Hire by Technology

SERVICES

Regulators in Europe have tightened the screws with SEPA Instant requirements, while at the same time, the world's largest payment rails have transitioned to ISO 20022, a new global standard for electronic financial messaging.

This combination is going to require massive updates, and if you haven’t started yet, you are already behind. The problem comes down to timing.

Deadlines landed in rapid succession: SEPA Instant rules required inbound support from January 9, 2025. FedWire’s message format shifted to ISO 20022 on July 14 of the same year, and SEPA mandated outbound instant payments from October 9.

Then, on November 22, 2025, SWIFT formally ended the coexistence period between MT and ISO 20022 messages for cross-border payments, marking the start of what SWIFT describes as a new era of richer, more structured payments data.

That left very little breathing room for anyone whose core systems weren’t built for real-time flows and structured messaging.

However, the same shifts that create headaches can also open doors. ISO 20022 and instant payments can become the foundation for stronger fraud detection, cleaner reconciliation, and the kind of services customers actually notice, like Request-to-Pay and intelligent cross-border routing.

Let’s walk through the pitfalls that trip teams up, and the practical steps you can take now, not just to stay compliant, but to build a payments stack that sets you apart once the dust settles.

For help ensuring your products can utilize the latest payment rails, you are in the right place.

The compression of so many major changes made 2025 an unusual year. Some companies had to rush to meet the requirements, which meant that they ended up with tech debt and related issues.

Having a better understanding of the regulatory timeline can help you better understand what to look out for in your own products, and perhaps even help you identify opportunities.

From January 9, payment service providers in the eurozone needed the ability to receive SEPA Instant Credit Transfers.

Even if your fintech doesn’t classify as a bank, if your partner institution touches Europe at any point, you need to have the ability to process inbound instant payments.

Some providers outside the eurozone, including certain EMIs and PIs, had the luxury of slightly later timelines, but in the euro area, PSPs have been on the clock since January.

The U.S. Federal Reserve then held to its delayed date of July 14 as the migration date for the Fedwire Funds Service.

What does this mean for you? In short, all Fedwire messages now use ISO 20022, and the legacy FAIM format no longer receives support.

By October 9, eurozone PSPs needed to send SEPA Instant payments.

For a lot of the companies that we worked with at the time, this requirement carried more weight than inbound, since outbound flows require changes to customer-facing systems, fraud controls, and reconciliation engines.

Some limited exceptions apply for non-eurozone PSPs, but most companies were held to this deadline.

Related Reading: How to Hit Roadmap Deadlines Without Hiring

On November 22, 2025, SWIFT formally ended the coexistence period between MT and ISO 20022 messages for cross-border payments and reporting.

They continue to offer a conversion service to handle remaining MT instructions automatically during the wind-down period, but ISO 20022 now serves as the required format for payment instructions across the SWIFT network.

If your fintech is operating globally, this means ISO 20022 fluency is now a baseline requirement.

