Hire by Technology

SERVICES

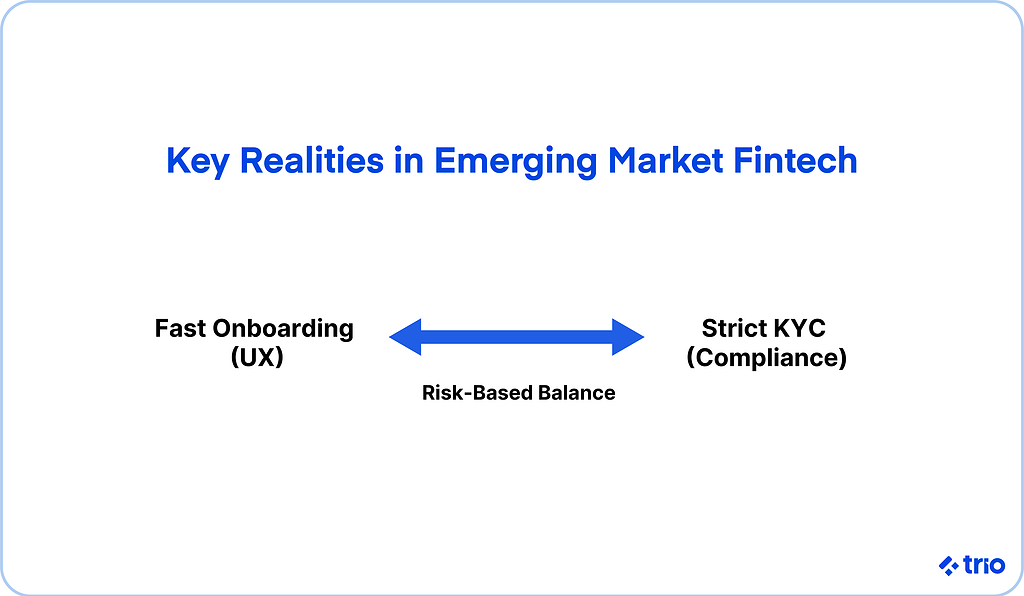

Fintech companies often feel stuck trying to create a fast onboarding process while also meeting every KYC and AML rule under the sun.

It sounds simple on paper, yet the moment your client onboarding flow slows down or asks for something unexpected, potential users start drifting away.

A small hiccup may be all it takes for someone to try a different financial service that feels easier.

This tension only gets worse as synthetic identities and deepfake attempts increase.

Some teams respond by tightening every control, which might look safe at first, but often frustrates new users. Others take the opposite path and try to make everything seamless, which sounds nice until a regulator points out gaps in the onboarding process.

A more sustainable path usually appears when you combine a risk-based KYC process with thoughtful design and reliable tools.

That approach tends to reduce friction, support faster onboarding, and help you prevent fraud without slowing people down.

It also gives you a better chance of meeting global regulatory requirements without burning out your compliance team. At Trio, we have a host of fintech specialists who can advise your team and help implement these solutions.

Before improving your client onboarding process, it helps to step back and look at what KYC means for financial institutions today. At its core, KYC involves verifying a customer's identity, assessing their risk profile, and screening for global sanctions or red flags connected to financial crime.

For fintech companies, this usually includes document verification, identity verification checks, and ongoing monitoring. In many cases, the onboarding journey also triggers customer due diligence requirements that must meet both local and global standards.

The challenge is that fraud tactics keep evolving. Deepfake video calls that look convincing at first glance, or synthetic identities stitched together from real and fabricated data, can slip through older verification systems. Regulators are very aware of this shift, and they expect companies to keep up rather than rely on outdated methods.

Strong KYC compliance supports trust and protects both your new customer and your business. Weak controls tend to show up later in the form of chargebacks, unexpected AML alerts, or regulatory audits that become far more stressful than they need to be.

A typical digital onboarding process starts when a new customer enters a few basic details, then moves through identity verification and a set of automated checks.

By the time the onboarding experience ends, the company should have enough information to understand the customer's identity and their intended financial activities.

The tricky part is that every step introduces a chance for friction.

A blurry photo, a liveness check that feels finicky, or a missing piece of customer information can disrupt the entire customer onboarding experience. Even if your compliance team knows why the step matters, users may not understand it.

A smoother onboarding journey often depends on clear instructions, predictable steps, and verification tools that behave consistently on different devices.

Fintech companies face several recurring issues during onboarding.

Some challenges are obvious, like customer drop-off when document capture keeps failing. Others are subtle, such as identity theft attempts that look harmless at first or data collection requirements that vary from country to country.

Jurisdiction-based rules can be especially tough. The United States may ask for owner information during business onboarding, while the EU uses eIDAS guidelines, and the Financial Action Task Force publishes updated expectations on digital identity.

Even when global and local rules overlap, they rarely align perfectly.

