Hire by Technology

SERVICES

Wealth management feels like it is standing at a crossroads. Investors expect fast, clear digital experiences, yet they still want the reassurance that comes from talking to an actual human advisor when things get messy.

Most wealth management firms are trying to keep up. They are under pressure to automate parts of the job, keep fees competitive, and still deliver financial advice that feels thoughtful.

It is not easy to satisfy all of these demands at once.

The rise of robo-advisors may look like the obvious fix, but fully automated platforms often make people nervous.

A lot of investors trust algorithms for routine portfolio management, although they hesitate when the stakes feel personal.

This gap has created space for hybrid robo-advisors that combine automation with human expertise.

These hybrid advisory models seem to meet investors where they are: they want smart automation, but they also want a human advisor ready when life changes, or markets slide.

This article walks through how robo-advisors work, how fintech is reshaping investment management, and why hybrid models are gaining traction across the wealth management landscape.

If you need an experienced developer to help you integrate robo-advisors into your existing financial services in a way that is both secure and compliant, we may have the right people for you.

Robo-advisors started as simple tools that helped people invest without needing a traditional advisor.

Over time, they evolved into more capable platforms that handle investment strategies, financial planning tasks, and ongoing portfolio management.

They are not replacing the entire wealth management industry, but they are changing how investors think about accessibility and cost.

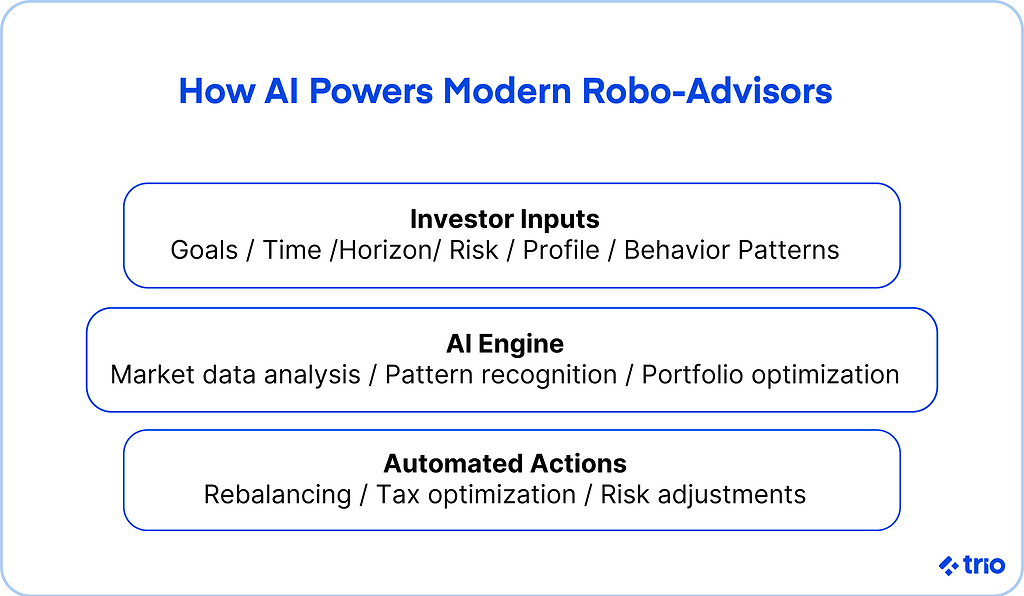

Robo-advisors use algorithms to manage investments based on your goals, time horizon, and risk tolerance. The models behind these platforms automate financial tasks that used to take hours.

They build a portfolio, allocate assets, and handle routine adjustments. Sometimes, they may just offer simple investment advice.

A typical robo-advisor relies heavily on ETFs and well-researched allocation frameworks. Some include features like tax optimization, rebalancing, and risk management triggers that respond to market conditions.

Most investors appreciate the simplicity. You answer a few questions, add funds, and the platform takes over.

