Hire by Technology

SERVICES

Building a fintech marketplace means putting together a platform that connects businesses or consumers with financial service providers, whether lenders, insurers, payment processors, or credit scoring tools.

There are a couple of good examples that you can draw from for your own product. Lendio does this for small business loans, and NerdWallet built a comparison engine for financial products across categories.

A fintech marketplace model sits in a different category than simply embedding finance into your product.

You're not processing transactions yourself. You're building the layer that helps others find, compare, and connect to the providers who do.

In short, you need to think of it more like a marketplace business with a financial services supply side. That is all going to bring a distinct set of technical and regulatory challenges.

There are a couple of core decisions involved in actually building it: architecture, provider onboarding, API orchestration, compliance, and the monetization structures that tend to work at scale.

Having a fintech developer on your team, skilled not only in general development but with actual time in the financial services industry, can be a great asset.

If you want to find out if Trio is a good fit for you, view our capabilities.

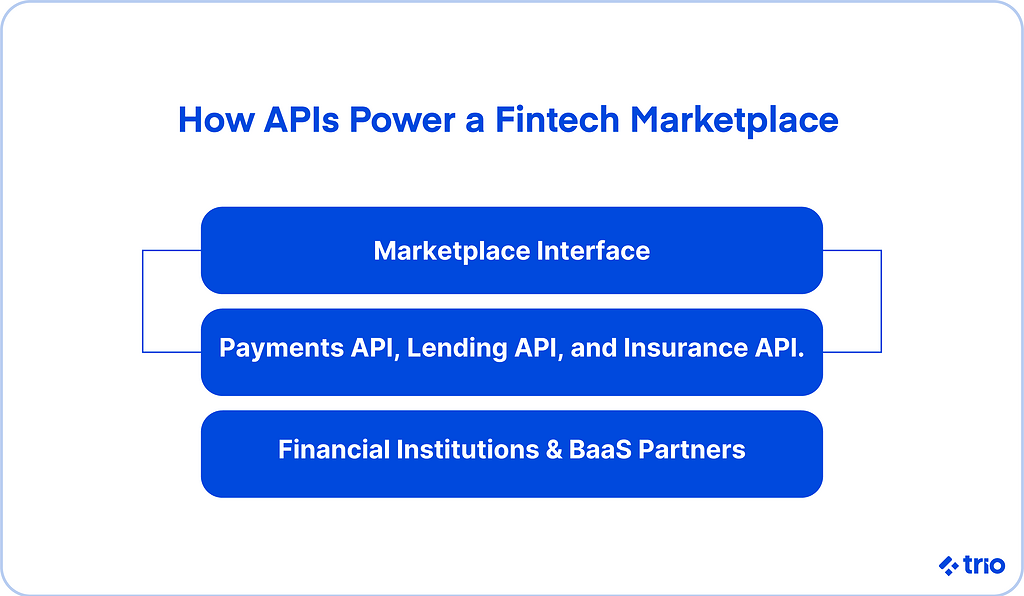

A fintech marketplace functions as an aggregation and matching layer.

Users arrive with a financial need, and the fintech marketplace platform connects them with one or more providers capable of meeting it.

The platform itself doesn't have banking licenses and doesn’t provide the services itself. Instead, it facilitates access.

You create a two-sided value proposition, reducing friction for users while creating distribution for providers.

Getting both sides working simultaneously is the biggest challenge that you are going to face.

Financial services tend to carry high customer acquisition costs. Supply can also be quite fragmented, and if users are not familiar with industry pricing, they may struggle with custom.

Those conditions make marketplace models very attractive.

A well-executed fintech marketplace can aggregate supply across dozens of providers and present it in a way that helps users make faster decisions. In doing so, you can earn a margin on each conversion without taking on too much risk.

That said, the opportunity varies considerably by subcategory. If you have a lending marketplace or offer any sort of lending services, you will probably have to deal with ongoing regulatory scrutiny of lead generation practices.

Insurance aggregators operate under state-level licensing requirements that differ significantly across the US. Payment provider comparison platforms tend to have lower barriers to entry but also lower monetization per transaction.

Related Reading: Embedded Payments for SaaS Platforms

Most fintech marketplaces share a common structural pattern, even when their supply side differs.

Understanding the best practices being formed and assessing the decisions being made by others can help you make informed decisions and potentially even help prevent tech debt.

The frontend handles everything that users see and interact with, including onboarding, profile collection, product comparison, and application flows.

