Hire by Technology

SERVICES

CTOs and Heads of Engineering across the banking sector face the same tension: customer expectations rise, but engineering capacity rarely scales at the same speed.

Knowing about the top trends in digital banking allows you to prepare ahead of time, find the right developers with the right skills, and work on new features long before they become urgent.

The top banking trends reshape user experience and quietly raise the technical bar for every digital bank and financial institution competing in this space.

Artificial intelligence in banking demands auditability. Open banking increases vendor risk. Personalized financial tools require tighter data governance than many teams anticipated.

The institutions that win will build deliberately, with infrastructure, security posture, and engineering depth aligned from the start.

Let's go over the most important banking trends and, more importantly, what they mean for fintech teams responsible for delivering secure, scalable digital banking services inside a regulated financial industry.

At Trio, we have extensive experience in digital banking as well as many other fintech products. View our capabilities.

With the constant hype around AI, it is no surprise that it has made its way into banking. Artificial intelligence in banking has moved past chatbot demos and basic automation.

AI quietly shapes underwriting decisions, fraud detection, digital customer support, and even proactive financial advice.

We saw early AI in financial services being used to handle basic automation, like repetitive support tickets.

Today, it's far more advanced. Agentic systems manage portions of lending workflows, flag suspicious banking transactions in real time, adjust credit models dynamically, and much more.

Some digital bank platforms already test semi-autonomous decision layers that reduce manual review cycles.

Our developers have noted that this shift reduces operational friction, but it also raises the stakes. When AI touches core banking operations, auditability and explainability become critical.

Regulators now expect financial institutions to document model behavior clearly.

In retail banking and lending environments, opaque AI logic invites scrutiny.

Fintech engineering teams must design artificial intelligence systems with logging, rollback capability, human oversight, and general auditability built in from the start.

In practice, that means integrating model monitoring into core banking infrastructure.

AI-driven digital transformation sounds strategic at the board level. At the implementation level, it translates into data pipeline upgrades, stricter access controls, and stronger environment separation across digital platforms.

For fintech teams scaling quickly, the real constraint often becomes talent capacity.

Building responsible artificial intelligence in banking requires engineers who understand both financial technology and regulated environments. Without that domain fluency, teams risk slowing releases or exposing compliance gaps.

Finding developers with both this skillset and fintech experience is our specialty here at Trio.

Mobile banking now anchors the entire digital banking model. People have their phones with them all the time, making banking apps the natural option for most.

What began as a companion app has become the primary interface between banking customers and financial products.

The growth of the digital wallet reflects a broader shift in banking adoption.

Customers expect instant digital payments, available around the clock with a seamless checkout process. They also want the process of utilizing their wallets to be secured through methods like biometric authentication.

For a digital bank, supporting mobile wallets involves more than integrating Apple Pay or Google Pay.

It requires secure tokenization, fraud prevention logic, and tight integration with core banking services so that balances, alerts, and spending insights update instantly.

Some digital banking trends point toward consolidation.

Instead of switching between tools, users expect a unified banking platform that combines payments, savings, investing, and lending in one place. In other words, they expect a fintech super app.

Super app models blur lines between financial services and everyday digital tools.

Embedded insurance at checkout and point-of-sale lending need to appear in non-banking digital platforms. For product teams, that means designing APIs flexible enough to support external partnerships without compromising secure digital architecture.

Rising smartphone penetration, as we have already mentioned, also continues to fuel reliance on mobile banking.

Instead of people sitting down to take care of all of their banking tasks at once, banking usage now happens in micro-moments, often on a single mobile device throughout the day.

This behavioral shift changes performance expectations drastically.

A slow banking app or delayed push notification doesn’t just frustrate users; it erodes trust quickly.

Engineering teams must optimize for low-latency transactions, real-time alerts, and resilient backend systems that withstand traffic spikes.

Mobile-first design often improves operational efficiency when executed well. As the name suggests, this is a model that assumes the majority of banking is going to happen on a mobile device, in any place, at any time.

