Hire by Technology

SERVICES

Fintech compliance costs significantly exceed the audit fee. For a startup needing SOC 2 Type II and PCI DSS SAQ D, total first-year spend can reach as much as $120K–$250K when including engineering implementation, readiness assessment, audit fees, tooling, and penetration testing.

The audit fee is only 15–30% of this total, so treating the audit fee as the compliance cost will result in massive underbudgeting, which is difficult to explain to investors, and may result in massive compliance issues that may even sink smaller issues.

Let’s look at everything you need to know about security and compliance costs for fintech, including regulations like SOC 2, PCI DSS, KYC/AML, and DORA, with specific ranges calibrated to fintech startup and growth-stage contexts in 2026.

At Trio, we have pre-vetted fintech specialists with extensive production experience in these regulated markets. These developers can be placed in as little as 3-5 days.

Book a security-ready consult.

Not every fintech needs every framework. Understanding which frameworks your product, market, and customer base trigger will help you to prevent investing in certifications you don't need, and missing the ones that you actually do.

| Framework | Triggered by | Not required when |

| PCI DSS | Storing, processing, or transmitting payment card data. | Using fully hosted payment pages (Stripe Elements, Adyen Drop-in) results in SAQ A only. |

| SOC 2 Type II | Enterprise customers’ and banking partners' requests and requirements, fundraising due diligence. | Pre-product or consumer-only products with no enterprise buyers. |

| KYC/AML (FinCEN/BSA) | Money transmission, account opening, crypto operations, and B2B payments. | Read-only data aggregation products that don't move money. |

| GDPR | Processing personal data of EU residents. | US-only operations with no EU user data. |

| DORA | EU-licensed payment institutions, credit institutions, investment firms, and their critical ICT providers. | US-only fintechs with no EU operating entity or EU financial institution customers. |

| ISO 27001 | Banking partner contracts, enterprise procurement, and government financial contracts. | This is rarely mandatory. Most fintechs prioritise SOC 2 as the primary information security certification. |

| SR 11-7 | AI/ML models influencing financial decisions at Fed/OCC-supervised institutions. | Fintechs without AI/ML in credit scoring, fraud detection, or financial risk models. |

The minimum viable compliance stack for most US consumer fintechs handling card data and targeting enterprise buyers is PCI DSS, SOC 2 Type II, and KYC/AML.

Each of these has a distinct cost profile and engineering implementation requirement.

SOC 2 is the information security attestation that we see most commonly required by enterprise fintech buyers and banking partners.

An SOC 2 report acts as proof that your company's internal controls for security operated effectively over a defined period.

Optionally, it also gives an indication of availability, confidentiality, processing integrity, and privacy.

SOC 2 Type I evaluates whether your controls are designed correctly at a specific date.

Type II evaluates whether controls operated effectively over a defined period, typically 6–12 months.

The 6-month minimum observation period for Type II is fixed. Since there is nothing you can do to accelerate it, you should begin planning as early as possible to make sure that it doesn’t affect your fundraising timelines, banking partner onboarding, and enterprise sales cycles.

| Cost component | Typical range |

| Readiness assessment (gap analysis) | $10K–$25K |

| Control implementation engineering | $15K–$40K |

| Compliance automation platform (Vanta, Drata, Thoropass, Secureframe) | $5K–$20K/year |

| Penetration testing | $10K–$20K |

| Type I audit fee | $10K–$25K |

| Type II audit fee | $15K–$50K |

| Legal review (vendor contracts, employee agreements) | $5K–$15K |

| Internal engineering time (opportunity cost) | $20K–$60K |

| Total: Type I first year (startup) | $40K–$100K |

| Total: Type II first year (startup) | $60K–$150K |

Annual renewal cost once the baseline is established runs at around $25K–$60K/year. Most of this is made up of the ongoing audit fee ($10K–$25K), platform subscription, and penetration test.

Internal engineering time is one of the most expensive costs we see our clients exclude from compliance budgets.

Configuring evidence collection, remediating control gaps, updating access management, implementing logging infrastructure, and managing audit preparation typically consumes 200–400 engineering hours.

This makes it a $20K–$60K opportunity cost for senior fintech engineering teams.

Compliance automation platforms like Vanta, Drata, and Thoropass can help you reduce this significantly by automating evidence collection from cloud infrastructure, but you still need some level of implementation engineering.

Each criterion beyond security, such as availability, confidentiality, processing integrity, and even privacy, adds 20–30% to audit scope and cost.

Privacy is the most expensive, regularly adding up to 50% for our clients.

Most early-stage fintechs focus on security, and add criteria only as enterprise customers require them.

From what we have seen, banking partners occasionally require availability, while healthcare-adjacent fintech products frequently trigger Privacy.

In recent years, competition among compliance automation platforms has driven prices down considerably.

Secureframe, for example, is currently pricing at minimums around $7K/year for startups. Vanta and Drata typically quote higher but are willing to negotiate or provide discounts for smaller teams.

