Hire by Technology

SERVICES

Bitcoin and blockchain were once considered breakthrough tech. But nowadays, they are far from a niche new development. Even established financial institutions are now leveraging similar tools to enhance their cross-border payment infrastructure.

CBDC (Central Bank Digital Currency) technology, or a digital form of a country’s official currency, is one such example being used to promote economic stability and make real-time payments more feasible, especially cross-border payments.

However, with the increased use and development of these payment networks, companies in the fintech sector are experiencing a mixture of challenges and opportunities.

With countries piloting CBDCs and the ongoing demand for faster, cheaper international payments, you need to understand how to adapt your infrastructure to these new systems so that you can not only deal with cross-border transactions effectively but also potentially find opportunities to create solutions for existing financial systems.

Our developers here at Trio specialise in fintech, giving them an extensive understanding of everything involved in the technical and regulatory side of cross-border payments and CBDCs.

If you need development assistance, view our capabilities.

The best place to start is with what cross-border payments are and how they currently work, especially in the context of emerging forms of money.

Cross-border payments refer to transactions in which the payer and payee are located in different countries.

Usually, they involve different forms of money or different currencies, which can create frictions in the process.

The payment, if made in cash, would have to literally cross borders.

This is rarely the case today, though. Instead, the process occurs through electronic payment methods like B2B transfers, card payments, e-commerce settlements, interbank settlements, and many others.

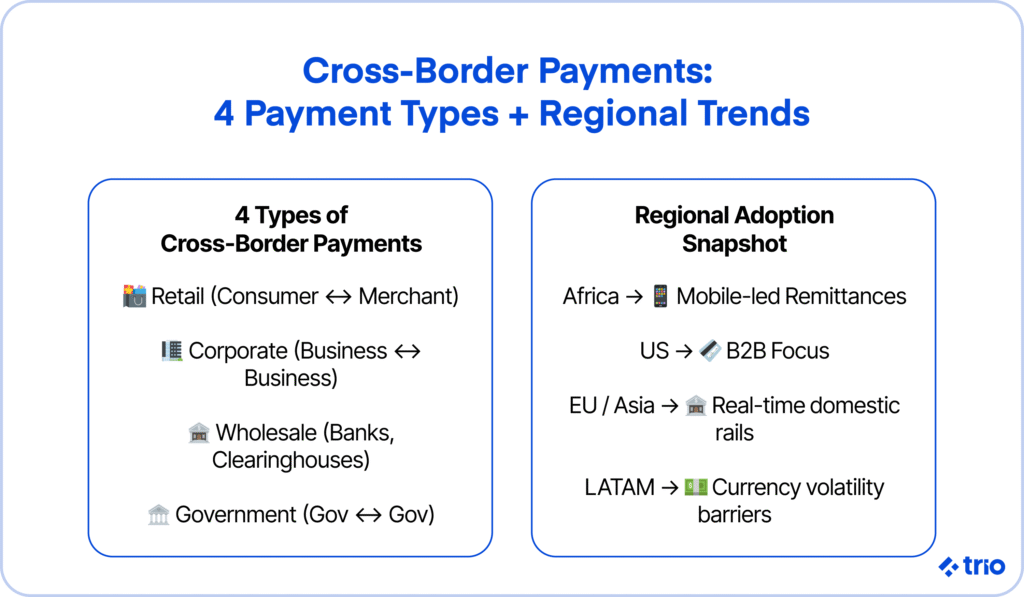

These payments can also span a wide range of use cases, from consumer to corporate, and even include financial institutions.

A lot of people like to split the types of cross-border payment systems into four different categories:

Essentially, every country in the world is interested in making instant payments across borders. However, we have noticed that their motivations for doing so, as well as the payment service providers they utilize, can differ vastly.

In Africa, mobile-led remittances are gaining significant popularity. Sub-Saharan Africa accounted for a large proportion of total growth in mobile money accounts in recent years.

In more developed economies like the United States, B2B payments are the focus, and many companies are focused on getting speed up and cost down.

Outside of consumer demand, we are also seeing factors like region-specific regulations, currency volatility, and banking infrastructure play a role in the frequency and efficiency of these payments.

