Hire by Technology

SERVICES

The use of AI coding in enterprise SaaS has created a growing need for engineers embedded at the point of customer value. While products may work in staging, real production deployments often run into issues, and when you add the complexities of regulated financial environments, the chances of something going wrong only increase.

This is where forward deployed engineers (FDEs) come in.

A forward deployed engineer combines software engineering with consulting to embed directly within a financial client, whether a bank, hedge fund, or payment processor, and write production-grade code inside their environment.

They bridge the gap between a fintech product's core capabilities and a specific client's unique regulatory, security, and operational needs.

Let's look at exactly what a forward deployed engineer does in a fintech context. We'll go over the responsibilities, the skills required, the salary range, and the two distinct ways fintech companies tend to use the FDE model.

If you need expert FDE developers to ensure your integrations work effectively, or to ensure your customers can integrate your product successfully, you are in the right place.

Forward deployed engineers work embedded within a client organisation, writing production-grade code inside the client's environment to close the gap between a software product and the client's real-world operational needs.

Palantir originated the model in the early 2010s under the name "Delta." Since then, OpenAI, Anthropic, Ramp, Stripe, and a growing number of AI and enterprise software companies have built FDE functions of their own, and demand for the role has grown considerably.

If the role can be summarised in a single word, it would be "ships."

In practice, an FDE scopes the real problem with the customer, builds a working prototype, validates it against actual workflows, ships it to production, and owns what happens next. When something breaks in production, the FDE fixes it.

There are a few adjacent roles worth distinguishing it from:

The distinction that matters most: only the FDE writes code on the client's infrastructure.

Every FDE works inside a client's environment with the client's data and constraints, so their specific tasks always vary.

Fintech constraints, though, differ structurally from general enterprise software deployments in ways that carry real compliance and operational consequences.

Unlike consumer applications, a defect in a financial transaction system can mean significant financial losses, regulatory penalties, or audit failures. FDEs ensure deployments remain secure and compliant throughout, which shapes the work at every level.

There are four specific structural differences you need to understand before letting an FDE anywhere near your application.

A fintech FDE can't make architectural choices purely on technical merit.

Before writing the first line of integration code for a payment flow, for example, the FDE needs to determine PCI DSS scope and apply that information throughout.

That determination affects which systems come into scope, which access controls apply, and which security standards the code must satisfy. Adding something as simple as a logging statement requires checking whether it would capture card data.

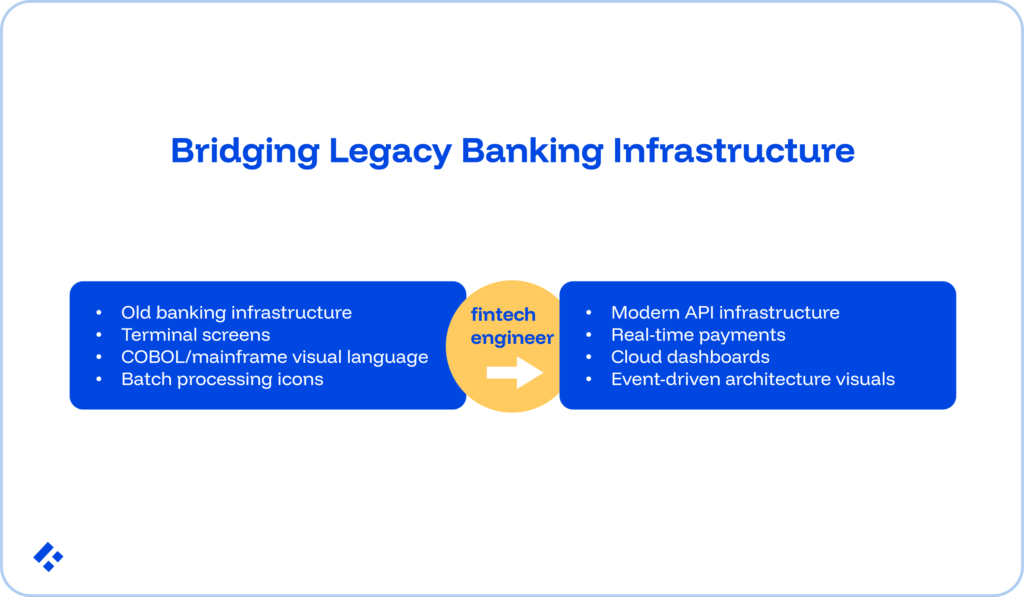

General enterprise SaaS FDE work typically involves connecting one modern product to another.