Even if the possibility of negotiations is not expressly advertised, it is worth asking about.

PCI DSS is mandatory for any fintech that stores, processes, or transmits payment card data.

Version 4.0, with all future-dated requirements effective March 2025, introduced more rigorous penetration testing requirements, continuous monitoring obligations, and expanded authentication standards.

The cardholder data environment (CDE), or the systems in scope for PCI DSS, is primarily shaped by the architectural decision of whether card data ever touches your systems directly.

Using a hosted payment page (Stripe Elements, Adyen Web Drop-in) means card data flows directly from the customer's browser to the PSP, so your systems never see it.

This qualifies for SAQ A, the lightest compliance path.

Building a custom card entry form where card data passes through your servers dramatically expands the scope to SAQ D or a full QSA assessment, which costs 4×–5× as much.

| Level / SAQ type | Who it applies to | Total first-year cost range |

| SAQ A (hosted payment pages) | Fintechs using Stripe Elements, Adyen Drop-in, etc. | $8K–$20K |

| SAQ B/B-IP (card-present via approved devices) | Limited card-present implementations | $15K–$35K |

| SAQ D (merchants processing their own card data) | Custom card capture forms, stored card data | $40K–$80K |

| Level 2 (1M–6M transactions): SAQ + QSA oversight | Mid-volume card processors | $30K–$80K |

| Level 1 (>6M transactions): full QSA RoC audit | High-volume card processors | $70K–$200K |

Scope creep causes 30–50% cost inflation on its own, according to RedSecLabs' 2026 data.

Systems that appear outside the CDE scope at the start frequently surface as in scope during the QSA assessment. Some of the common examples we see of this include application logs capturing partial card data, development environments with production data copies, and email archives containing card data.

A pre-audit scoping engagement, with a QSA, typically costs $3K–$8K. But it is often the more cost-effective option as it prevents $12K–$25K+ in mid-audit remediation surprises.

| Annual cost component | Typical range |

| QSA annual assessment or SAQ renewal | $5K–$100K (depends on level) |

| Quarterly ASV vulnerability scans | $4K–$20K/year |

| Annual penetration test (required under PCI DSS 4.0 for SAQ D and above) | $8K–$30K |

| SIEM/continuous monitoring infrastructure | $5K–$50K/year |

| Annual recurring total (SAQ A to Level 1) | $22K–$200K/year |

KYC and AML obligations under the Bank Secrecy Act and FinCEN rules apply to most fintechs that move money, open accounts, or operate as money services businesses. It is primarily an engineering cost.

The primary regulatory requirement is to have functioning systems, not to receive a third-party certification.

Designing KYC as a stateful system with lifecycle management adds $20K–$40K to the initial engineering scope compared to a simple boolean is_verified flag. Most developers without fintech compliance experience default to the Boolean because it is simpler.

However, even though this is cheaper upfront, if a QSA or regulatory examiner who reviews the system finds that a boolean flag doesn't maintain the stateful audit trail that AML rules require, you’ll need to retrofit a proper KYC state machine post-audit.

This costs $50K–$120K in re-architecture, data migration, re-certification, and the re-engagement fees for engineers who have left the project.

DORA (Digital Operational Resilience Act, Regulation EU 2022/2554) has been enforceable since January 17, 2025.

It only applies to financial entities operating in the EU and their critical ICT service providers.

Nineteen ICT providers (including AWS, Microsoft Azure, and Google Cloud) have been designated as critical and are subject to direct EU supervisory oversight since November 2025.

Penalties are serious, including10% of annual global turnover or €10 million for serious breaches (whichever is higher), and even €1 million for personal accountability failures of senior managers.

Most fintechs need more than one framework, but the combined cost is not simply additive.

PCI DSS and SOC 2 share approximately 60% of their control requirements. Running them simultaneously rather than sequentially saves 20–30% of the combined cost.

Similarly, DORA and SOC 2 availability and confidentiality criteria overlap significantly for ICT risk management and incident response.

Here is a combined first-year compliance budget:

| Fintech profile | Required frameworks | First-year budget range |

| US payment app (Stripe-based, SAQ A, pre-enterprise) | PCI DSS SAQ A + KYC/AML | $60K–$130K |

| US payment platform (own card capture, enterprise customers) | PCI DSS SAQ D + SOC 2 Type II + KYC/AML | $150K–$320K |