Now that you have an idea of what cross-border payments are, let’s examine the infrastructure required to support them, along with the changes that may be necessary when working with legacy architecture.

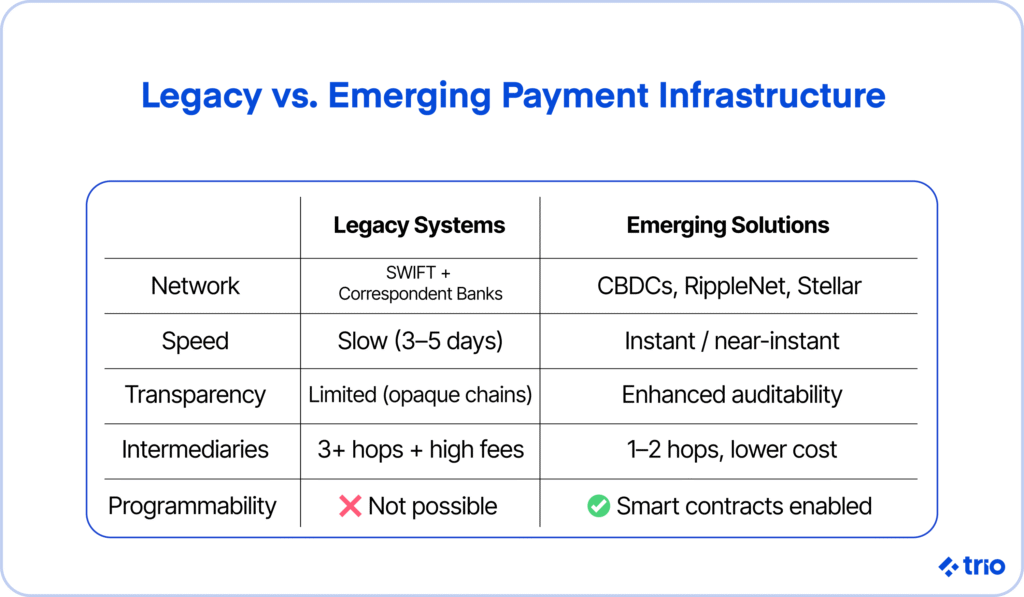

Everything, from international to regional payments, still relies heavily on correspondent banking relationships and centralized messaging systems. However, working with these systems can be expensive, so knowing what you are up for ahead of time is a non-negotiable.

The Society for Worldwide Interbank Financial Telecommunication (SWIFT) is the primary messaging network banks currently use.

Many people who are unfamiliar with the fintech industry believe that it moves the money, but this is not true. Instead, it sends payment instructions between banks using a standardized format.

So, how are funds settled then?

In short, SWIFT messages only work if they are paired with correspondent banking, which involves one bank holding accounts with another. This account is used to fulfill any monetary obligations.

This process can get complicated.

You inevitably end up working with long chains, especially if you are dealing with minimally used currencies, like the kind that you might encounter in less developed markets.

Settlements are also incredibly slow, with high intermediary fees and exchange markups.

And, to make matters even worse, there is very little that end users and compliance teams can see, making KYC processes difficult to implement and enforce.

As you can imagine, SWIFT is a nightmare for fintech platforms trying to enhance cross-border payment services. It acts as a massive infrastructure bottleneck.

The result has been that many different regions are investing in faster technology, such as the EU’s TARGET Instant Payment Settlement (TIPS), India’s UPI, and the UK’s Faster Payments.

These are probably some of the best examples of domestic payment systems. The issue is that they still do not improve global networks.

SWIFT gpi and Visa B2B Connect are some ways in which people are trying to make cross-border payments. However, even though they offer some improvements in terms of speed and transparency, they are still based on legacy technology.

The only real solution that has emerged in recent years has been blockchain-based networks and CBDCs.

RippleNet and Stellar are providing crypto-native infrastructure, while companies like JP Morgan and Visa are turning to hybrid models and stablecoin experiments to advance their capabilities in international trade.

Fintech companies are capitalizing on the shift in industry standards to develop products that leverage alternative cross-border payment methods and address the issues associated with previous systems.