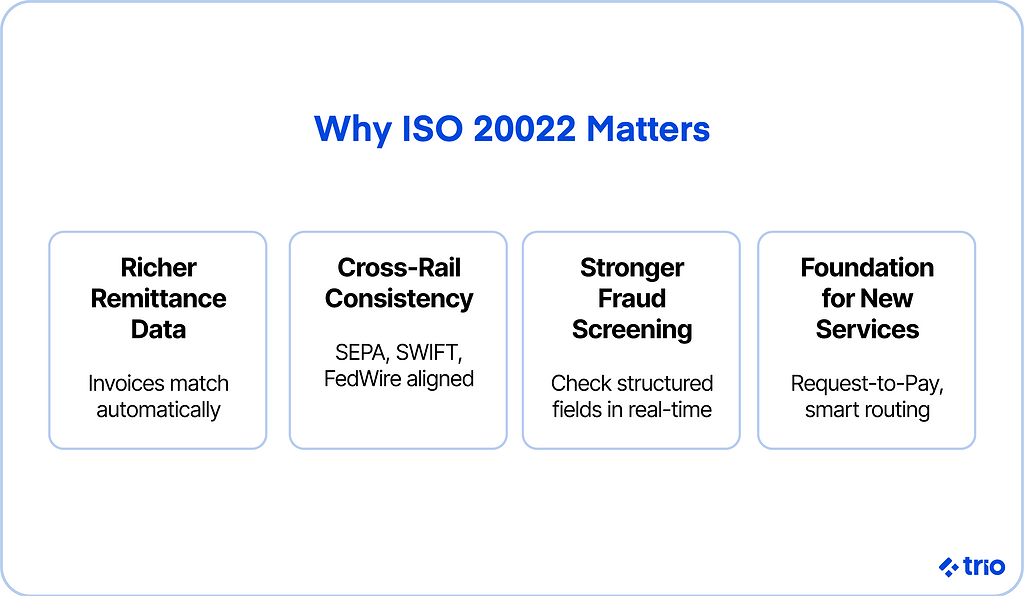

ISO 20022 may look like just another message format update, but the reality is a little more complex.

ISO 20022 marks the establishment of a shared language for payment rails that has the ability to carry meaning rather than bare-bones instructions.

Legacy formats have previously left banks and fintechs only able to pass around information like amount, account, reference, and little else.

This created difficulties in dealing with the many errors that occurred, and made fraud detection a lot slower than it could have been had there been more information available.

ISO 20022 changes the equation by embedding structured, data-rich fields into every message.

The G20 and the Committee on Payments and Market Infrastructures (CPMI) have both endorsed the standard, which appears to represent the first genuine attempt at an end-to-end global payments grammar.

While the upfront infrastructure implications can be costly, you should see it as astrategic investment that will become the backbone for global reach.

Most fintech stacks weren’t designed for instant settlement or for messages packed with structured data. That gap tends to show up in a few critical areas.

For months, and in some cases years, rails will run both formats simultaneously. Your systems will need to recognize and reconcile these messages in real-time, which means you’re probably going to need orchestration middleware to deal with the format differences.

Without this additional infrastructure, you would be left with brittle point-to-point fixes that collapse under volume.

The middleware layer buys time without forcing a full rewrite of downstream systems, and lets you avoid the additional expenses that come with scattering patch logic across multiple services.

Related Reading: Boost Approval Rates with Intelligent Payment Routing

Instant payments leave no room for manual review queues. Once money settles, recovering it can be virtually impossible. And, in the rare instances where you can do something, it may take weeks.

That puts pressure on fraud models to operate at millisecond speed.

Fortunately, ISO 20022’s structured fields give AI-powered models considerably more to work with. On top of cleaner KYC data that you would usually get, you also have access to structured counterparty information and behavioral signals that were previously buried in unstructured text.

Teams that wire detection logic directly into the transaction path, rather than running it as a downstream check, tend to catch more without generating excessive false positives.

That said, developers need to account for global data handling and security standards when deciding where models run and what data they can access.

There are already some third-party detection models built specifically for ISO 20022. These can help you reach production faster than building from scratch, and many have already cleared the compliance review process.

“Always-on” shifts from a marketing claim to a hard technical requirement. This is great for the user, but it is definitely a challenge.

Instant rails mean transactions flowing around the clock, with spikes that ignore business hours.

Horizontal scaling and API-first design all help, but they only deliver results if you’ve load-tested against realistic payment volumes.

We recommend that you focus on discovering capacity bottlenecks during stress testing. Finding issues before you go live puts you in a fundamentally different position than finding them in production.

If your systems can’t handle the load and crash during peak hours, it can be incredibly frustrating to clients.

In an effort to meet the deadlines we spoke about above, a lot of companies ended up forgoing testing and migration governance at levels that the industry would usually demand. Now, they are stuck with parallel runs, version mismatches, and cutovers that can’t tolerate downtime.

Automated testing and careful staging environments always reduce the risk significantly.

Teams that build personal accountability into their DevSecOps practices also tend to surface issues earlier, when fixing them costs far less than it would mid-migration.