User experience is also a major pressure point.

If the onboarding solution treats every applicant as high risk, the process becomes slow and heavy. On the other hand, if verification requirements drop too low, you may accidentally approve someone who triggers AML (anti-money laundering) regulations later.

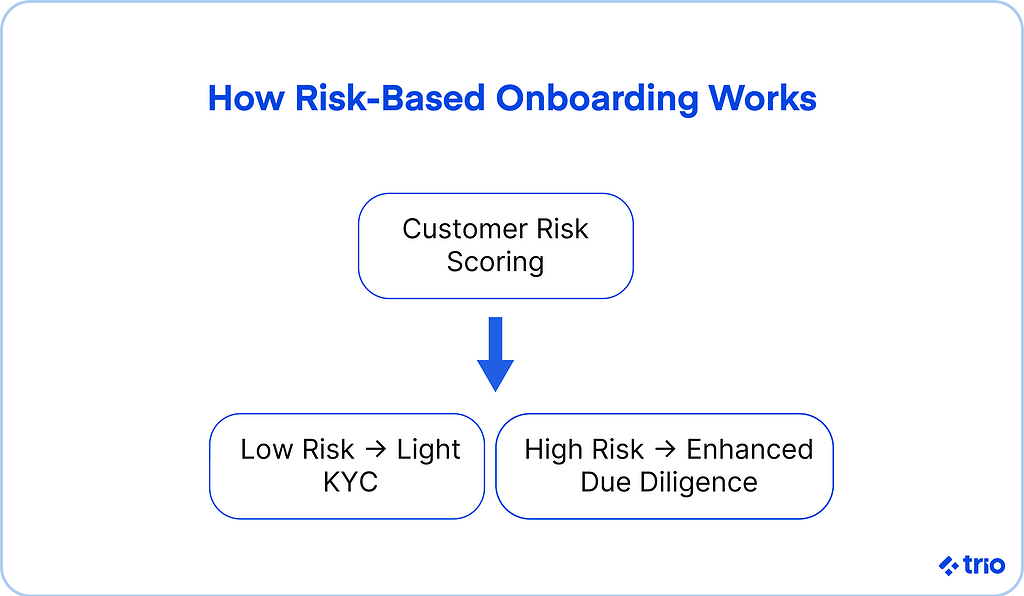

A risk-based approach tends to work well because it adjusts the onboarding process based on real signals rather than treating everyone the same.

Customers with a low risk assessment can move through a more lightweight onboarding journey. People who appear higher risk move through enhanced due diligence instead.

Small design choices play a big role here.

Clear prompts during document verification, shorter copy, and guidance when something fails can reduce frustration. You may also find that personalizing the onboarding process to match common document types or connection speeds in specific countries helps customers finish without confusion.

We have seen fintech teams reduce friction simply by reordering steps or by giving users a tiny bit of explanation about why identity verification matters. It sounds minor, but it can change the customer experience drastically.

When this balance works, you get faster onboarding times, improved customer satisfaction, and fewer false positives that would otherwise hold people back.

KYC software can automate large parts of the onboarding process and reduce manual review.

Most fintech teams rely on some combination of biometric checks, OCR for document verification, and real-time identity verification to validate a customer's identity.

API based KYC solutions give you the flexibility to change the journey depending on risk or region.

Some providers also include behavioral analytics to detect suspicious movements or unusual typing patterns, which helps prevent fraud without adding visible steps.

One interesting shift is the rise of low-document and zero-document onboarding in certain regions.

These approaches rely on trusted data sources rather than forcing customers to upload documents. When done correctly, it leads to faster onboarding with less frustration.

It is also important to choose tools that reduce false positives rather than create piles of unnecessary alerts. That is partly why companies often work with partners like Trio, who help engineering teams select the right KYC provider, integrate APIs cleanly, and ensure compliance without slowing product development.

The regulatory landscape keeps shifting, and it can feel like a moving target.

In the EU, the AMLA authority and eIDAS 2.0 identity wallets are shaping digital onboarding expectations.

The US continues to expand its rules around beneficial owners.

The UK updates JMLSG guidance frequently, and countries across the GCC push toward unified digital KYC.

These changes affect not only KYC onboarding but also ongoing monitoring, recordkeeping, and customer identification requirements. Your compliance team must stay familiar with both global sanctions lists and local AML regulations.

Companies must also pay attention to audit trails, data residency, and how automated decisions are reviewed by real people.

Teams that invest in compliance early often find expansion easier later, especially when working with experienced fintech developers like those at Trio, who help them navigate the complexities of KYC and AML with fewer growing pains.

Several trends appear to be shaping client onboarding.

AI-driven verification is becoming more common, although regulators encourage companies to maintain human oversight. Predictive risk scoring is gaining traction, but it works best when paired with clear policies.

