Hire by Technology

SERVICES

Mexico sits at the top of most nearshore hiring shortlists for US companies, and for fintech engineering specifically, it offers a combination that no other LATAM market quite assembles in one place.

Mexico has over 560,000 software engineers, making it one of the largest developer pools in Latin America, with roughly 124,000 STEM graduates entering the market annually, while sharing a land border with the US and a time zone.

It also falls under the USMCA trade framework, which provides legal protections for intellectual property and cross-border data flows.

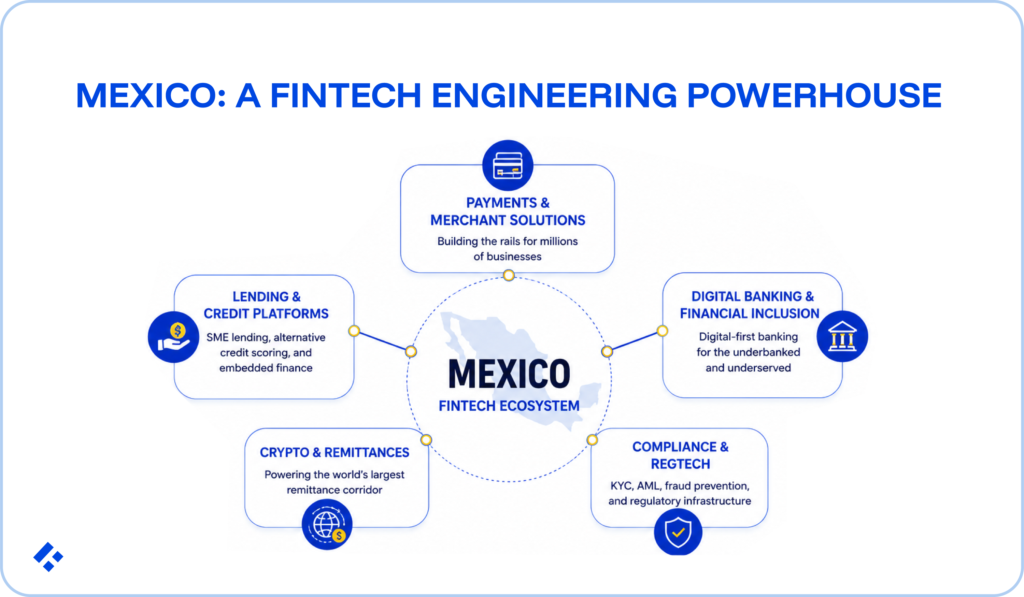

But it’s not just a great option for general software development outsourcing. The country has the second-largest fintech ecosystem (after Brazil), with hundreds of active fintechs operating under the Ley Fintech, Latin America's pioneering financial-technology regulation.

Many Mexican fintech engineers have built merchant payment systems (Clip), SME lending platforms (Konfío), crypto and remittance infrastructure on the world's largest remittance corridor (Bitso), and digital banking for a population that remains largely underbanked.

However, Mexican fintech developers are not the right choice for all companies. Making a hiring mistake could put you back months and lead to additional costs in terms of lost time and compliance backlash.

Let’s look at the skills Mexico's ecosystem produced, what they cost, how to hire them compliantly given Mexico's distinctive labour framework, and how to vet for fintech-specific competency.

At Trio, we pre-vet talent from Mexico for fintech production experience, so they can be placed in as little as 3-5 days.

Four things make Mexico distinctively strong for US fintech engineering hiring, and none of them applies quite the same way anywhere else in the region.

With 560,000+ software engineers and 124,000 new STEM graduates annually, Mexico generates a much larger absolute pool of engineering talent than any other country in Latin America.

Mexico also ranks #4 globally in Coursera's developer skills rankings and produces 49% of its first university degrees in STEM fields, well above the OECD average of 28%.

For fintech specifically, that scale matters a lot, since a larger general pool means a larger absolute number of engineers with potential fintech domain experience to draw from.

Mexico shares a border with the US, so if you need to get there to meet with developers in person, you can take advantage of the fact that a flight from many US cities runs two hours or under.

This occasional in-person collaboration can’t be matched by any other transatlantic or trans-Pacific engagement without real effort.

Central Time alignment also means Mexican engineers' working days overlap completely with US Central offices and substantially with East and West Coast teams, making meetings through video calls and synchronous communication through messaging convenient.

The USMCA framework provides legal protections for intellectual property and cross-border data flows, giving Mexico a structural advantage for any fintech concerned about where its IP and data reside.

Mexico pioneered fintech regulation in Latin America.

The Ley Fintech, which is the Law to Regulate Financial Technology Institutions, covers electronic payment fund institutions (digital wallets), crowdfunding platforms, and novel models through a regulatory sandbox.

It requires licensed entities to implement robust KYC, anti-money-laundering controls, and consumer protection measures.

This means that many Mexican fintech engineers have built under a mature, compliance-oriented regulatory regime longer than their peers in most of LATAM.

Mexico's fintech ecosystem now also includes hundreds of active fintechs with several unicorns like Bitso (crypto and remittances), Clip (merchant payments), Konfío (SME lending), Stori (digital banking), and Clara (B2B expense management), with Plata becoming the most recent addition to the unicorn cohort in early 2025.

Only about 49% of Mexicans over 15 hold a traditional bank account.

This gap created a specific engineering context where developers have experience building financial services for users without the documentation, credit history, or infrastructure that conventional banking assumes.

Many Mexican fintech engineers have built KYC onboarding flows for thin-file users, alternative credit scoring models, and mobile-first designs that work under limited connectivity.

This experience transfers directly to US fintechs targeting underserved populations or building for emerging markets.

Mexico's tech workforce is concentrated across several distinct hubs, each with a different character.

