Hire by Technology

SERVICES

AI API spend has become one of the fastest-growing and least-governed line items in fintech engineering budgets.

A fraud detection pipeline that costs $800 a month at launch can cost $12,000 four months later because each new feature added tokens to every request without anyone reviewing the cost.

Understanding where fintech AI workloads run expensively can provide valuable insights into ways to optimize AI token costs and reduce overall AI spend for fintech engineering teams.

We have identified three structural reasons. Compliance system prompt length, AML and fraud screening volume, and agentic compliance work.

Let’s look at how you can fix these issues specifically in fintech contexts, with current pricing, concrete numbers, and a routing matrix that maps workload types to the model tier that actually fits them.

If you need developers to help you build your fintech applications, using AI efficiently to improve productivity and service quality while staying within your budget, we can assist.

Output tokens cost several times more than input tokens across every current Claude model. Typically, there’s a 5x ratio.

That asymmetry means that, if your fintech pipeline returns verbose JSON explanations when it only needs a classification and a confidence score, you will be paying a real premium for output nobody reads.

Structured output with an explicit token cap is the direct fix, but we’ll go into that more below.

Regarding input tokens, prompt caching cuts cached input cost by roughly 90%.

When a prompt prefix stays stable across calls, a compliance system prompt, a regulatory reference document, or a CLAUDE.md file, Claude can cache that prefix and charge a small fraction of the standard input rate to read it back.

This is the highest-ROI single lever that our developers have been able to implement for most fintech AI workloads.

However, it’s important to keep in mind that the first write to cache actually costs more than a standard call (roughly 1.25x base input for the short-lived 5-minute cache, or 2x for the longer 1-hour option), so caching pays for itself on reuse, not on the first call.

Finally, batch APIs have become a best practice, as they can cut costs by a flat 50% across the board.

For anything that doesn't need a real-time response (overnight AML screening batches, compliance document analysis, and fraud pattern processing), this is a great way to save some AI spending.

If your team is mid-migration, the tokenizer changed between Opus 4.6 and Opus 4.7, and it can generate meaningfully more tokens, up to roughly 35% more, for the exact same input text.

Related Reading: GitHub Copilot vs Cursor for Fintech: What Changed in June 2026

Let’s look at an example of what current production rates go for, for Claude specifically. Keep in mind that these figures change relatively often, though, so it is important to verify real-time information before you start budgeting.

| Model | Input ($/MTok) | Cache read ($/MTok) | Output ($/MTok) | Batch discount |