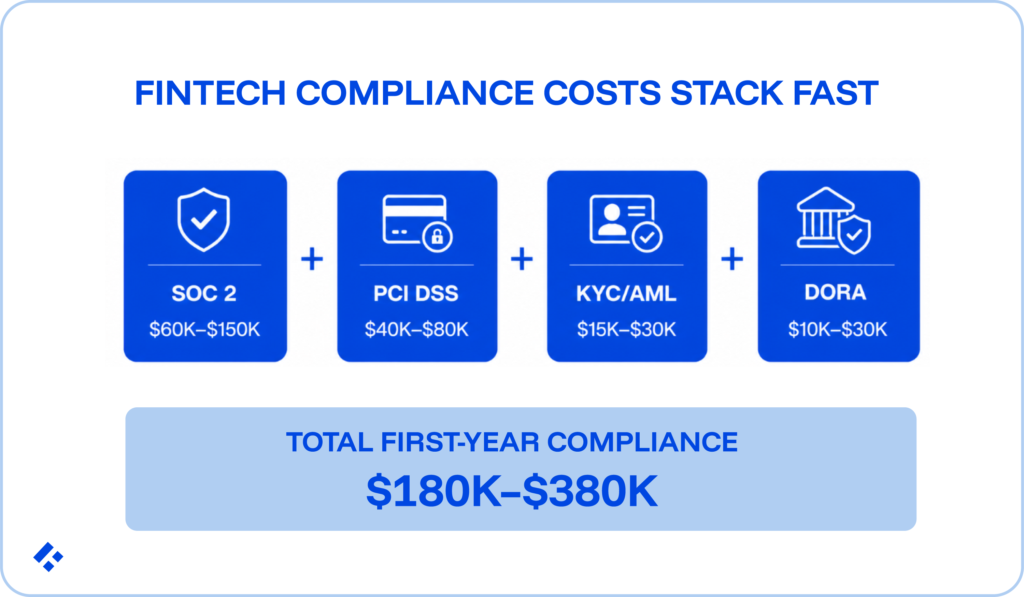

| US neobank (BaaS-based, banking partner required) | PCI DSS SAQ D + SOC 2 Type II + KYC/AML | $180K–$380K |

| EU payment institution (DORA-subject, enterprise) | PCI DSS + SOC 2 + KYC/AML + DORA + GDPR | $250K–$500K |

| AI-enabled credit platform | PCI DSS + SOC 2 + KYC/AML + SR 11-7 governance | $180K–$400K |

We have already mentioned that compliance controls cost three to five times more to retrofit than to build into the architecture from the start. This ratio is the single most important variable in determining the true total cost of a fintech's compliance program.

| Compliance control | Build-in cost | Retrofit cost | Multiplier |

| Audit trail / immutable logging infrastructure | $10K–$20K | $25K–$60K | 2×–4× |

| KYC state machine (vs. boolean flag) | $20K–$35K | $50K–$120K | 2.5×–4× |

| PCI DSS scope architecture (hosted vs. custom card capture) | $5K–$10K decision overhead | $30K–$80K to migrate to hosted | 6×–8× |

| Monetary precision (DECIMAL vs. FLOAT design decision) | $0 | $30K–$60K data migration under load | ∞ |

| SR 11-7 model documentation infrastructure | $15K–$25K | $40K–$80K | 3×–4× |

The two-week discovery phase at the start of a fintech development engagement is the point at which compliance requirements should map to engineering decisions.

Compliance is an annual cycle. There are fixed milestones and ongoing engineering maintenance obligations that need to be met.

If your fintech achieves SOC 2 Type II and PCI DSS, you will need to budget for it every year to keep that certification.

| Period | Activity | Engineering involvement | Estimated cost |

| Q1 | SOC 2 annual evidence preparation and audit | 2–4 weeks of engineering | $10K–$25K (audit) |

| Q1 | PCI DSS quarterly ASV scan | DevOps: 1 day | $1K–$5K |

| Q1–Q2 | Annual penetration test (PCI DSS + SOC 2) | Engineering: remediation of findings | $10K–$30K |

| Q2 | PCI DSS quarterly ASV scan | DevOps: 1 day | $1K–$5K |

| Q2–Q3 | SOC 2 observation period monitoring | Ongoing: automated evidence collection | $5K–$20K (platform) |

| Q3 | PCI DSS quarterly ASV scan | DevOps: 1 day | $1K–$5K |

| Q4 | PCI DSS quarterly ASV scan + annual SAQ renewal | Engineering: review and update | $5K–$20K |

| Ongoing | KYC/AML transaction monitoring, SAR filing | Ongoing: compliance ops + engineering | $15K–$80K/year |

| Ongoing | Security patch management, access reviews | Engineering: monthly cycle | $10K–$30K/year |

Annual total for a mid-market US fintech (SOC 2 Type II + PCI DSS SAQ D) is typically around $60K–$200K/year in direct costs, plus $30K–$80K/year in internal engineering time at opportunity cost.

A fintech compliance program is an engineering infrastructure project that the compliance team governs. The engineering work falls into three categories that must be resourced like product work:

The difference between a team that builds compliance in from the start and a team that retrofits it is usually domain experience.

Engineers who have shipped production fintech systems know which architectural decisions carry compliance consequences before they make them, and can adjust to minimize your total cost, as well as alert you to those requirements as decisions are being made.

At Trio, we place compliance-aware fintech engineers with production experience in payment systems, KYC/AML, PCI DSS architecture, and DORA requirements.

Since these engineers are pre-vetted, you don’t have to go through an extensive hiring process, but can instead bring them into your team in as little as 3-5 days.