These smaller companies are transforming the payments landscape by reducing intermediaries (or “hops”) and enhancing both transparency and auditability, thus addressing frictions in cross-border payments. A lot of them are also focused on near-instant currency conversion.

These smaller companies are also able to use things like programmable logic, which would have been impossible in many legacy systems, allowing them to leverage smart contracts and similar blockchain-based technologies to ensure security and prevent fraud.

However, if you are interested in getting involved, you need to be incredibly careful. Making mistakes in the fintech sector is not an option. You are handling people’s money and their sensitive personal information.

You need to ensure that you have expertise on your team.

Related Reading: Intelligent Payment Routing

If you decide to build anything related to cross-border payments, you should be aware of the challenges you will encounter.

Knowing the pain points ahead of time allows you to plan for them and address them in the most cost-effective way possible.

Cross-border payments can get very expensive. While it varies from region to region, usually it is a percentage of the amount being sent.

These costs generally include the SWIFT fees, intermediary bank charges, foreign exchange markups, and additional overhead related to security and compliance.

There is a notable lack of price transparency for people trying to use traditional services.

You may have to be prepared to deal with very slim margins and focus on transparency to stay competitive.

Developers who understand the U.S. regulatory landscape but operate out of lower-cost markets give you a meaningful edge here, since they can help you build compliance-aware systems without the overhead of onshore hiring.

Compliance can be intense, especially when considering the numerous differences across the global financial system. Regulations don’t just differ from country to country, but sometimes even differ in different parts of the same country.

Typically, these regulations encompass all aspects related to anti-money laundering (AML), know-your-customer (KYC) requirements, foreign exchange controls, and capital flow restrictions.

The fragmented nature of these regulations results in differences in services depending on the user’s location, which drastically increases development and operational costs while complicating client onboarding and transactions.

CBDCs offer a way to mitigate some of these differences, as they are governed globally. That said, the rapid acceleration of stablecoin adoption adds a layer of complexity here that wasn't present a few years ago.

Private stablecoin issuers operate outside the same governance frameworks, and the regulatory response to that gap varies significantly by jurisdiction, so the picture may look quite different depending on where your users are based.

We have already mentioned the long chain of intermediaries that money traditionally goes through. If you are working with older institutions, you need to be prepared to work with these chains.

They often cause delays, data truncation risks, and make tracking and reconciliation incredibly difficult, contributing to frictions in cross-border payments.

With so many go-betweens, it’s also far more likely that something will go wrong, and you won’t be able to identify where the issue occurred.

Additionally, you need to deal with the fact that traditional banks often still batch their transactions, rendering real-time payments impossible, even if other parties in the transaction chain can ensure instant settlement on their end.

Since many parts of the world are still working with traditional banks, you will need to have funded accounts with those banks.

This can get very expensive.

While the money can technically be returned, having all of your capital tied up can hinder your growth in other areas.

Banks also have limited operating hours, to which those accounts will be subject.

CBDCs can be an incredible solution here, as they enable you to implement an always-on infrastructure and integrate liquidity mechanisms into your product.

We have already mentioned that SWIFT is still considered the industry standard. Which means you may encounter it in your workflows, leaving you subject to its limited field capacity.

You may be forced to reduce transparency, or you may notice your AML efforts are not practical.

ISO 20022 was designed to address these issues.

But you’ll still need to deal with legacy systems that lack the necessary support for automated compliance processes.

One issue that we have noticed our clients are rarely even aware of is sanctions filtering and fraud detection. You may need to integrate these capabilities into your products manually, which can make your tech stack more complicated.

CBDCs, as we have already mentioned, are digital currencies. Think of bitcoin, but more formal, issued by central banks, and designed to be legal tender.

A lot of people confuse them with stablecoins. But it’s important to note that stablecoins are privately issued, while CBDCs often refer to digital legal tender, created by governments.

Since they are formally issued, they are also centrally governed, and banks generally aim to have them reflect the value of an existing currency. For example, the digital yuan (e-CNY) is tied directly to the Chinese Yuan.

In theory, it’s just a digital version.

