Hire by Technology

SERVICES

Knowing how long you are looking at is essential for budgeting, as well as managing user and investor expectations. Fintech software development timelines range from 3 months for a narrow-scope MVP to 18 months for a licensed digital bank.

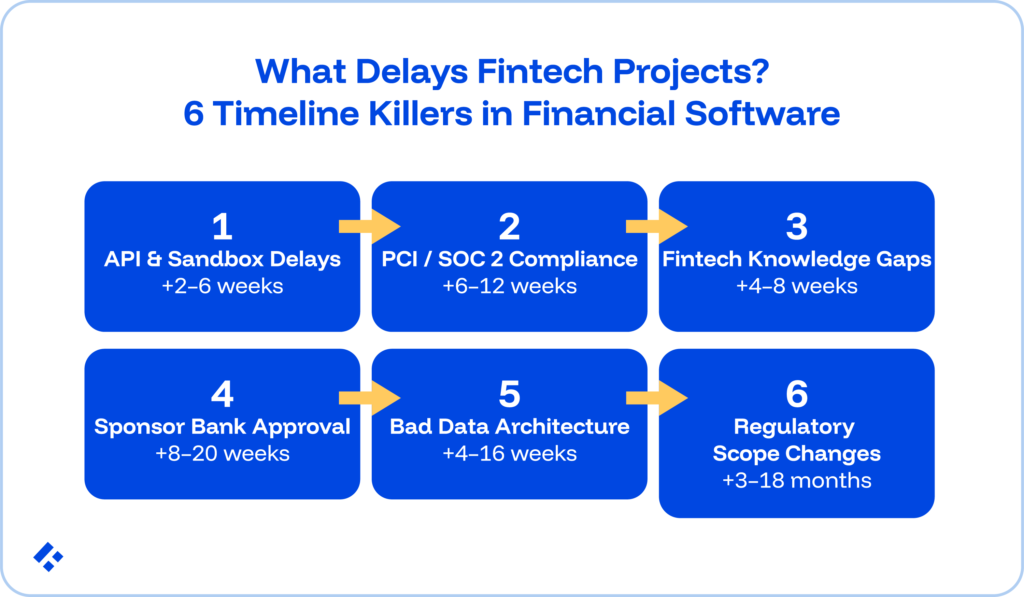

There are six categories we have identified that drive fintech software development timeline variation:

Issues related to these factors surface on almost every fintech build. Teams that know about them before the project starts are more likely to build realistic schedules. Teams that discover them mid-execution slip, sometimes by months. Let’s look at the mechanism behind each delay, the typical slip duration, and what experienced fintech teams actually do to mitigate them.

If you are interested in production-experienced fintech developers who can help you prepare for and avoid these issues entirely, we can help.

Most fintech timeline estimates use a framework that looks like this:

These ranges hold up in aggregate, but they can’t really be used for planning a specific project because of the sheer number of factors they rely on.

The 3–6 month MVP estimate, for example, assumes a scope focused enough to avoid compliance-sensitive data, a BaaS provider already contracted with onboarding complete, an engineering team carrying prior fintech domain experience, no new regulatory licensing required, and third-party API sandboxes available on day one.

Fintech products run on integrations. A typical payment-enabled MVP that our developers get added onto usually connects to a KYC provider, a payment processor, a BaaS provider or card issuer, and often a banking data aggregator.

Each of these integrations requires a working sandbox environment before development and testing can proceed. And sandbox provisioning is not instant.

Different providers carry very different provisioning timelines:

A team that begins development assuming sandbox access in week one and discovers an unexpected provisioning timeline loses all of the time it takes for that integration work across the schedule, with no way to recover it in parallel.

Even when sandboxes arrive on time, sandbox behavior is rarely exactly the same as production. How exactly it differs only really shows up when you get to your final testing, though.

Webhook retry behavior, error code granularity, and edge-case response formats often differ between environments.

Typical slip duration: We estimate about 2–6 weeks per major third-party integration, compounded when multiple integrations sit on parallel critical paths.

Mitigation: File all third-party API applications and sandbox provisioning requests on day one of the project.

Compliance certifications in fintech carry two properties that general software security reviews don't. First, they depend on external parties (a QSA, a penetration tester, a regulator), and they also have minimum lead times that internal resources cannot compress by adding headcount.

Most fintech projects treat compliance certification as a pre-launch gate if they haven’t worked on these kinds of projects before and don’t understand the delays that can result.

Mitigation: You need to determine PCI DSS scope on day one, because scope affects most architecture decisions.

The regulatory and financial system conventions shaping every significant architectural decision take time to acquire for engineers who haven't built regulated financial systems before.

A skilled engineer without fintech domain experience typically requires 4–8 weeks to reach compliance-aware productive velocity on a regulated fintech system.

This is not the only delay to consider, though.

During this period, they can contribute to general engineering tasks but not to compliance-sensitive components. If they do, they are at risk of making mistakes that add even more time later.

Typical slip duration: 4–8 weeks per engineer without domain experience.