Digital onboarding for an online bank account, automated identity verification, streamlined customer support, educational resources, and more all reduce strain on physical branch networks.

However, migrating customers away from traditional banking channels requires robust backend systems.

If digital offerings fail during high-demand periods, such as if payment systems can’t deal with a massive spike caused by Black Friday, customers revert to physical branch visits, increasing costs and damaging confidence in digital banking services.

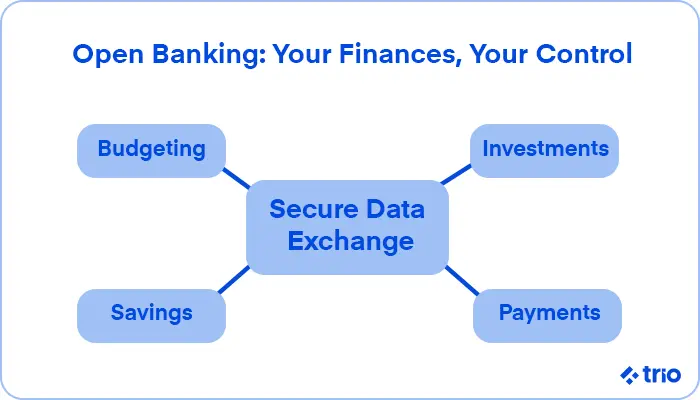

Connected ecosystems are another trend that is quickly becoming a baseline expectation from users.

Open banking initiatives and API-first architectures reshape how financial institutions collaborate.

Open banking encourages secure data sharing between approved providers. For banking users, that means easier access to financial tools, consolidated dashboards, and personalized financial insights across accounts.

For fintech engineering teams, it means building API layers that handle authentication, rate limiting, and permission management securely using techniques like tokenization to ensure data is encrypted.

A weak integration can expose sensitive data or disrupt banking operations across multiple partners.

Embedded finance expands banking solutions beyond traditional boundaries. Retail platforms, ride-sharing apps, and SaaS tools increasingly integrate financial products directly into their workflows.

While this approach increases access to financial services, it also complicates governance. Every embedded integration introduces vendor risk, data-sharing complexity, and dependency on external uptime.

Security leaders in financial institutions already scrutinize internal systems. Open ecosystems multiply the surface area.

Connected banking requires strict least-privilege access, environment separation between development and production, and documented incident response pathways. Without disciplined architecture, the promise of digital innovation quickly collides with compliance reality.

Customers now expect personalized banking that mirrors recommendation engines in entertainment and e-commerce. Generic product pushes feel outdated.

Banks are now able to analyze spending behavior and transaction patterns to deliver contextual financial advice.

A banking app might suggest adjusting savings contributions after a salary increase or flag unusual subscription spikes.

Predictive models support personalized financial recommendations, but they rely on clean, well-structured data, so fragmented systems across digital and physical channels weaken insight accuracy.

Regulators and customers alike demand transparency.

Banking customers want clarity on how their data powers recommendations and digital offerings, and how it is being stored or shared.

Strong governance frameworks allow users to manage notification settings and data-sharing permissions.

Over-automation risks crossing into intrusive territory. Under-personalization feels generic.

In short, we’ve seen that delivering personalized banking at scale requires careful balance.

Engineering teams must design modular recommendation engines that respect user-defined boundaries.

Sustainability increasingly influences banking trends. Customers, especially younger demographics, examine how financial institutions align with environmental and social priorities.

Green lending programs and ESG-focused investment portfolios may become part of more mainstream offerings.

Digital bank platforms often surface impact metrics directly inside dashboards in an effort to attract clients and investors.

But, without credible measurement, sustainability claims risk reputational damage.

We’ve seen some institutions explore blockchain-based traceability for sustainable investments, while others integrate third-party rating systems into digital platforms.

Engineering teams must ensure that sustainability metrics remain accurate, up to date, and clearly explained.