| Claude Haiku 4.5 | $1.00 | ~$0.10 | $5.00 | 50% off |

| Claude Sonnet 4.6 | $3.00 | $0.30 | $15.00 | 50% off |

| Claude Opus 4.8 | $5.00 | $0.50 | $25.00 | 50% off |

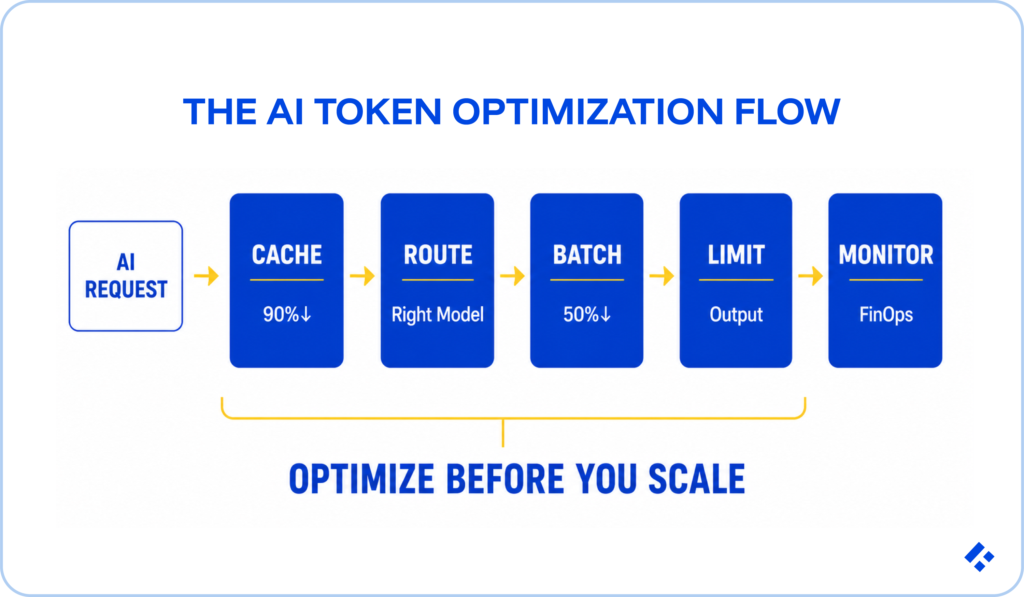

Seven levers control token spend in total, but the order that makes sense for fintech can be slightly different from more general development orders.

Compliance prompt volume, screening scale, and agentic usage patterns push some of these levers incredibly high.

A KYC screening system prompt carrying regulatory requirements, FATF definitions, PEP screening criteria, jurisdiction-specific rules, and AML typologies can easily run 2,000 to 5,000 tokens.

Without caching, every single call pays the full input price for that static content.

If, for example, you are dealing with 100,000 daily screening calls at 3,000 tokens of compliance context each, that's 300 million compliance-context tokens a day, at $3.00/MTok, that's $900 a day spent just re-sending the same regulatory boilerplate.

To fix this, structure the prompt so the compliance context sits as a stable prefix, then add a cache_control breakpoint at the end of that stable section, before any per-request variable content.

As we have mentioned, cache reads cost a small fraction of the uncached rate. On Sonnet 4.6, that's $0.30/MTok against $3.00/MTok uncached, a 90% reduction on those specific tokens.

If you are working: 90% off the cached tokens, then on the same 100,000-daily-call example, $900 a day drops to roughly $90 a day just on the compliance context.

One important thing to note, however, is that caching only works when the exact cached prefix repeats. Any change to that section, extra whitespace, reordered content, or a punctuation tweak causes a cache miss.

Most fintech teams that we have worked with default to one mid-tier or frontier model for every call, including plenty of simple tasks that a cheaper model handles just as well.

Opus-tier pricing runs roughly five times Haiku-tier pricing for the same volume, and it just isn’t necessary for everything.

The fintech routing matrix:

| Workload | Recommended tier | Why |

| Transaction document ingestion/extraction | Haiku | Structured extraction, deterministic output, no complex reasoning needed |

| KYC document validation (initial pass) | Haiku | Name, date, and ID pattern matching, deterministic |

| AML alert initial triage (suspicious / not) | Haiku, escalate unclear cases | Structured classification, escalate only what's actually unclear |

| Fraud pattern analysis (complex reasoning) | Sonnet | Multi-step reasoning at a cost-effective tier |

| Complex regulatory interpretation | Sonnet or Opus | Nuanced judgment justifies the upgrade against task complexity |

| Payment code generation (daily Claude Code use) | Sonnet | Best cost-to-capability ratio for routine coding |

| Architectural refactors (complex Claude Code use) | Opus | Large context and stronger reasoning justify the cost here |

| Compliance codebase audit (Claude Code agent) | Opus, with an explicit token budget | Needs the full context window, but needs a spending limit just as much |

What works well is to run an initial triage on the cheapest tier, escalate to the mid tier when confidence drops below a threshold, and reserve the top tier for cases that genuinely need complex multi-step reasoning.

AML transaction monitoring, fraud batch scoring, and compliance document analysis run large volumes of structurally similar calls with no real need for an instant response, but a lot of teams still run them synchronously at full price.

We recommend that you move anything latency-tolerant to the Message Batches API.

You should get a flat 50% off across every Claude model, with meaningfully higher output limits per request than the synchronous API, which makes batch particularly well-suited to long compliance document analysis.

Fintech workloads that fit this well:

Since output tokens cost several times more than input, a pipeline returning verbose JSON explanations when it only needs a classification and a confidence score is paying a real premium for tokens nobody actually reads.

Make sure to set an explicit output token cap on every call, since a model without one will often generate hundreds of tokens of explanation before it gets to the structured output you actually wanted.

Also, request a defined JSON schema rather than prose wherever the output feeds a downstream system rather than a human. For fraud alerts specifically, something like a decision, a confidence score, and a primary signal runs 30-50 tokens, against several hundred for a narrative explanation.