The U.S. doesn't currently have a retail CBDC. In early 2025, President Trump signed an executive order halting all domestic retail CBDC development, making the U.S. the only major economy to formally step back from that path.

However, since the U.S. continues to participate in wholesale cross-border payment research through Project Agorá, a collaborative initiative with six other major central banks, a total disengagement from CBDC development seems unlikely.

Retail CBDCs are typically intended for general use by everyone. It’s a digital form of cash that can be stored in a digital wallet and spent as you’d like, typically through peer-to-peer (P2P), consumer, or merchant payments.

Wholesale CBDCs are only for financial institutions and represent a new form of money in the evolving financial ecosystem. They are used to try to modernize transactions between banks.

Between the two, wholesale CBDCs are likely to have the most significant impact on global cross-border payments at present.

Since banks and similar institutions primarily use them, they are easier to govern; however, they still enable increased payment speed for the average consumer, thanks to reduced transaction chain delays.

We are very excited about the development of multi-CBDC arrangements (mCBDCs).

Project mBridge, which connects central banks in China, Thailand, the UAE, Hong Kong, and Saudi Arabia, aims to advance international trade through innovative forms of money.

Project Dunbar aims to address the frictions in cross-border payments through innovative CBDC solutions., led by the BIS Innovations Hub, is testing how cross-border payments can be made across multiple CBDCs.

Currently, these systems employ a shared ledger model, where each bank maintains its own CBDC, but inter-bank transactions take place on a common platform.

So far, it seems promising. Some benefits include everything you would associate with a decrease in intermediaries.

But there are still a lot of technical and regulatory challenges that need to be addressed, particularly regarding identity management and what happens in the event of a dispute.

Preparing for a future that might include CBCD integration is critical.

To make sure you are ready, you will need to audit your fintech stack to ensure you are ready to utilize the technology to facilitate instant cross-border payments.

For each component, consider agility, interoperability, and long-term resilience.

Related Reading: Payment Facilitation Explained

If you are working with a legacy system of any kind, identify issues that will affect transaction speed and auditability. Since these are so critical in interlinking fast payment systems, a comprehensive overhaul may be necessary.

If you’re not sure where to start on this, we’d recommend taking a look at your general ledger, treasury management systems (which must be auditable in real-time), and any payment gateways you may be using.

An API lets you interact securely with other systems.

Most central banks are probably going to publish public or restricted-access APIs for their CBDCs. These APIs will facilitate issuance, redemption, transaction validation, and even wallet services.

There may be an opportunity for you to gain a foothold in the industry by creating secure APIs in collaboration with these institutions, provided you can assemble the right team.

To do this, you’ll need developers who understand both financial compliance requirements and API security at a level most generalist engineers simply don't have.

The key is going to be standardizing your API architecture around protocols like REST, and either gRPC or GraphQL support. Ensure that you also consider global regulations, particularly as they evolve.

Any systems you create will need to have low latency and high availability.

Security, compliance, and long-term reliability are all things we have mentioned before. But what does this mean in practice?

You need to ensure that unauthorized individuals cannot access your infrastructure. Similarly, no one should be able to tamper with it.

Consider what would happen if sudden influxes of traffic were to occur. Would the system fail?

Our developers can help you implement fine-grained permissioning, ramper-evident logging, and automated transaction monitoring or fraud detection. They can also make sure that you are up-to-date with the latest regulations.

One area that many of our clients often overlook is their disaster recovery plan. What happens if there is a domestic or international failure? Do you have alternative providers or systems you can switch to, so that you can minimize potential downtime?

Related Reading: Scalable Payment Systems

Pilot programs and regulatory sandboxes are sometimes launched by central banks or initiatives that are affiliated with these experiments.

If you can, try to utilize the provided tools and familiarize your developers with any available information.

These will provide your team with knowledge about potential technical constraints you need to address, API structures you will need to implement, and compliance requirements.

It’s also a good idea to start establishing a partnership with your relevant central bank or the intermediaries that will provide you with access to the APIs you need in the future.

While there’s no way to say anything with certainty yet, past trends indicate that these CBDC APIs will probably be gated in some way.