The firms that come through this change and any others in good shape aren’t necessarily the ones with the largest budgets.

They tend to start early and design with both compliance and resilience in mind.

If you are starting with ISO 20022 from scratch, or even if you are trying to retrospectively assess your migration, you need to start by mapping every component that touches payments.

This can include messaging engines, fraud detection modules, reconciliation tools, and all the ways that data flows between them.

You’ll quickly identify where ISO 20022 mapping doesn’t exist yet and where legacy assumptions will break. That map also helps you prioritize. Not every system carries the same level of urgency.

During the coexistence period that we’re probably going to see for a while, you’ll need a way to process both ISO and legacy messages without breaking downstream systems.

We have already mentioned that middleware that normalizes message formats provides consistency throughout the transition.

What you also need to keep in mind is that middleware can help avoid the temptation to hardcode patches in multiple places, each of which becomes its own maintenance burden later.

Finding middleware for this and the upcoming changes before they come into effect is usually best.

Traditional fraud checks run in minutes or hours. With instant payments, that’s too slow by several orders of magnitude.

If we’re moving to faster payment trends overall, you will need to address this at some point.

With ISO 20022, everything you need to identify and address high-risk behavior before settlement occurs, because the data you need actually lives in the message rather than requiring a separate lookup.

If you rely on payment service providers or massive banks, their migration schedule may not align with yours.

You need to find out about any gaps before you just go live.

While it may be a bit of a headache to deal with international changes like this, it’s important to remember that there are additional benefits beyond simple regulatory compliance.

Since it aims to become an industry standard, ISO 20022 can connect to multiple markets with less friction.

Instead of maintaining a half-dozen mapping rules, you’re working from a common data language, which means it will be easier to scale into new geographies later, with the growth being faster and with fewer errors than the previous approach required.

Services like Request-to-Pay, dynamic payment scheduling, and financing offers triggered at the point of transfer already appear in pilots across European markets.

ISO 20022 makes them workable at scale in ways the legacy format couldn’t practically support, thanks to the wealth of information available to anyone, at any step of the money-moving process.

Clean, structured payment data lets you stop guessing about customer behavior, too. We’ve already mentioned how this can be a great asset in fraud detection, but it is also great for standard analytics.

Real-time dashboards for merchants, predictive cash-flow tools for small businesses, and personalized financial insights for consumers all become easier to build when the underlying data actually has structure.

Related Reading: Alternative Data for Credit Underwriting

Most fintechs still treat resilience and fraud prevention as overhead, but the reality is that faster settlement times with lower false-positive rates and tighter fraud controls form a legitimate part of your value proposition.

Customers will notice if their transfers clear instantly and securely. More importantly, if your competitors start setting expectations, customers will notice when your services fail to live up to them.

The deadlines that have already passed, but we’re probably still in a transition period. Consider how modern and compliant your own infrastructure is.

Instant rails and ISO 20022 are going to play a big part in global scaling and instant payment settlement, but only if you are able to move quickly enough to take advantage of new developments.

Waiting until the final quarter to react isn’t a strategy.

Our payments experts at Trio can help you figure out where to start.

Request a consult.

Missing the ISO 20022 deadlines puts your fintech at risk of losing access to key payment rails, including Fedwire and SEPA Instant. You may also be exposed to regulatory penalties.

All fintechs need to support SEPA Instant compliance if they are operating in or connected to the EU, including indirect participants whose partner banks have already committed to the standard.

ISO 20022 performs better than existing payment formats because the messaging carries data-rich fields, giving every transaction context that legacy formats couldn’t carry. That structured data makes automated reconciliation and real-time fraud detection easier.

ISO 20022 improves fraud detection in real-time payments thanks to its structured fields, which give fraud models richer signals to screen against, allowing AI-powered models to improve decisioning accuracy.

Scaling real-time payments without destabilizing fintech systems typically requires horizontal infrastructure, cloud-native deployment, an API-first approach, and thorough load testing against realistic transaction volumes.