Hire by Technology

SERVICES

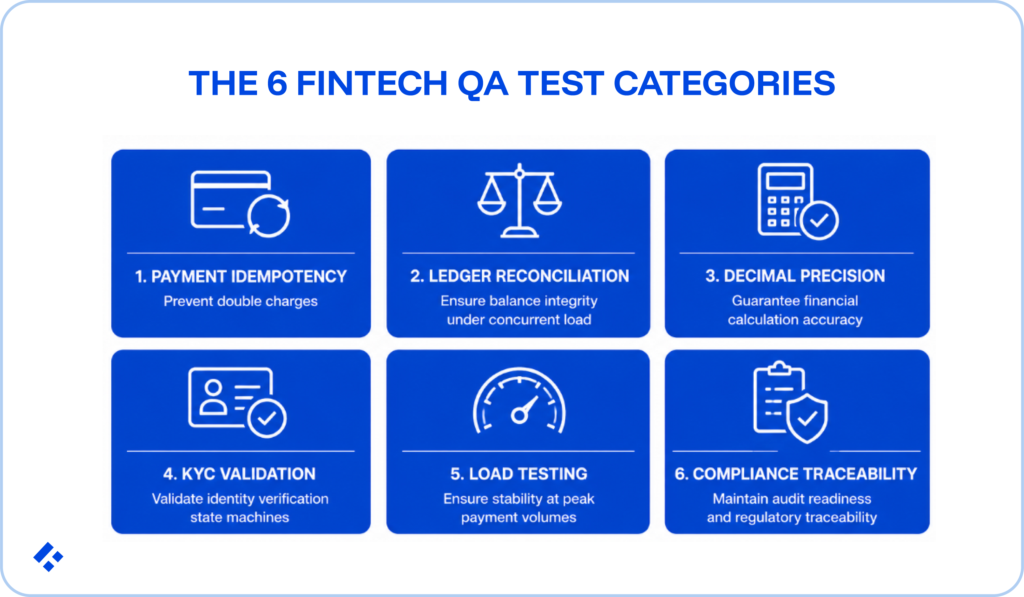

Fintech QA costs 25–35% of the total development budget. This is considerably higher than the 20–30% general software benchmark.

This is largely due to 6 fintech-specific test categories:

Each adds a cost that standard QA budgets don't account for. Failing to budget correctly leads to misallocated funds, which end up forcing you into tech debt that shows up during compliance audits or results in costly client remediation and loss of reputation.

This article prices each fintech-specific test category, provides a complete QA budget model by company stage, and explains where the typical fintech QA underinvestment occurs.

At Trio, our QA developers are pre-vetted for fintech production experience and can assist you in the relevant testing both retrospectively and throughout the development process.

General software QA benchmarks (20–30% of development budget) apply to products where a production bug degrades user experience, but nothing else.

Fintech QA benchmarks run higher because a production bug may simultaneously degrade user experience, double-charge customers, corrupt ledger balances, violate AML monitoring obligations, or trigger a regulatory finding.

Since these are unique to fintech, the test coverage required to prevent them doesn't appear in general QA frameworks either.

As we have already mentioned, six test categories in fintech require purpose-built suites that general software QA frameworks don't generate automatically.

Each adds to the QA budget above the general software baseline because the failure modes being guarded against are different from anything a general testing approach anticipates.

Idempotency testing validates the payment retry scenario.

This is where a charge is processed at the PSP, but the confirmation response is lost in transit, and without a correct idempotency implementation, the customer gets double-charged on retry.

Testing this failure mode requires deliberately triggering it by simulating PSP acknowledgment without database write completion. You need to verify that the retry produces a record lookup rather than a new charge.

This isn't a standard API integration test, since it requires infrastructure that can simulate partial failures at specific points in the payment execution sequence, namely, between PSP confirmation and database write, between webhook receipt and processing, and between ledger entry and confirmation response.

Building that infrastructure requires QA engineers who understand payment system architecture.