MAS (Singapore), the Riksbank (Sweden), and the Bank of England are all publishing resources.

The contents of these differ, but some include SDKs, interface definitions, and references to assist with tasks such as wallet integration or KYC verification.

While it is best to focus on region-specific documents, when it comes to global payment systems, it is probably safe to assume that there will be a fair amount of overlap.

International standards will be key if the global CBDC landscape is to be effective.

The G20 has been coordinated by the Financial Stability Board (FSB) and the BIS. The hope is that international payment options will be faster, more accessible, and more transparent in measurable ways.

The initial G20 cross-border payment targets have a deadline of 2027. CBDCs could play a significant role in helping countries reach these goals and increasing global financial inclusion.

ISO 20022 is quickly becoming a standard alternative to SWIFT.

It enables richer data sharing and greater transparency, making it the most likely option for CBDC systems to adopt.

Another global initiative to consider is the work of CPMI (Committee on Payments and Market Infrastructures) on standardizing APIs and digital identity frameworks.

These standards all aim to support overall stability and economic growth.

Interoperability is crucial at a policy level, but it’s also important to consider the efforts of leading fintechs, banks, and infrastructure providers who are forming consortia to create shared rails and interoperability layers.

We have been closely monitoring efforts such as the Universal Digital Payments Network (UDPN) and BIS’s Project Nexus, along with a few others, to ensure we have a clear understanding of the private sector’s plans to improve regional payment systems and, eventually, cross-border payments.

We would be remiss if we did not examine the risks that CBDCs pose. These risks span operational, technical, and regulatory fields.

If you think you will need to design or evolve your architecture to utilize CMDCs for instant payments, then weighing the numerous risks against the potential benefits is one of the first steps to ensuring your company’s continued success.

Adding CBDC infrastructure into your fintech products will mean that you have more code to write and a more complex tech stack to maintain. This means you’ll need to think about additional costs, both in initial development and long-term maintenance.

The added code and tools also mean that there are more opportunities for things to go wrong, whether that is due to an increased reliance on vendors or new hiring needs that you may fill incorrectly. The latter is easily addressed when you go through a company like Trio.

New APIs with different identity standards increase your potential attack surface, too.

You will need to focus on an extensive DevSecOps strategy, ensuring that you have all the necessary tools ready. This will enable you to identify issues as early as possible, pinpoint their origin, and develop comprehensive contingency plans as part of effective risk management.

None of this is free, and it can make it a lot more challenging to enter the field when CBDCs become more commonplace, and users expect access as a bare minimum.

Related Reading: Instant Cross-Border Payment Trends

If CBDCs are appropriately integrated, we could be looking at some new targets for cross-border payments. Instant settlements will be the norm, and you will need to adjust to the shifting metrics to stay competitive.

However, the reduced FX exposure and real-time reconciliation that are made possible will decrease the cost of these transactions, potentially allowing you to compete with established institutions by offering lower rates or achieving better margins.

Either way, if you rely on liquidity, speed, and trust, this potentially gives you an edge, provided you can capitalize on these technologies before most of your competitors.

One of the best ways to ensure you are ready is to have an industry expert on your team. We can help with that by providing solutions to reduce frictions in cross-border payments.

Ready to get started, or need more information? Request a consult.

Cross-border payment infrastructure covers the systems, networks, and agreements that allow money to move between countries. In practice, an international payment typically passes through multiple intermediary banks before settling.

CBDCs improve cross-border payments by enabling central banks to settle transactions directly on shared digital ledgers, cutting out the intermediary chains that slow down and inflate the cost of traditional transfers.

Multi-CBDC arrangements let central banks from different countries settle transactions across a shared platform while each maintains its own digital currency. They matter for fintechs because they could eventually replace the correspondent banking layer that most international payment products depend on.

The U.S. doesn't currently have a retail CBDC, and domestic retail CBDC development has been halted by executive order.

Preparing for CBDC integration means auditing your core ledger, treasury systems, and API architecture for compatibility now, and engaging with available sandboxes so your team understands real technical constraints before the rails go live, and building relationships with banks that will likely be involved in CBDC development in the future.