Fintech FDE work frequently involves connecting a modern product to a legacy core banking system running on a mainframe, a proprietary protocol, or a batch-processing architecture that predates REST APIs entirely.

In these cases, the FDE designs and builds the bridge.

This usually takes the form of normalisation layers that translate legacy data formats, adapter patterns that make legacy batch systems accessible to real-time API consumers, and event-driven connectors for systems that only support polling.

Many fintech FDE engagements start because of a specific, fixed deadline.

Recent examples include the Fedwire ISO 20022 migration, the SWIFT MX message format transition, DORA compliance requirements, and the Nacha 2026 account validation mandate.

These dates generally don't shift, so the FDE deploys to close the implementation gap before the deadline arrives, under a timeline the client's engineering team couldn't achieve alone.

In fintech, mistaking a product limitation for a client implementation gap, or the other way around, creates serious issues.

Building a workaround for what turns out to be a product limitation may become a compliance risk when the underlying product updates.

Likewise, escalating a client implementation gap as a product bug costs the vendor's engineering team time that should go toward the actual roadmap.

The following deliverables appear consistently across fintech FDE engagements, though the weight of each shifts depending on the client's situation.

All FDEs need strong software engineering fundamentals, at least one systems language (Python and TypeScript are most prevalent), SQL and data pipeline literacy, and working knowledge of cloud infrastructure across AWS, GCP, or Azure.

On top of that, they need the communication skills to function effectively in a stakeholder-heavy environment.

One thing worth noting: an analysis of over 1,000 FDE job postings found LLM experience listed in 31% of them and RAG architecture in 12%. The technical requirements for the role appear to have shifted meaningfully toward AI deployment skills over the last two to three years.

Fintech FDEs also need several domain-specific competencies that rarely appear in standard engineering roles:

The FDE function appears in fintech in two structurally different configurations. Knowing which one applies changes how you structure the engagement and what due diligence you need to do upfront.

Companies like Ramp and Stripe embed FDEs with their largest enterprise customers to accelerate implementation, close the gap between the product's general capabilities and a specific enterprise's infrastructure, and generate product feedback that shapes the roadmap.

In this model, the FDE works for the fintech vendor but operates inside the bank or enterprise client's environment. The benefits include lower implementation failure rates, faster time to first value, and product insights that internal teams can't replicate from behind a ticketing system.

Banks and large fintechs receive embedded FDE teams from their technology vendors, typically core banking system providers, fraud detection platform vendors, and payment orchestration companies.

In this configuration, the bank or fintech holds the client position. If you're in this position, you'll need to evaluate whether a vendor's FDE carries sufficient qualifications for a compliance-sensitive production environment.

This process requires the same due diligence as evaluating any external engineering resource with access to your infrastructure.

Fintech FDE talent remains scarce.

Finding engineers who combine production-grade technical ability, client-facing communication skills, and deep fintech domain knowledge proves genuinely difficult, and compensation reflects that scarcity.

Based on disclosed 2025 job postings, the median FDE total compensation across the broader market sits at approximately $174,000.

At OpenAI and Anthropic, mid-to-senior FDE packages have settled at $350,000 to $550,000, partly because client profiles at those companies require engineers who can fine-tune models and present findings to a Fortune 500 CTO in the same week.

Contract FDEs engaged for specific implementation projects typically bill $60 to $250 per hour, depending on region, seniority, and domain specialisation, with fintech specialists at the upper end of that range.

At Trio, those senior fintech specialists are sourced from LATAM, which brings costs to $40 to $90 per hour, depending on your specific needs.

Three engagement structures appear most often in fintech FDE deployments:

Finding the right people for this role remains genuinely difficult.

The FDE candidate pool in fintech typically draws from three backgrounds: senior fintech engineers who develop customer-facing skills over time, solutions engineers with enough coding depth to write production code, and generalist engineers who have worked at a fintech company and absorbed the domain conventions over time.

Realistically, traditional hiring timelines rarely align with implementation schedules or regulatory deadlines.

That leaves most organisations choosing between building FDE skills in a fintech specialist already on staff or developing fintech domain knowledge in an FDE generalist from outside the industry. Neither path moves quickly.

Alternatively, working with a specialist staffing partner who pre-vets for the specific combination of fintech domain knowledge and FDE delivery experience may reduce that timeline considerably. At Trio, we can place the right people in as little as three to five days.