As digital banking matures, differentiation increasingly depends on engagement rather than access alone.

Social banking reflects a broader shift in how banking customers interact with financial tools and with each other.

Community features inside a banking platform might once have sounded experimental, but now they increasingly shape product strategy.

Some digital bank platforms allow users to compare anonymized spending benchmarks, share saving strategies, or participate in moderated financial literacy forums.

For retail banking teams, these collaborative banking tools increase engagement and retention.

However, community-driven features also require thoughtful moderation systems. Unchecked peer advice in a financial services environment can create compliance exposure.

Modern banking users expect a voice in how digital offerings evolve.

Feedback loops embedded directly into a banking app, structured beta programs, and user advisory panels can give users a sense of satisfaction and make them feel like their needs are being considered.

This shift benefits digital innovation when managed carefully.

Product teams gain faster validation and clearer signals around customer needs. But it is important that governance remains your utmost priority.

Social banking is great in many ways, but we cannot ignore that it increases platform complexity.

Storing user-generated content and facilitating and managing discussion spaces introduce new risk vectors.

Security leaders must treat community features with the same rigor applied to core banking services; these added layers can strain banking operations and introduce reputational risk.

In line with the super apps we mentioned above, customers are increasingly expecting more than just simple money storage and transfer abilities.

Many now look for continuity in financial services across all of life’s stages, from first paycheck to retirement planning.

Lifetime banking requires product architecture that adapts as customers evolve. This gives you the opportunity to decide on a target market and evolve your features as they grow, rather than trying to provide all of the features at once.

For example, a digital bank serving early-career professionals may initially focus on budgeting and digital payments.

Years later, those same customers will expect lending options, investment tools, and wealth management features, which means that you can start working on those offerings.

Modular banking products and configurable digital platforms allow you to offer these services later without forcing migrations to separate systems.

Advances in artificial intelligence in banking enable proactive insights tied to life events.

Spending pattern shifts may indicate relocation. Income changes may signal career progression. These signals allow banking solutions to surface relevant financial advice at the right moment.

If earlier banking trends focused on improving interfaces, invisible banking shifts attention to what customers no longer see.

Financial services increasingly operate in the background, embedded into everyday digital experiences.

Embedded finance allows customers to access financial products without navigating a traditional banking app. Insurance at checkout and financing integrated into e-commerce are some of the most common examples we see.

For a digital bank, success in embedded models depends on resilient API infrastructure and secure data exchange.

External platforms may drive the user experience, but accountability for financial accuracy and compliance remains with the financial institution.

Invisible banking reduces friction by automating routine decisions.

Automated bill pay, real-time fraud detection, and dynamic savings adjustments occur without manual intervention.

From the outside, the experience feels seamless. Internally, however, these digital technologies require robust monitoring systems, clear escalation pathways, and precise logging of banking transactions.

When automation handles critical financial flows, oversight must remain tight.

The contrast between traditional banking and digital bank models is important to note, especially for fintechs who are likely to work as digital-only entities or perhaps only partner with traditional banking institutions.

Neobanks, or digital-only banks, typically benefit from very modern core banking infrastructure and leaner operational structures.

Since they do not have to maintain or retroactively deal with issues in legacy physical branch networks, they can iterate very quickly on digital offerings and mobile banking features.

Onboarding is also usually optimized for the digital experience, since it is literally impossible for users to go into a branch at any point.

This agility and optimized user experience combined often attract younger banking customers who are comfortable with fully digital service.

Rapid feature deployment, facilitated by skilled fintech engineers, also strengthens their competitive position.

You can think of traditional banking institutions almost as the opposite of neobanks in many regards.

They often operate complex legacy systems layered over decades. Integrating modern digital platforms with older core banking services introduces technical friction, which takes longer for developers to deal with.

Digital transformation initiatives attempt to close this gap, but migrations rarely move quickly when you compare them to the speed of smaller startups.

Since they have an existing client base, these massive institutions are also stuck balancing digital and physical channels and must maintain stability while modernizing incrementally.

