Hire by Technology

SERVICES

Fintech Super Apps: How Banking Gets Rebuilt Around Ecosystems

The idea of a single app handling all your financial needs once sounded far-fetched, but that is exactly where we are heading.

The fintech super app refers to a single platform that bundles a bunch of different financial services together. It brings payments, savings, credit, investing, and even lifestyle features together on one platform.

Some apps now even combine travel perks and credit-building tools alongside everyday banking, all without requiring the user to leave a single interface.

These models have already become popular in Asia, with amazing examples like Alipay and WeChat, so we can only assume that the United States and Europe won’t be far behind.

As banking and fintech companies race to build connected ecosystems that will become a defining point for the next decade of financial services, many opportunities are emerging.

Let's explore what makes super apps different, how they're transforming the fintech landscape, and what it takes to build one that customers actually trust.

If you need specialist fintech developers to advise on your own products, you're in the right place.

A super app works more like an ecosystem than a product.

Instead of offering one or two financial tools, a super app combines various financial services into a single platform where users can spend, save, invest, borrow, and pay bills without switching between multiple apps.

The difference between a super app and a traditional fintech app comes down to integration.

While most fintech apps serve a narrow function, such as digital payments or trading, super apps provide an all-in-one experience.

It needs to be well-designed so users can move naturally between services.

This complete offering could create an incredibly loyal customer base in theory. If they already trust you to keep their money in a digital wallet, users may be more inclined to trust you with their stock portfolio or their life insurance.

The challenge, though, is that combining various services creates real complexity.

Apps must maintain performance, meet financial regulations, and deliver consistent UX across a lot of moving parts. With a lot of different parts, there is a lot more than needs to be maintained, and if you don’t approach development correctly, a break in one system could affect others.

That's why fintech super apps tend to be designed around modular architectures and open APIs, letting developers integrate new functions without breaking what already works.

Most successful fintech super apps share a few defining characteristics.

It is very rare for a single company to have the resources to develop all the different aspects of a super app. Instead, the ecosystem model depends on partnerships between banks, payment networks, and third-party service providers.

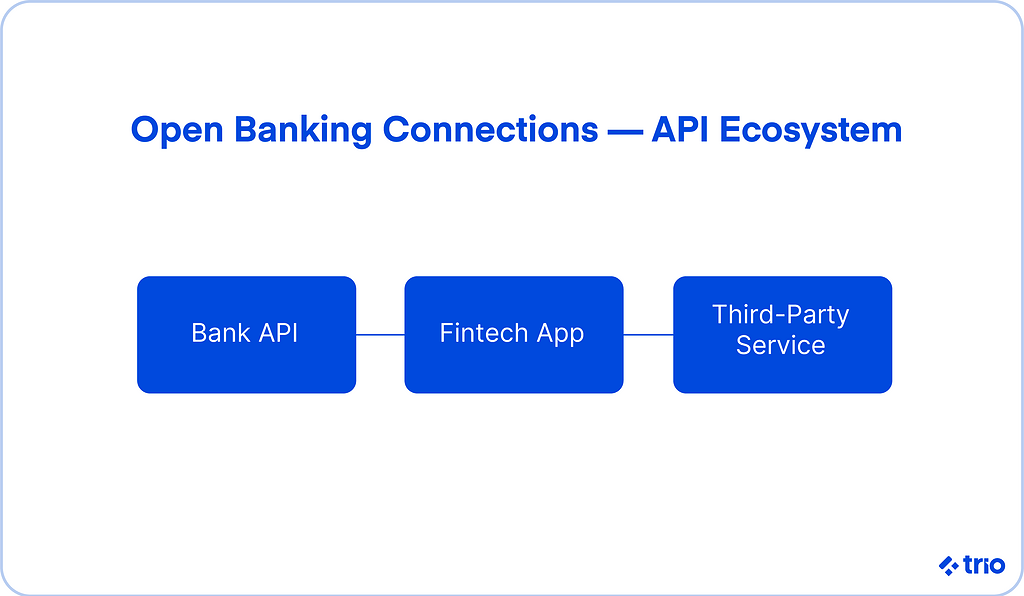

Open banking regulations in the EU and UK have accelerated this shift by requiring financial institutions to share data securely through APIs.

This has given rise to pre-integrated app ecosystems for open banking, where fintechs can connect financial and lifestyle services with everything from standard banking products to retail discounts and travel insurance within one platform, with very little development.

The result feels seamless for users, but it is powered by a network of specialized providers working in the background.