What it includes:

Typical cost to build: $15K–$35K in engineering time (3–6 weeks of senior QA or backend engineering).

Annual maintenance: 10–15% of initial build cost.

What it prevents: Customer double-charge incidents costing $50–$500 per affected transaction in remediation, plus regulatory scrutiny overhead.

Ledger reconciliation testing verifies whether the financial ledger maintains integrity under concurrent write load.

It checks for correct balances, ensures no floating-point arithmetic errors, and makes sure there is no race condition balance drift.

A ledger that balances correctly in single-threaded testing may produce discrepancies under the concurrent write patterns of real production traffic.

What it includes:

Typical cost to build: $10K–$25K initial (2–4 weeks of QA and DevOps engineering for test infrastructure).

Load test infrastructure: $500–$2,000/month in cloud compute during active test cycles.

Decimal precision testing covers every financial calculation path in the codebase for floating-point arithmetic errors.

This specific failure occurs because monetary amounts stored as FLOAT or DOUBLE cannot represent many decimal fractions exactly in IEEE 754 arithmetic.

Testing for it requires QA engineers who know how to look for it, test cases designed around specific IEEE 754 edge cases, and coverage across every calculation path.

What it includes:

Typical cost to build: $8K–$18K (1.5–3 weeks of senior QA engineering), largely as a one-time investment with low ongoing maintenance costs.

KYC state machine testing covers the completeness and correctness of the identity verification lifecycle.

Specifically, it ensures that every state transition is tested, invalid transitions are rejected, EDD triggers fire correctly, and ongoing monitoring re-screens customers when risk indicators change.

A kyc_verified boolean has two states and two tests.

A proper KYC state machine with 8–12 states, multiple valid and invalid transition paths, and ongoing monitoring triggers has hundreds of test scenarios.

Missing test coverage for an invalid KYC state transition is a regulatory gap that surfaces in an AML examination, often 12–18 months after the code was written.

What it includes:

Typical cost to build: $20K–$45K (3–7 weeks of senior QA and compliance-aware engineering).

Annual maintenance: 20–25% of initial build cost.

Payment load testing verifies system behaviour under the load patterns specific to payment processing, like massive spikes around weekends and holidays.

General load testing generates uniform requests, while payment load testing requires realistic transaction volume distributions, correlated spike scenarios, and SLO validation against financial thresholds.

What it includes:

Tooling: k6 (open source, preferred for scripting complexity), Gatling (JVM-based, preferred for enterprise), Artillery (lightweight, API-focused).

Typical cost: $10K–$25K initial build. $500–$3,000/month for load generation infrastructure during test campaigns. $5K–$15K per quarterly load test campaign ongoing.

Compliance traceability testing verifies that the system's audit trail is complete, correct, and queryable.

You need to confirm that every logged record needs to contain the fields required by the applicable compliance framework (PCI DSS, SOC 2, SR 11-7) and ensure that the log infrastructure functions as a compliance control.

It requires engineers who understand the regulatory requirement being tested, who understand what immutability looks like.

What it includes:

Typical cost to build: $12K–$28K (2–4 weeks of QA and compliance-aware engineering).

Annual maintenance: $5K–$15K/year as compliance requirements evolve.

Without automation, a fintech regression cycle takes roughly 10 working days of manual testing.

However, with a properly built automation suite, the same cycle can run in approximately 3 hours, with 2 days of residual exploratory testing.

This means that each regression cycle saves approximately 7 working days of QA engineering time, which at a LATAM nearshore rate of $50–$80/hr translates to $2,800–$4,480 per cycle.