Reusable digital identity is also on the rise through verifiable credentials and eIDAS 2.0 wallets. This may cut down on document verification requests, which could eventually help reduce friction for both new and returning customers.

Zero-knowledge edge proofs are getting attention, too.

They allow people to prove certain facts without exposing unnecessary customer data. While not mainstream yet, they hint at a privacy-conscious future for financial services.

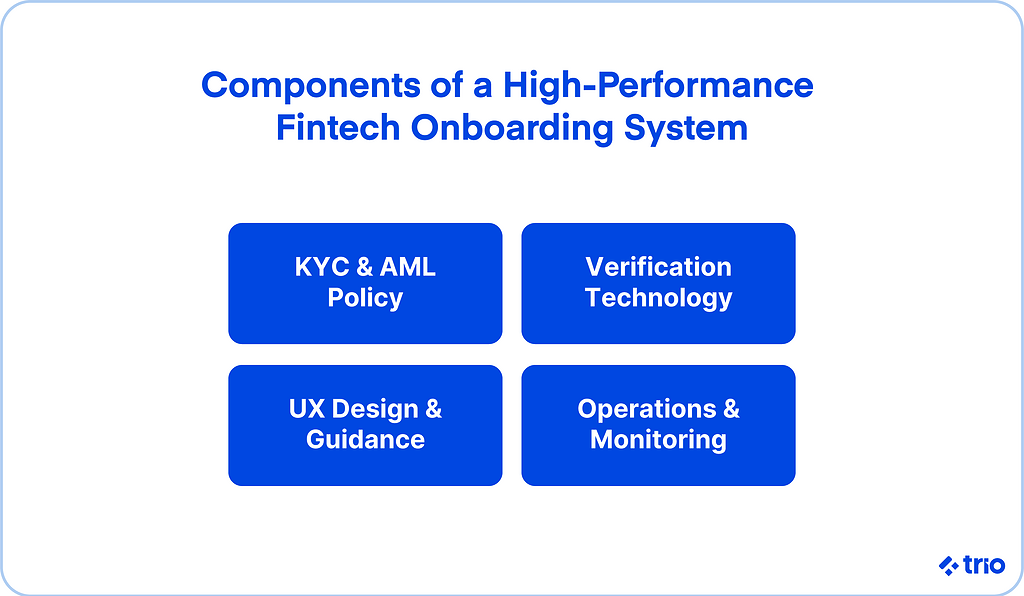

A strong onboarding solution relies on clear policies, good tooling, and a team that understands the regulatory requirements behind each step.

This includes customer due diligence, enhanced due diligence, and ongoing monitoring once the customer begins financial activities.

Vendor selection matters as well.

Some KYC providers offer reliable uptime and clear documentation, while others introduce complexity that slows product teams down. Many fintech companies use a mix of third-party tools for verification, authentication, and AML screening.

It also helps to train your operations and support teams so they can spot red flags, recognize suspicious behavior, and understand how different decisions affect compliance and customer experience.

Sometimes these teams catch problems long before automated systems do.

Working with engineering partners such as Trio can shorten the time it takes to build a secure onboarding experience that scales as your customer base grows.

Teams that succeed with digital onboarding often share a few habits.

They test their onboarding journey regularly with real users, they refine their KYC process instead of leaving it static, and they use data to understand where friction occurs.

Some companies noticed that asking for a document too early caused drop-offs, so they shifted it to a later point. Others realized their identity verification provider generated too many false alerts, and switching to a different KYC software cut their operational workload significantly.

Changes like these may sound small, but they often improve customer retention and reduce the number of people who stall during onboarding.

A thoughtful onboarding process can help you prevent fraud, keep regulators happy, and give new customers a smoother start. It takes creativity, strong systems, and a clear approach to KYC compliance, but the payoff is worth it.

When fintech companies balance UX with regulatory expectations, they tend to grow faster and avoid costly surprises.

If you refine your onboarding journey, select KYC solutions carefully, and keep your compliance team involved early, you can create a client onboarding experience that feels straightforward for users and dependable for your business.

You need developers who are not only great at coding but also understand the unique challenges of the industry. To hire fintech developers, get in touch!

KYC in fintech onboarding refers to verifying a customer's identity and risk level so the company can meet AML regulations and prevent financial crime.

Fintech companies can reduce friction during the onboarding process by simplifying steps, improving guidance, and using verification tools that adapt to a customer's risk profile.

Customer onboarding requires identity verification because financial institutions must confirm the customer's identity to comply with AML rules and avoid onboarding high-risk users.

KYC onboarding best practices for fintech companies include using risk-based checks, clear instructions, and real-time verification to support a faster and safer onboarding experience.

Fintech companies ensure compliance during client onboarding by following regulatory requirements, documenting decisions, and using monitoring tools that track sanctions and red flags.

A risk-based approach to KYC means adjusting verification depth depending on a customer's risk profile so the company can avoid unnecessary friction for low-risk users.