For fintech developers, building that ecosystem means balancing speed and security. API gateways must stay watertight while allowing third-party access.

At Trio, our fintech engineers often help clients design these integrations safely. By consulting with experts, you not only ensure security and regulatory compliance, but you also get industry insights into things like user expectations and real-time trends.

Designing a financial super app involves building an architecture that can adapt and scale as your user base grows or as you expand to other regions. You also want to focus on maintainability and the long-term ROI.

Let’s take a practical look at some of the primary considerations that go into designing a super app.

We’ve already discussed integration and the role it will play in super apps briefly.

Payments, lending, wealth management, and insurance must work together. APIs handle the connectivity, but orchestration is what makes it feel unified.

Embedded finance is another major factor to consider.

By partnering with traditional banks, fintech companies can offer credit, accounts, or savings products directly within their own platform, without needing to go through the process of getting licensed to offer these services on their own.

It's a mutually beneficial model as fintechs expand their service range, and more traditional banks gain digital distribution without building everything themselves.

You need skilled developers who understand both code and compliance. They need to understand what is truly at stake when dealing with people’s money and sensitive information, and need the experience to actually make informed decisions based on that knowledge.

If your team doesn’t have domain fluency, they might underestimate just how demanding integration across open banking APIs, regulatory frameworks, and diverse data sources can be.

Our developers have helped fintechs integrate complex financial systems securely and clean up messes constantly. It is more cost-effective to ensure that you have the right tech partner from the start, before you make mistakes that invite regulatory scrutiny or lose user trust.

Once the ecosystem goes live, keeping users engaged becomes the next challenge.

Many super apps use gamified loyalty programs and personalized dashboards with some sort of incentive.

In recent years, we’ve seen a rise in the use of AI-driven analytics to identify user patterns and offer timely nudges, like recommending an investment product right after a paycheck arrives.

But beyond clever engagement mechanics, long-term retention depends on credibility.

Apps that educate users through financial coaching tools or provide transparent insights into spending behavior tend to build stronger loyalty over time because users feel like you care and like you are ultimately on their side.

If your fintech super app runs on microservices, it is easy to use API gateways to integrate a variety of AI features related to security.

Fraud detection is one field we have seen AI used in more often. Machine learning models can analyze massive quantities of data almost instantaneously and make decisions based on the gained insights.

Stripe is just one example of a platform that does this very well, monitoring user behavior to detect anomalies.

As you integrate credit-related services, AI can also be used in risk scoring and underwriting, even automating the KYC process.

But AI also adds complexity as models might have security gaps, deal with data incorrectly, or even develop biases. It’s important to ensure that your AI, or any integration you are considering that utilizes AI, is not only ethical but also auditable.

Super apps are not new. The concept first took hold in Asia, where apps like WeChat and Alipay turned messaging tools into multi-service ecosystems.

It was only a matter of time before we saw a global shift.

Several factors appear to be driving the rise of fintech super apps at this particular moment.

Consumers expect digital platforms to work across needs as well as functions. Younger generations treat banking as a service, not an institution, and want financial tools that fit naturally into their digital lives.

We have already mentioned how open banking has also made integration far easier than it used to be, with regulations like PSD2 and PSD3 letting fintechs connect directly with banks, so users can manage multiple accounts through one interface.

Combine that with advances in mobile technology and faster cloud infrastructure, which can facilitate these kinds of apps, and it feels like a very natural progression.

It's also worth noting that traditional banking systems have been at a disadvantage for quite some time and appear to be reaching their limit.

Whether it is due to legacy software or bureaucratic chains that slow down decision-making, or a mixture of the two, many established financial institutions still struggle to meet user expectations around seamless digital experiences.

Alipay and WeChat became household names by offering everything from digital payments to loans, insurance, and lifestyle perks like travel savings programs that double as credit-building tools for underserved users.

In Latin America, apps like Nu (Nubank) and Mercado Pago have reshaped consumer finance by making it mobile-first and inclusive.

Europe and the U.S. are catching up. Revolut and Monzo have been expanding from single-product fintech apps to full-fledged financial super apps, each building its own ecosystem across a wide range of services.

What we can see is the formation of a global trend transforming fragmented fintech tools into genuinely connected financial platforms.