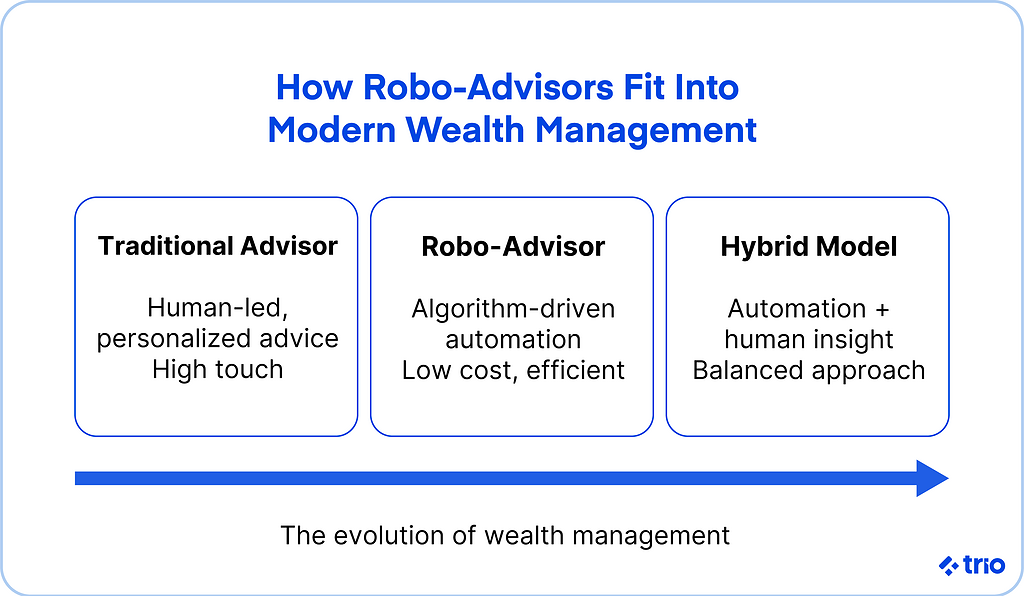

Not all advisory models work the same.

Some platforms run everything automatically with no human in the loop. Others rely on hybrid models that combine automation with access to a human advisor who can step in when decisions require judgment.

Fully automated platforms suit investors who want hands-off investing. Hybrid robo-advisors offer a middle path.

If you prefer talking to a financial advisor when the market gets shaky, hybrid advisory gives you that option without paying high management fees.

There are also differences between bank-supported robo-advisors and platforms built by fintech companies.

Banks lean on trust and established systems. Fintech companies tend to focus on speed, accessibility, and user experience. Both groups are part of the larger robo-advisory market, although their priorities differ.

Most modern robo-advisors use AI models at some level.

The use of AI may vary significantly from one platform to another, but it usually improves accuracy, personalization, and automation.

This shift is one reason automated investment options have become more appealing to a broader range of investors.

AI models help platforms review large amounts of information, including market conditions, historical data, and investor behavior. With these analytics, a robo-advisor can adjust a portfolio more intelligently than a simple risk-profile slider.

Machine learning appears to help platforms recognize patterns that human advisors might miss in a day-to-day workflow.

Some models even flag when an investor shows signs of emotional trading, which helps maintain long-term discipline.

Automation takes over once the portfolio is in place.

A robo-advisor can rebalance assets as they drift out of range. It can harvest tax losses throughout the year. It can run optimization checks more often than a traditional financial advisor would have time for.

This type of automated investment management is what many investors value most. It handles repetitive tasks and frees advisors to focus on high-value conversations.

These adjustments do not remove risk, although they can create a steadier long-term path.

Some platforms also test alternative allocation strategies for clients with complex needs, which feels like an early glimpse at the future of wealth management.

Personalization once meant choosing conservative, balanced, or aggressive.

Now AI can personalize financial planning and investment management in more subtle ways. A platform can adjust a portfolio to match real behavior instead of relying on general assumptions.

If an investor tends to withdraw during volatility, the system might shift toward assets that produce more stability. If someone adds funds frequently, the system may lean toward strategies that reward consistent contributions.

Hybrid robo-advisors take personalization even further by letting a human advisor interpret the output and explain how those decisions fit into a bigger financial planning strategy.

Fintech is one of the biggest forces disrupting wealth management.

There is a steady push toward simpler onboarding, more transparent pricing, and tools that let people invest regardless of portfolio size.

This rise of digital wealth management tools has widened access for users who used to feel shut out by high minimums and complex systems.

Fractional shares are a good example of how fintech companies have changed the landscape.

Younger investors can buy a small slice of companies they believe in without needing large sums. Some platforms let you automate recurring buys, helping new investors build habits.

Fintech also powers real-time adjustments, giving investors more control without overwhelming them. And with open APIs, platforms can share data more easily, which supports planning and investment management across different accounts.

These improvements make the entire fintech ecosystem feel more connected and responsive.

Hybrid robo-advisors may seem like a natural response to investor habits.

