand idempotency but haven’t implemented it correctly.

It's the most common production incident in payment integration work by engineers new to the domain.

The screening question: "Walk me through how you'd implement idempotency for a payment endpoint. Where does the idempotency key come from, and how do you prevent a double charge if a network timeout occurs between the PSP confirming a charge and your database recording it?"

The idempotency key comes from the client, not the server. This means it is generated before the payment request fires.

If the server generates it and the response is lost, the client can't retry with the same key and has to generate a new one, which is what leads to a double payment.

The key applies at three layers:

It’s important that you probe your candidate to mention the write-ahead log gap.

This is where a window exists between the PSP confirming the charge and the database write completing. A production-grade solution uses a write-ahead record created before the PSP call, deleted only after the database write succeeds.

On recovery, unresolved write-ahead records trigger a PSP status query rather than a new charge attempt.

Follow-up questions you can ask here include, "What's the difference between a soft decline and a hard decline from a payment processor, and how does your retry strategy change for each?"

If your candidate really has fintech experience, they will be able to distinguish these immediately.

Soft declines (insufficient funds, temporary issuer unavailability) retry with back of, while hard declines (stolen card, account closed) never retry automatically.

PCI DSS scope determines the complexity and cost of security certification.

If your engineer doesn't understand the scope, they will make implementation choices that expand it unnecessarily by logging raw card data in debug statements, placing non-payment services in the same network segment as card data, and using shared credentials across systems that touch cardholder data.

The screening question: "If your application uses Stripe Elements or Adyen's hosted payment fields for card data collection, what is your PCI DSS scope and why?"

Hosted payment pages or JavaScript libraries (Stripe Elements, Adyen Web Drop-in) mean that your cardholder data travels directly from the browser to the PSP's servers.

Your application never touches the raw card data.

This lets you qualify for SAQ A, the lightest compliance path, because the application doesn't store, process, or transmit cardholder data directly.

You should also make sure that the candidate understands how using PSP tokens for all subsequent operations (capture, refund, recurring billing) maintains this minimal scope.

A good follow-up question here would be something like, "What would change about your PCI scope if you decided to store card tokens in your own database rather than in the PSP's vault?"

The domain-experienced answer is that PSP tokens have no value outside the PSP relationship and are not cardholder data, so storing them in your own database doesn't significantly expand PCI scope.

KYC at a regulated fintech is not a form that calls a verification API and stores a verified boolean.

Instead, it's a stateful system with defined lifecycle states, regulated transition conditions, ongoing monitoring requirements, and EDD (Enhanced Due Diligence) triggers.

A developer who designs KYC as a simple verification form with a boolean flag produces a system that passes initial compliance review at low scale and fails under regulatory scrutiny as the customer base grows.

This is exactly the architectural failure behind the Monzo FCA fine (£21 million, July 2025).

The screening question: "Describe how you'd design the data model and state machine for KYC customer onboarding. What happens after a customer is initially verified?"

KYC needs a state machine, not a boolean. States should include at minimum: INITIATED, DOCUMENT_SUBMITTED, DOCUMENT_VERIFIED, LIVENESS_CHECK, SANCTIONS_SCREENING, RISK_SCORED, APPROVED, REJECTED, PENDING_EDD, SUSPENDED.

Your potential developer should understand that KYC is ongoing, not a one-time event. Initial verification is a state entry.

They also need to understand that a customer's risk classification can change based on transaction behaviour, and that change must trigger a state transition.

A good follow-up question here is, "What would cause a previously approved customer to re-enter a review state?"

Experienced answers are specific, while generic answers reveal theoretical rather than practical knowledge.

A fintech engineer doesn't need regulatory knowledge at a compliance officer's depth, but they do need to know which frameworks apply to the systems they're building, what those frameworks require at the engineering level, and when to escalate a decision.

An engineer who builds a credit decisioning model without knowing ECOA requires adverse action notice capability, or builds an EU payment product without knowing DORA applies to their third-party API dependencies, creates compliance gaps.

A candidate who responds to engineering-level regulatory questions with "our compliance team handles that" isn't operating at the seniority level the role requires.

The five domain screening areas above complement standard technical assessment rather than replace it. A complete fintech developer vetting process covers both layers.

Standard technical assessment (necessary but not sufficient):

Fintech domain screening (what distinguishes fintech-competent from fintech-adjacent):

If you are reviewing a candidate and notice that they struggle in two or more of the five domain areas, we recommend that they be treated as a general engineer.

This means you are going to have to invest in significant fintech onboarding before working independently on compliance-sensitive systems.

Mistake 1: Testing general coding ability and calling it fintech screening. LeetCode challenges test algorithmic thinking. Both matter for fintech roles, so you need to make sure that you are screening for both.

Mistake 2: Accepting "I've worked at a fintech company" as domain experience. A developer who built the marketing website for a fintech startup has not built payment systems.

Mistake 3: Asking regulatory questions that test memorisation rather than application. "What is PCI DSS?" tests awareness. "If I log the full card number in a debug statement during testing, what does that do to my PCI DSS scope?" tests the application.

Mistake 4: Not asking about failure modes. "What's the most common mistake you've seen in fintech payment integration code?" is one of the most revealing questions available. Engineers with production experience give specific, detailed answers.

Mistake 5: Treating compliance knowledge as optional for backend roles. Every backend engineer working on a fintech product touches compliance-sensitive systems eventually. Treating regulatory awareness as a nice-to-have for backend roles produces the architectural gaps that surface in compliance reviews.

Related Reading: Fintech Career Paths: Compliance, Jobs, and Roles

When a staffing partner claims to offer pre-vetted fintech developers, the claim only carries weight if the vetting covers the domain layers described above.

It is important that you make sure they are not just vetting for general engineering quality.

Here are three questions worth asking any staffing partner you are considering:

Trio's vetting covers all of the domain areas we have already spoken about, and is supplemented by reference checks that verify production fintech experience specifically.

Developers are then hand-picked based on your specific requirements, so they are guaranteed to have all the right skills, leading to a 3-5 day placement time, with easy replacement guaranteed, further minimizing your risk.