You can route the genuinely ambiguous cases to a human analyst who can ask for the narrative if they need it.

Where a model supports extended reasoning, keep it off for routine classification and reserve it for the handful of tasks where the reasoning quality difference is actually measurable, complex regulatory interpretation, not routine document validation.

Fintech codebases and compliance document libraries tend to run large.

Stuffing entire policy documents, full conversation histories, or whole codebase files into every prompt consumes tokens without affecting the actual output.

For compliance document Q&A, retrieval-augmented generation beats including full policy documents, embed the regulatory corpus, retrieve only a handful of chunks actually relevant to the query, and pass just those, which can cut per-request context tokens substantially on document-heavy workloads.

For Claude Code, you can cache the CLAUDE.md file and the service-level architecture context at the start of a session. For long conversations, summarize older turns before context pressure builds rather than carrying the entire history forward.

Claude Code does this automatically through auto-compaction, but custom workflows need it built in explicitly.

Also, make sure to trim tool schemas. MCP tool definitions sent on every call add real token weight, so load only the schemas the current task actually needs, rather than the full set by default.

Related Reading: Claude Code vs Cursor for Fintech Engineering Teams

Agentic workflows, a Claude Code compliance audit, an automated KYC pipeline review, and a multi-step fraud investigation agent run up several cost components at once.

This is for a variety of reasons, including a large context window, long reasoning loops, verbose tool output from file reads and command execution, and sometimes extended reasoning on top of all that.

Without explicit governance, a single compliance audit session can run $50 to $200 in API calls, an order of magnitude more than a typical request.

To prevent this, make sure to set workspace-level rate limits so an automated compliance audit agent can't quietly consume the budget meant for production workloads.

You can put explicit token budgets on any automated agent session, particularly ones triggered by CI/CD or scheduled jobs, rather than a human watching the session live.

Keep developer-facing Claude Code usage on a separate track from production API usage, so one doesn't eat into the other's budget without anyone noticing.

Another useful strategy our developers employ is to disable extended reasoning for routine tasks by default, saving it for the cases where the reasoning quality genuinely changes the outcome.

Without token-level visibility, there's no way to know which calls, workflows, or features are actually driving spend, or to confirm the optimizations above are working.

It’s worth setting up a tool like Langfuse or Phoenix to log token counts per request and aggregate by model, task type, and team, since this is what actually tells you which fintech AI workflow is your biggest cost driver before you go optimize the wrong one.

A proxy layer like LiteLLM is also a good idea if you're routing across multiple providers, since it handles cost tracking and per-user budget limits in one place. And for Claude Code specifically, the Claude Console gives workspace-level cost tracking with per-user attribution.

Instead of tracking cost per month, it’s more useful to track cost per business outcome.

Cost per KYC document verified, cost per AML alert triaged, cost per transaction screened, and cost per compliance audit completed tells you whether the spend is actually proportional to the value.

Not all seven levers carry equal weight, and doing them in a sensible order compounds the savings rather than just adding them up.

Start with prompt caching and output control. This has the lowest effort and highest immediate return.

Add cache_control breakpoints to every stable compliance system prompt, and make sure to set explicit output token caps on every call. Both changes are well under a day of engineering time each and typically cut costs 40-60% almost immediately.

Once that’s done, move to model routing and batch API.

Audit every AI call across the fintech stack and map each one to the routing matrix above. Move overnight AML screening, compliance document analysis, and non-urgent KYC verification onto the Batch API.

Finally, move to agent budget governance. For any team running Claude Code in CI/CD or for automated compliance audits, put workspace rate limits and per-session token budgets in place, and stand up Langfuse or Phoenix for token-level observability.

Token cost optimization in fintech is engineering work. You need engineers who not only understand the unique requirements of heavily regulated, production fintech environments, but also how AI token consumption works, and where they can realistically minimize spend without impacting users or developer productivity.

Trio places pre-vetted LATAM fintech engineers who understand both sides of this: the AI API mechanics, caching, batching, model routing, and the fintech domain context that actually determines which workloads are safe to route to a cheaper model.

If you are running AI at real scale, fraud detection, KYC screening, compliance monitoring, and AI-assisted code review, we can connect you with the right people in as little as 3-5 days.