Many people like automation but still want a human advisor to talk to during big decisions. The hybrid approach also builds trust, which continues to be one of the biggest barriers for fully automated investment management services.

Hybrid models that combine automated investment tools with human financial advisors appear to meet the real-world expectations of modern investors.

When someone faces a major life change, they rarely want to depend on automation alone.

This blend of automation and human expertise helps reduce emotional reactions to market volatility. It works especially well for investors who want the efficiency of a robo-advisor but still value a personal relationship.

The robo-advisory market has grown fast. Investors see these platforms as an easy entry point, while wealth management firms use them to reach clients they could not serve efficiently before.

Some platforms focus on beginners. Others support complex financial planning for larger portfolios.

There is room for all of them in the current wealth management landscape.

Fintech companies tend to emphasize clean design, low friction, and quick sign-up flows.

They often use AI to personalize portfolios in ways that feel more modern than traditional financial advisors.

Banks take a different path. They highlight stability, management services, and long-standing client relationships. Some bank platforms include financial planning tools for retirement, tax planning, or college savings.

One example is the Vanguard Digital Advisor service. It uses automated investment tools backed by the firm's long history in index investing. Platforms like this help traditional wealth management firms stay competitive without losing their identity.

These differences show up in features like ESG screens, risk management controls, and financial advisory options that appeal to different investor groups.

The adoption of robo-advisors keeps climbing, especially among investors who grew up comfortable with fintech.

Younger investors appreciate accessibility and lower management fees. They also like that a robo-advisor can automate routine tasks without asking for constant input.

Institutions have joined the trend as well. Wealth managers use robo-advisory solutions to scale their advisory services, reduce overhead, and automate financial tasks that once took valuable time.

Robo-advisors continue to affect how wealth managers operate. Instead of replacing advisors, they shift the workload so human advisors can focus on high-value discussions instead of routine portfolio maintenance.

This helps advisors avoid long hours spent reviewing allocation models and lets them build stronger client relationships.

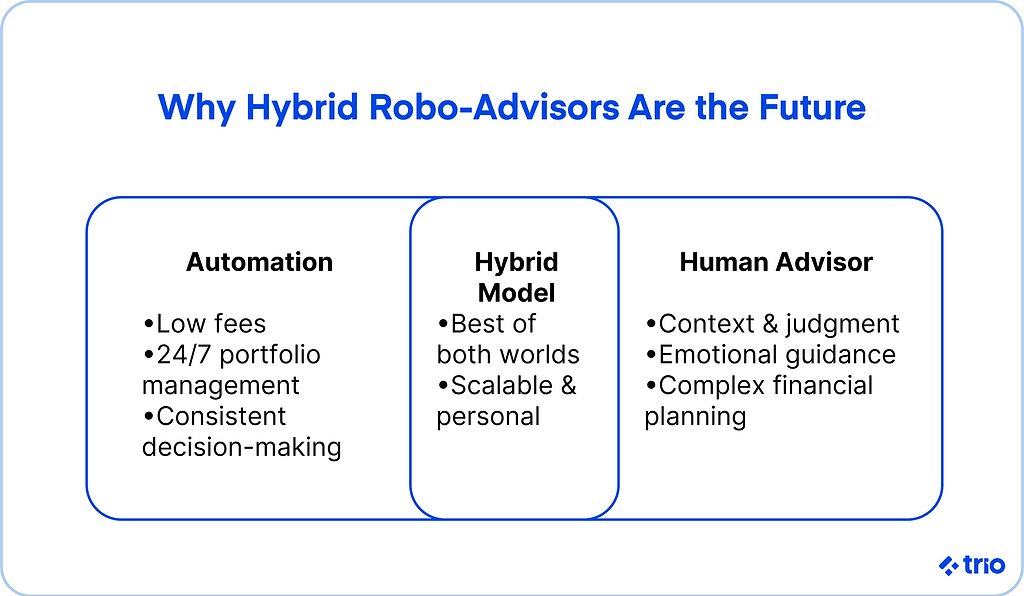

A robo-advisor works well for predictable tasks such as allocation, optimization checks, and rebalancing.

These tasks are perfect for automation because algorithms handle them consistently.

A human advisor shines in situations that involve emotions, uncertainty, or major life decisions. They can explain trade-offs, adjust expectations, and help investors think clearly during market volatility.

Investors tend to want both. Automated investment management offers speed and cost savings. Human advisors offer context and judgment.

Investors use these platforms differently depending on their stage of life.