At bi-weekly releases, automation pays for its initial build cost within as little as 4–6 months.

| Framework | Licensing | Best for | Fintech suitability |

| Playwright | Free (open source) | Web UI, API, cross-browser | Best overall. 42% faster than Selenium, 67% fewer flaky tests per TestDino 2025. Actively maintained. |

| Cypress | Free; Cloud $67+/month | Web UI, component testing | Strong for UI, but limited to Chrome-based browsers without the Cloud tier. |

| Selenium | Free (open source) | Web UI, legacy browser support | Mature but 2× flakier than Playwright. Highest maintenance overhead. |

| Appium | Free (open source) | Mobile (iOS/Android) | Standard for mobile fintech. Requires device farm (BrowserStack $15–$100/month) |

| REST Assured / Postman | Free / $14–$149/month | API testing | Essential for payment API regression. |

| k6 | Free; Cloud from $49/month | Load testing | Best developer experience for payment load test scripting. |

While the automation framework itself carries a cost, you also need to take into account the engineering investment in setting up this automation.

For example, setting up a Playwright-based test automation framework for a payment-enabled fintech product costs $15K–$40K in engineering time (2–6 weeks of senior QA automation engineer).

This cost covers framework architecture, CI/CD integration, test data management, parallel execution configuration, and a first regression suite covering core payment and KYC flows.

A poorly architected automation suite increases your need for maintenance at the senior engineer level.

When tests fail intermittently or break on UI changes, junior QA engineers escalate to senior backend engineers, who end up spending time on test maintenance rather than feature development.

This maintenance concentration can cost $75K–$120K/year in senior developer time for a 10-engineer team.

Alternatively, investing $15K–$30K in a QA architect for the first 2–3 months of framework setup saves 30–50% on long-term maintenance by producing a correctly structured framework from the start.

Beyond the initial costs, we recommend that you budget 15–25% of initial test suite build costs for maintenance.

A $30K initial framework requires $4,500–$7,500/year in ongoing maintenance engineering.

The QA budget for a fintech product combines QA engineering labour, test tooling and infrastructure, and the six fintech-specific test category builds.

Here is what that looks like when you use LATAM nearshore rates for engineering labour:

| Cost component | Seed | Series A | Series B |

| QA engineering labour | 0.5 FTE: $1.5K–$3K/month | 1–2 FTE: $3K–$8K/month | 3–5 FTE: $8K–$20K/month |

| Automation framework + CI/CD | $10K–$20K one-time | $20K–$40K build + expansion | $40K–$80K build + scale |

| Payment idempotency test suite | $15K–$25K | $20K–$35K | $30K–$50K |

| Ledger reconciliation + load testing | $10K–$20K | $15K–$30K | $25K–$50K |

| KYC state machine test suite | $15K–$30K | $20K–$40K | $30K–$60K |

| Compliance traceability testing | $8K–$15K | $12K–$25K | $20K–$40K |

| Test tooling (BrowserStack, Postman, k6) | $200–$500/month | $500–$2K/month | $2K–$5K/month |

| Load test infrastructure | $500–$1K/month | $1K–$3K/month | $3K–$8K/month |

| QA as % of dev budget | 25–30% | 25–35% | 28–35% |

QA is expensive, but the fintech QA investment case is stronger than in most other industries. Production defect costs carry real financial consequences:

Everything we have mentioned requires QA engineers who understand fintech domain conventions, not just test framework operation.

A QA automation engineer who can write Playwright tests for a general web application cannot necessarily design an idempotency test suite for a payment retry scenario.

This means you will either need to put each candidate through an extensive fintech screening process or provide 4–8 weeks of fintech ramp-up time before they can contribute.

Here are the different roles that you will need to fill:

Most seed-stage fintechs that we have worked with have none of these profiles in-house and end up with massive testing debt that inevitably surfaces in the first production incident.

By the time they start hiring, the cost is already elevated, with timelines that do not allow for conventional hiring or ramp-up time.

Trio places pre-vetted QA engineers and software engineers who write compliance-aware tests from the start, preventing unnecessary tech debt, and dealing with it as quickly and efficiently when they are brought on to your teams.

Since our developers are pre-vetted, they simply need to be matched to you based on your requirements and can be placed in as little as 3-5 days.