Speed increasingly determines market position. Whether digital-first or legacy-based, financial institutions that cannot secure sufficient engineering capacity struggle to keep pace with trends in banking.

The gap often does not stem from strategy. It emerges from execution bottlenecks, delayed hiring cycles, and limited access to engineers fluent in financial technology and regulated environments.

Let’s take a look at some banking statistics that help contextualize these emerging trends and ground strategy in real-world usage patterns.

Mobile banking adoption continues to rise across demographics. According to a study by the American Bankers Association, younger users show an incredible reliance on mobile banking apps, while older cohorts steadily increase digital usage as digital literacy improves.

While there is definitely still a place for other banking methods, this steady shift indicates that it is very important to invest in reliable mobile and online banking infrastructure.

Digital platforms should be viewed as primary service channels rather than supplemental tools.

Online banking and internet banking remain widely used, with 3.6 billion global users.

Mobile platforms are very popular, but approximately 25% of U.S. adults prefer web-based online banking. In our experience, this is likely due to the larger screen size.

By making sure to devote resources to both mobile apps and browser-based digital banking channels, you are more likely to capture broader engagement and reduce strain on physical branch networks.

Customer loyalty increasingly correlates with digital experience quality. In the same ABA survey we mentioned above, 95% of users had a positive perception of their bank’s digital offerings.

These positive interactions foster a perception of trust, which makes digital banking services a strategic asset, even for well-established banks.

Recognizing digital banking trends helps at the strategy level, but only if you understand the implications and what you need to focus on while still ensuring that you deliver products that can stand up to regulatory scrutiny.

Execution speed is a major advantage. If you get a new feature out first, users are likely to test your software, which may result in a long-term conversion.

A strong roadmap without the engineering capacity to support it simply creates backlog and burnout.

For growth-stage fintech companies, capacity gaps can become a major issue.

Hiring senior engineers with financial services experience can take months and can be incredibly expensive. In a market where digital bank competitors iterate weekly, that delay compounds quickly.

Teams that secure vetted, domain-fluent engineers early tend to maintain release velocity without compromising security or compliance.

Even highly skilled developers slow down when they lack context around core banking best practices and compliance requirements.

Fintech teams building lending platforms, digital payments systems, or digital currencies cannot afford long onboarding cycles.

Engineers who already understand regulated financial systems contribute meaningfully faster, reducing friction across product and security teams.

The only thing that they need to familiarize themselves with is the specifics of your product, not the entire industry.

Scaling a digital banking model introduces structural risk. More users increase the load. More integrations expand the attack surface.

To make matters even worse, the more features you offer, the more difficult it can be to test and identify potential issues.

Security leaders in financial institutions scrutinize things like access controls and vendor exposure. Investors and product managers may push for speed.

It is critical that engineering leadership and CTOs step in to ensure a balance between the two pressures.

If you need skilled engineers and engineering leaders on your team, you are in the right place. At Trio, we focus on fintech development, meaning all our senior engineers have industry experience, specifically in U.S. markets.

They are familiar with regulatory requirements and user expectations, and can help you strike a balance between developing quickly and developing resilient products.

To find out more about our services and if we have the right developers for you, request a consultation.

Digital banking refers to when you offer core banking services through digital channels like online banking or mobile banking apps instead of relying primarily on a physical branch.

The difference between digital banking and digital-only banks is that digital banking describes any banking services offered online, while digital-only banks operate without physical branches. One example of a digital-only bank is what is commonly referred to as a neobank.

A neobank is a type of digital bank that operates fully online, often focusing on streamlined mobile banking and simplified financial products. They do not have any physical branches at all.

Online banks are safe when they follow regulated security standards, including encryption and secure digital authentication. They need to be held to the same standards that you would require from traditional banking institutions.

A financial super app is a banking platform that combines wallets, payments, lending, investing, insurance, and other financial services into one integrated mobile app experience. It is a one-stop shop where users can get all the services they need.