Traditional wealth management firms are shifting toward technology-forward approaches. Many advisors now use platforms that automate financial tasks behind the scenes.

These systems allow advisors to monitor portfolios, run projections, and handle investment management more efficiently.

Some firms integrate analytics that flag when a portfolio needs attention. Others include financial planning tools that help advisors present clearer long-term forecasts.

These changes lower operational workloads and help financial advisors stay competitive in a market where investors expect digital convenience.

Even with all the progress, robo-advisors face real problems.

It is worth acknowledging these issues because wealth management services depend heavily on trust and transparency.

Robo-advisors must follow strict guidelines.

Regulators want to know how the algorithms work, why certain decisions are made, and whether the system is making suitable recommendations. Platforms also need to document how they automate financial processes.

These rules exist to protect investors. They do, however, create extra work for firms that rely on automated investment strategies.

Security remains a major concern in digital wealth management.

A robo-advisor stores sensitive financial information that requires strong encryption and ongoing monitoring.

Any breach, even a small one, can damage user confidence. This is one reason hybrid models appeal to many investors. Having a human advisor available helps reinforce trust when people feel uneasy about automation.

Algorithms can struggle during extreme market conditions. They make decisions based on historical data, and some edge cases fall outside normal patterns.

When volatility hits unexpectedly, many investors prefer talking to a human advisor who can explain what is happening.

As we have already mentioned, this is one of the biggest reasons hybrid models that combine human expertise with automation are growing quickly. The human advisor can guide clients through situations where automation alone might feel unclear.

The future of wealth management is shaping up to be a mix of automation, human guidance, and smarter analytics.

Robo-advisors continue improving, and hybrid advisory models appear to be the direction many wealth managers are moving toward.

Generative AI may help platforms run detailed simulations that adapt to real-time changes. Some firms are experimenting with digital financial twins to let investors visualize long-term outcomes.

These tools are new, and adoption will likely depend on how comfortable investors feel with deeper automation.

Platforms are also testing features that allow portfolios to adjust themselves more frequently. This may offer a smoother response to market conditions, although it still requires oversight to avoid unnecessary trading.

Over the next decade, we think financial planning and investment management are likely to feel more tailored. Systems may track behavior and adjust portfolio management based on real habits rather than theoretical profiles.

Market trends that we have seen while in the field point toward greater accessibility and lower management fees.

Investors may see consistent advisory services across banking, insurance, and investing through a shared fintech ecosystem.

The potential of robo-advisors is high, although growth depends on regulation, investor comfort, and how well platforms balance automation with human expertise.

Advisors are not being replaced by automation. Instead, they are shifting into roles that complement AI systems. A human advisor can interpret risk, guide emotional decisions, and help investors clarify long-term goals.

Hybrid models that combine automated investment tools with experienced advisors give clients a balanced service. Advisors can spend more time on strategic planning and less time on routine tasks.

In many ways, this combination may represent the future of wealth management services. Advisors bring human understanding, and automation brings consistency.

Robo-advisors offer practical tools that help investors get started and stay consistent. Fintech continues transforming wealth management by making investment management more accessible and easier to understand.

Hybrid robo-advisors are becoming the preferred choice for many investors. They blend automation with the reassurance of a human advisor who can help during uncertain times.

As technology expands, wealth management firms that adopt a balanced approach will likely adapt more easily to changing expectations. Investors want automated investment support when possible, and human guidance when it matters most.

If you want to start looking at what you will need to create a robo-advisor of your own, or you need specialists to make sure your existing product is secure, compliant, and offers accurate financial management, our expert fintech developers can help.

Get in touch!

A hybrid robo-advisor is a platform that blends automated portfolio management with access to human advisors. A hybrid robo-advisor works well for people who want low fees and automation but still value human guidance during big decisions.

Fintech innovations influence robo advisors by enabling fractional investing, smoother data sharing, and more responsive portfolio management. These tools make robo-advisors feel more accessible and more adaptable to different investor needs.

Hybrid robo-advisors are better for investors who want automation with human support, especially in uncertain markets. Fully automated robo-advisors may suit users who prefer a simple, low-cost, hands-off approach.

Hybrid robo-advisors usually cost more because they include human expertise, although fees still tend to be lower than traditional advisors. The extra cost often pays off for investors who want reassurance and context.

Beginners can use hybrid robo-advisors because onboarding is simple, and human advisors can answer basic questions. A hybrid robo-advisor helps new investors feel more confident as their portfolio grows.