Mexico's fintech talent pool clusters around four profiles, each shaped by a specific part of the local ecosystem.

Engineers in each group tend to bring domain context alongside technical capability.

These are engineers from the Clip, Mercado Pago, Oxxo Pay, and Spin by OXXO ecosystems.

They have production experience in merchant payment acceptance, mobile point-of-sale, payment gateway integration, and Mexico's specific payment infrastructure, specifically SPEI (the interbank electronic transfer system) and CoDi (Banxico's QR-code-based instant payment system).

Clip, Mexico's first payment unicorn, anchors a deep merchant-payments engineering specialism.

In our experience, engineers from this ecosystem have built the full stack of payment acceptance, including terminal integration, payment link generation, reconciliation, settlement, and the acquiring-side systems that process millions of merchant transactions.

Lending is a notable Mexican strength, anchored by Konfío and Clara.

These engineers have usually built loan origination flows, AI-driven credit underwriting models, corporate card issuing systems, and the risk infrastructure B2B fintech products require.

What is often surprising for fintech firms here is the AI depth. 77% of Mexican fintechs report using AI, and the SME-lending ecosystem has developed particular expertise in machine-learning-driven credit scoring for thin-file business borrowers.

Remittances and crypto are a distinctively Mexican specialism with no close equivalent elsewhere in LATAM.

The US-Mexico remittance corridor handles more volume than any other remittance corridor in the world, receiving $64.7 billion in remittances in 2024, a new record.

Bitso, Mexico's first Bitcoin exchange and now a 9M+ user platform (as of December 2024), built crypto and stablecoin infrastructure specifically designed to serve this corridor, processing $12 billion in transactions in 2024 alone, a 90% year-over-year increase.

Engineers from this ecosystem have genuine production experience in crypto exchange systems, stablecoin integration, cross-border payment rails, and the compliance architecture that cross-border financial flows require.

This category includes engineers from Stori, Klar, Nu México (which surpassed 10 million total customers by early 2025 and leads Mexico's Sofipo savings category with 5.6 million savers), Hey Banco, and the broader neobanking ecosystem.

Their experience covers building digital banks and credit products for a largely underbanked population, including things like the KYC/digital-identity onboarding, alternative credit scoring, and mobile-first design that financial inclusion under the Ley Fintech requires.

The compliance context here tends to be strong, since Sofipo-regulated entities operate under CNBV oversight, which means engineers from this ecosystem have built under financial regulators, not just internal guidelines.

Mexican fintech developer rates run 30–60% below US domestic equivalents, with some variation by hub and seniority.

The average senior software developer in Mexico earns approximately $69,000/year, compared to roughly $122,000 for an equivalent US role.

The USMCA framework and relative peso stability make engagement costs more predictable than in markets with higher currency volatility, like Argentina.

Annual salary and hourly ranges for US-facing remote roles (2026):

| Seniority | Annual (USD) | Hourly equivalent |

| Junior (0–2 years) | $30,000–$45,000 | ~$25–$40/hr |

| Mid-level (2–5 years) | $48,000–$66,000 | ~$40–$58/hr |

| Senior (5+ years) | $66,000–$90,000 | ~$55–$80/hr |

| Lead / specialised fintech | $90,000–$120,000 | ~$80–$100/hr |

A few practical points worth noting:

Mexico's large, mature fintech ecosystem produces more fintech-experienced engineers than almost any market in the region, but ecosystem depth generates more qualified candidates, not guaranteed individual competency.

The five fintech competencies worth screening for are:

English proficiency across Mexico's major tech hubs has improved markedly, and most senior engineers working in US-facing roles communicate well.

However, proficiency still varies by individual and should be assessed during the process, particularly for roles involving client-facing work or complex architectural discussions.

When considering Mexico to outsource or augment your staff, there are a couple of practical considerations that will play a role in that decision.

Mexico aligns with US Central Time and overlaps strongly across all US time zones.

For US East Coast teams, the offset stays manageable, and for West Coast teams, the alignment is close to ideal.

We have also discussed physical proximity already. Thanks to the shared border, you have the opportunity for in-person collaboration at a frequency that's simply not practical with Eastern Europe or South Asia.

Mexico's 2021 labour reform prohibits the subcontracting of personnel.

Only "specialized services" that fall outside a company's core business activity may be outsourced, and providers must hold active registration with REPSE (the Registro de Prestadoras de Servicios Especializados u Obras Especializadas), Mexico's registry of authorized specialized service providers.

Non-compliance carries meaningful consequences, with major fines ranging from approximately $12,000 to $222,000+ USD under the Federal Labor Law, blocked tax deductibility, joint liability for the provider's employee obligations, and potential criminal exposure.

Enforcement tightened further in December 2025, when Mexico's STPS published a new inspection protocol specifically targeting irregular REPSE arrangements.

You need to make sure that you are choosing the right engagement structure for Mexico hiring functions as a genuine risk-management decision, not just an administrative convenience. A compliant managed staffing partner or Employer of Record handles this by design.

Four common structures for US companies hiring Mexican developers:

The USMCA framework provides explicit legal protections for intellectual property and cross-border data flows.

This data ownership, combined with the relative stability of the Mexican peso, makes Mexico a more predictable engagement environment than markets with higher political or monetary volatility.

Trio places pre-vetted Mexican fintech engineers with US and EU fintech companies, alongside engineers across LATAM.

We focus exclusively on fintech, which means the Mexican developers you hire through us arrive with domain context from the local ecosystem rather than needing weeks of orientation before contributing safely in a regulated environment.

Since they are already extensively vetted, they only need to be matched to you based on your specific requirements, so they can be placed in 3–5 days at $40–$80/hr ($7,000–$14,000/month).