In lending marketplaces, this typically means a multi-step application that collects financial data and presents matched offers.

In insurance aggregators specifically, a quoting interface is a great idea. You need to get this to update in real-time, though, and account for a variety of niche requirements.

The data you collect from users directly determines which providers you can route them to and how accurately you can match, making the initial user experience critical.

A form that collects too little produces weak matches. One that collects too much increases the chances of users leaving and potentially even opens you up to compliance issues.

Behind the frontend, an orchestration layer handles the actual routing logic.

When a user submits a loan application, the orchestration layer standardizes the data, figures out which lenders in your network meet the eligibility criteria, fires API calls to those lenders, collects responses, normalizes them into a consistent format, and surfaces the results.

From what we have seen, this layer is usually the most technically complex part of the platform, and the one that most teams underestimate in their initial scoping.

Each provider in your network will need to have a dedicated integration: authentication, request formatting, response parsing, error handling, and rate limiting, managed individually.

To make matters more difficult in terms of maintenance, provider APIs change, and documentation sometimes lags behind actual API behavior.

This means you are going to need engineers on your team pretty consistently.

Every piece of user data flowing through the platform requires handling in accordance with applicable regulations.

The compliance layer covers consent management, data storage policies, KYC and AML checks where required, and audit trail generation.

A lot of companies do not want to build this in from the start due to budget constraints. But retrofitting your compliance later costs a lot more, particularly if you are trying to get it done quickly before an audit or something like a finding layer.

Getting your first ten providers onto the platform may be quite challenging, particularly if you do not have existing connections in the fintech industry.

Provider onboarding in financial services involves legal negotiations, compliance reviews, API access agreements, data sharing contracts, and, in some cases, licensing checks.

Large financial institutions move slowly. Their vendor review processes can take months and may require evidence of your security controls and your data handling policies.

Smaller fintech lenders and insurtech providers tend to move faster, which may make it easier to start with non-bank or fintech-native providers before pursuing traditional bank relationships.

A few things tend to accelerate the process.

The supply side of your marketplace also shapes your monetization options directly, which makes provider selection a business model decision as much as a technical one.

Once you have more than a handful of providers integrated, orchestration becomes the defining technical challenge.

The goal of matching users and providers is to match each user with the provider for a successful conversion. It seems simple. But the execution requires several things working simultaneously.

Data normalization sits at the foundation.

Your orchestration layer needs to translate a single user profile into the input format each provider's API expects, and those formats can differ significantly across lenders or insurers, which you will need to account for.

Routing logic determines which providers receive each application. We recommend that you start with rules-based routing (minimum credit score, business age, loan size).

Once you have that in place, you could implement some of the latest trends around routing, namely, machine learning and AI.

If you are able to gather enough information, you could eventually even move towards predictive modeling.

Consider what happens next. You need to communicate decisions to your users, but different platforms might not necessarily all provide said answers at the same time. Response handling is the solution.

Some providers return a decision in seconds. Others fire a webhook hours later. Holding session state across asynchronous responses without creating a confusing user experience takes careful design.

To keep clients for as long as possible, even when providers decline, you could implement fallback logic.

The orchestration layer should automatically route to the next eligible provider without requiring your user to start over.

If you do not have this talent on board or cannot afford the time and resources to build from scratch, platforms like Alloy and Blend offer orchestration infrastructure specifically for lending, which can reduce the time spent building this logic from scratch.

The regulatory surface area of a fintech marketplace expands with every provider category you add. Every different sub-section of fintech has distinct obligations.

The monetization model you choose affects your revenue, your regulatory positioning, your relationship with providers, and your incentives around user outcomes.

This is the most common model. You earn a fee when a user converts with a provider in your network.

The advantage lies in simplicity and low implementation friction. Even those who have never worked on a marketplace before can understand their potential income with relative ease.

The risk, particularly in consumer lending, involves regulatory scrutiny around whether referral fees create incentives that work against consumers.

Disclosing your commercial relationships clearly appears increasingly important as CFPB oversight of comparison platforms grows.

Rather than a flat referral fee, we’ve seen some marketplaces that earn a percentage of the transaction value when a user converts.

Aligning your revenue with the quality of the match tends to create better incentives around routing logic, but it also makes revenue per conversion harder to forecast.

Charging providers a subscription fee for platform access, rather than transaction-based fees, provides more predictable revenue and reduces the conflict of interest that can arise from pure referral structures.