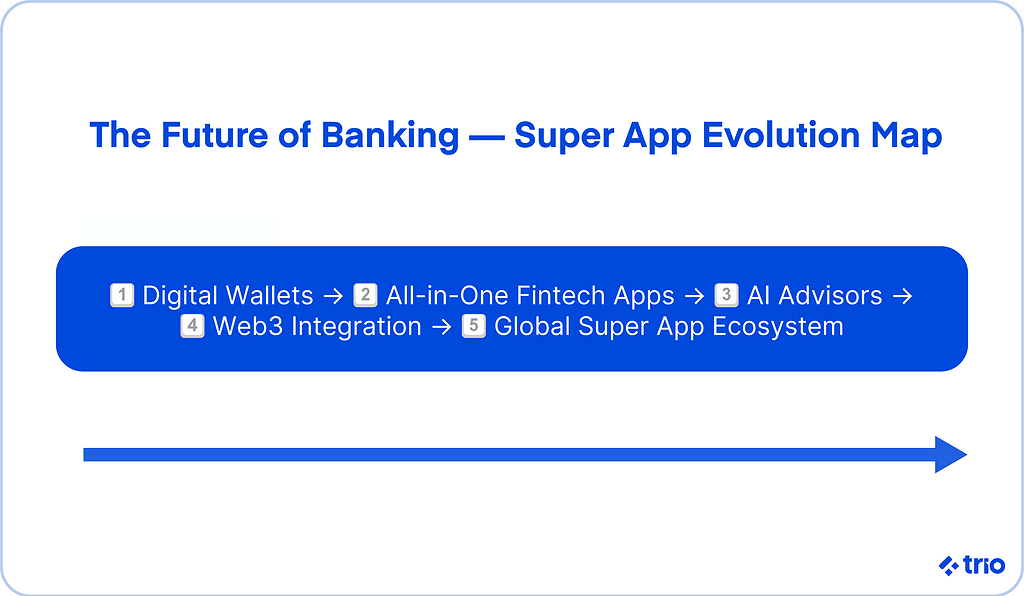

The future of financial services will likely be shaped by super apps.

As boundaries blur between financial and lifestyle platforms, we expect the next wave of competition to come from companies that manage to combine trust with service offerings.

We are already seeing more companies experiment with AI-powered personal financial advisors that act as virtual assistants that can forecast spending and recommend savings goals, so there is no reason super apps won’t utilize these as well.

Some AI-powered advisors can even negotiate recurring bills.

These tools have the potential to democratize financial planning, especially for younger users entering the financial system for the first time.

The next generation of super apps won't stop at finance. Many are branching into travel, retail, health, and entertainment. By integrating third-party services, they become daily lifestyle hubs that also handle financial transactions.

The super app model, once limited to fintech, appears to be becoming the blueprint for the broader digital economy.

A web3 super app, in its most developed form, would combine centralized financial services with decentralized infrastructure.

In other words, it would combine things like tokenized assets, blockchain-based identity, and decentralized lending, sitting alongside traditional accounts in one interface.

This is quite complex, so we expect adoption to be gradual.

But an eventual future of centralized and decentralized finance in the same platform, giving users access to both without needing to understand the underlying architecture, seems clear.

As super apps grow, so does regulatory attention.

Financial authorities will need to adapt to account for these changes, which means that fintechs will, in turn, need to make changes in order to stay compliant.

In Asia and Latin America, regulators are emphasizing interoperability and data sovereignty.

A super app operating across regions will have to manage multiple licenses and adhere to varied anti-money-laundering frameworks.

The fintech super app is changing the possibilities of what banking and financial services can be. One app for everything your users need.

For fintech companies, the opportunity is incredible. But you need the right fintech development talent on your team to make sure that your integration and architecture are not only secure, but also compliant.

At Trio, we help fintechs build scalable, secure ecosystems that can grow into tomorrow's financial super apps.

To find out more about hiring with us, request a consult!

A fintech super app is a single application that combines a bunch of financial services, so that users are able to access everything they need from one place. It is the epitome of convenience, but also incredibly complex from a development perspective.

A traditional fintech app differs from a super app as it typically serves a single function, like allowing users to make payments. A super app, on the other hand, integrates many services into one experience, sometimes even including non-financial features.

Super apps are becoming popular in banking thanks to a combination of open banking regulations and mobile infrastructure, which make it easier to offer a variety of services. User expectations also play a major role.

The biggest challenges in building a super app are regulatory compliance and data security. Choosing the wrong integration partner that causes a data leak or doesn’t hold up under an audit can result in a loss of user trust.

Financial institutions like banks and fintechs can benefit from the super app model by reaching more customers through partnerships and embedded finance integrations, gaining digital distribution without needing to build every product themselves.