Mitigation: Pre-vet engineering partners and contractors specifically for the fintech domain experience.

For fintechs operating through a sponsor bank relationship, which is one of the most common structures for US consumer fintechs at MVP that we have come across, the sponsor bank and BaaS provider sit on the project's critical path for launch.

There is very little that your engineers can do to accelerate a sponsor bank's compliance review.

Card program approval cannot begin until BIN sponsorship is confirmed. BIN sponsorship cannot begin until the sponsor bank relationship is established.

If your team doesn’t know about all of this and only discovers the sequencing in month three, you are facing a 6+ month cascade with no parallel path available.

Sponsor bank selection warrants the same diligence as any critical technology vendor.

For example, during the Synapse period, the banks Synapse partnered with received enforcement actions from federal regulators.

Typical slip duration: 8–20 weeks if the sponsor bank onboarding starts after engineering begins, rather than in parallel with it.

Mitigation: You need to begin the sponsor bank and BaaS provider application processes when you start engineering.

Three data architecture decisions in fintech cost 2–4 weeks to make correctly at the start of a project and 4–16 weeks to correct post-production.

None of them appear in generic project checklists, and engineers without fintech production experience frequently make the wrong choice on all three.

Storing financial amounts as floating-point numbers (FLOAT, DOUBLE) rather than fixed-precision types (NUMERIC/DECIMAL in PostgreSQL, or integer minor-unit representations) creates rounding errors that compound at transaction volume.

Discovering this after the system has processed real transactions requires a data migration under production load.

This is a 4–6 week engineering project on its own, with significant data integrity risk.

Building a mutable balance column rather than a double-entry immutable journal means any concurrent write, partial failure, or manual correction can create balance drift.

Migrating from a mutable-balance system to a proper double-entry ledger after real customers have real balances is a multi-month re-architecture project that generally cannot run without a maintenance window.

Many fintech products that we have worked with cannot accommodate this window.

Application logs don't satisfy regulatory evidentiary requirements. Instead, a proper audit trail requires immutable, append-only records carrying specific fields (who, what, when, which system version) that can answer questions under regulatory examination.

Building this correctly from day one adds 2–4 weeks of engineering.

However, this is far shorter than retrofitting it after a compliance review flags the gap, which adds 6–10 weeks, often with a remediation timeline tied to an external auditor's schedule.

Typical slip duration: 4–16 weeks when a foundational data architecture decision requires correction post-production, plus the risk of a production incident during migration.

Mitigation: Architectural review of monetary precision, ledger design, and audit trail schema as a mandatory pre-build checklist item, completed before the data model finalises.

Fintech projects regularly encounter regulatory requirements that weren't visible at project start, simply because the regulatory landscape is complex enough that requirements surface during development that genuine pre-build due diligence doesn't always catch.

Each discovery event affects your timeline individually.

This means that, when three or four discovery events happen across a six-month project, each one can add 3–8 weeks, which can put you massively behind, sometimes even doubling the original schedule, even when every sprint is executed cleanly.

Pre-build regulatory mapping. You need to create a documented assessment of which jurisdictions the product operates in, what requirements apply in each, and which third-party providers are compliant with each requirement.

This typically takes 2–3 weeks at project start, but it is well worth it if this allows you to avoid 12–20 weeks of delays in the middle of your project.

Let’s look at some of the most common fintech product types in terms of timeline estimates under two risk profiles. Low risk means all six factors we mentioned above have been mitigated proactively. High risk means factors discovered during execution rather than before it.

| Product Type | Low Risk Timeline | High Risk Timeline | Primary Timeline Drivers |

| Payment-enabled MVP (Stripe/Adyen, no stored financial data) | 10–14 weeks | 20–28 weeks | PCI DSS SAQ, API sandbox, domain ramp |

| Consumer fintech with KYC/AML (account + payments) | 4–6 months | 9–14 months | BaaS onboarding, KYC state machine, compliance certifications |

| Card-issuing product (debit or prepaid) | 5–8 months | 10–16 months | Card program approval, BIN setup, sponsor bank review |

| Lending platform (regulated consumer credit) | 6–9 months | 12–18 months | State licensing, ECOA/FCRA compliance, and underwriting model documentation |

| Neobank (full digital banking product) | 10–16 months | 18–36 months | Banking license or BaaS multi-party onboarding, core banking, compliance infrastructure |

| B2B payments infrastructure | 4–7 months | 9–14 months | PSP certification, sponsor bank, multi-jurisdiction data residency |

Related Reading: How to Hit Roadmap Deadlines Without Hiring

Every mitigation described in every instance we spoke about above requires skilled software engineers.

This means that team composition is one of the highest-leverage inputs to the fintech project timeline.

Eliminating the 4–8 week compliance ramp per engineer is entirely in your power if you have the time to invest in thorough vetting before hiring.

However, many companies need to scale faster than traditional hiring allows. That’s where our services come in.

Trio places pre-vetted fintech engineers with production fintech experience across payment systems, KYC/AML, PCI DSS, and compliance-aware architecture. This means you can get the right developer on your team in as little as 3-5 days.