This is a great option if you have a consistent user base, but it really only works if you are able to provide a continuous service of some sort and provide value over time.

Building the marketplace infrastructure and licensing it to financial institutions or other companies represents a fourth path.

If your orchestration and provider integration work genuinely sets you apart technically, then licensing it may create more durable value than operating the consumer-facing marketplace yourself.

A great example of this is Plaid, which, while not strictly a marketplace, has built significant revenue by providing the infrastructure layer that other fintech products depend on.

There are a couple of great examples of fintech marketplaces that are worth having a look at, so that you can not only set yourself apart, but also see what is working well for potential users.

Lendio aggregates over 75 lenders for small business loans.

It’s a particularly good example of user experience since it successfully collects a single application, routes it across the network, and surfaces ranked offers.

Their model is also an incredible practical instance of multi-lender orchestration. A declined application at one lender becomes an approval at another, and the borrower never encounters the routing complexity underneath.

NerdWallet's comparison model across credit cards, loans, savings accounts, and even insurance illustrates a content-driven conversion funnel that starts well before the comparison page.

While you may not be interested in driving conversions this way, itappears to be a meaningful part of why their acquisition economics work and is a valuable option to consider when you are first starting out.

Policygenius built an insurance marketplace by combining a digital comparison engine with licensed human advisors for complex products like life and disability insurance.

The hybrid model addresses the fact that some financial products require explanation before a user will feel confident enough to convert.

Building a fintech marketplace with a clear plan and a good idea of the desired outcome you want can greatly improve the process.

Before writing significant code, confirm that providers will actually integrate with your marketplace.

Preliminary conversations with five to ten potential providers, including a discussion of API access and commercial terms, will give you an idea of potential blockers early on so that you can deal with them effectively.

Starting with two or three integrated providers forces your orchestration architecture to handle the core routing and normalization problems without the complexity of managing a large network.

The patterns you establish with only a couple of providers will scale. If you start with ten or twenty, you might generate technical debt that compounds in an effort to handle everything at once.

Compliance architecture takes time to do correctly.

Running it in parallel with product development keeps your timeline realistic and your legal exposure manageable.

Getting compliance or RegTech experts on your team can help with this.

Once your first provider integrations run in a sandbox environment, test the quality of your matching logic before driving real users through it.

Poor matches damage provider relationships and user trust at the same time, both of which take significant effort to rebuild.

Conversion rate by provider, decline rate by user segment, average time to decision, API error rates, and more can be tracked to give you the data you need to improve routing logic and identify provider integration problems before they affect user experience at scale.

Teams that add instrumentation later tend to make decisions on incomplete information during the months that matter most. This leads to wasted time and money, and can sometimes even lead to a bad reputation if issues appear in front of users.

A few structural shifts appear likely to shape the category over the next several years.

Open banking regulation, already further along in the UK and EU than in the US, may eventually give fintech marketplaces easier access to verified financial data.

Faster and more reliable data access tends to improve match quality and reduce application friction for users, which would benefit most marketplace models.

AI-assisted matching is also very quickly becoming a baseline expectation so that platforms can predict approval likelihood and offer quality across their provider network with reasonable accuracy.

Building toward this capability requires collecting and structuring approval outcome data from day one, which makes instrumentation an even more important early decision.

Verticalization is another thing we are seeing more of.

Rather than broad financial product comparison across categories, newer entrants tend to focus on a specific user segment, freelancers, immigrants, small business owners in specific industries, and build a marketplace tailored to providers who serve that segment well.

Building a fintech marketplace means solving a two-sided market with users and providers successfully in one of the most regulated industries out there.

If you're working through the architecture, the provider strategy, or the compliance questions involved in building your marketplace, Trio's engineers have worked across payments, lending, banking, and insurtech.

Request a consult.

A fintech marketplace connects users with financial service providers through a centralized platform, usually only requiring one set of information from users to provide them with a variety of options.

Rather than offering financial products directly, fintech marketplaces earn revenue by facilitating those connections. One of the most common monetization models is referral fees.

You only need two or three integrated providers to launch your fintech marketplace. This appears more effective than waiting until you've built a large network, because a small, well-matched supply side lets you validate routing logic.

The timeline to build a fintech marketplace depends on the number of provider integrations and the complexity of your compliance architecture. A focused MVP with two to three provider integrations and a solid compliance layer typically takes four to eight months.

Some of the best examples of fintech marketplaces include NerdWallet and Lendio. These platforms solve real-user issues with optimized lead generation and routing systems.