Hire by Technology

SERVICES

Payment systems are supposed to quietly work in the background, but without the right preparation, they rarely work as they should.

A single routing misstep or poorly timed retry can mean lost revenue, extra support load, and frustrated customers who never come back. Approval rates that look acceptable in aggregate often hide significant regional variation, and that variation usually points directly to routing logic that hasn't been revisited since the initial setup.

In practice, improving your approval rate and reducing processing costs only happens when your routing logic is able to adjust in real-time or by implementing techniques like smart retries.

Let’s take a deeper look at how intelligent payment routing and smart retries work in real environments, including how payment routing strategies evolve as your business grows, why dynamic routing often outperforms static routing, and how you can implement these techniques.

At Trio, we provide senior fintech experts who help companies implement the latest best practices for payment routing to ensure your success.

Payment routing is the automated process of directing transaction data through the most efficient, secure, and cost-effective payment processor or gateway, ensuring high success rates.

Essentially, your routing system looks at each transaction, evaluates the available options, and tries to route payments through the path most likely to succeed at the lowest processing cost.

A simple payment stack probably just uses a single provider. That works for very small companies, but is not the ideal path forward if you need to scale or improve the success rate across regions.

Once you support multiple payment processors or operate globally, routing becomes a performance lever rather than a configuration setting.

At that point, you are balancing approval likelihood, latency, uptime, regulatory constraints, fraud posture, tokenization status, and the cost of a successful transaction alongside simply choosing a payment gateway.

The right choice depends on a bunch of different factors like the issuer, BIN range, card brand, geography, payment method, authentication state, and even the time of day.

A transaction on a Visa debit card issued in Mexico has different routing needs than a Mastercard credit card issued in Germany, and treating them differently based on those requirements can increase the chances of success.

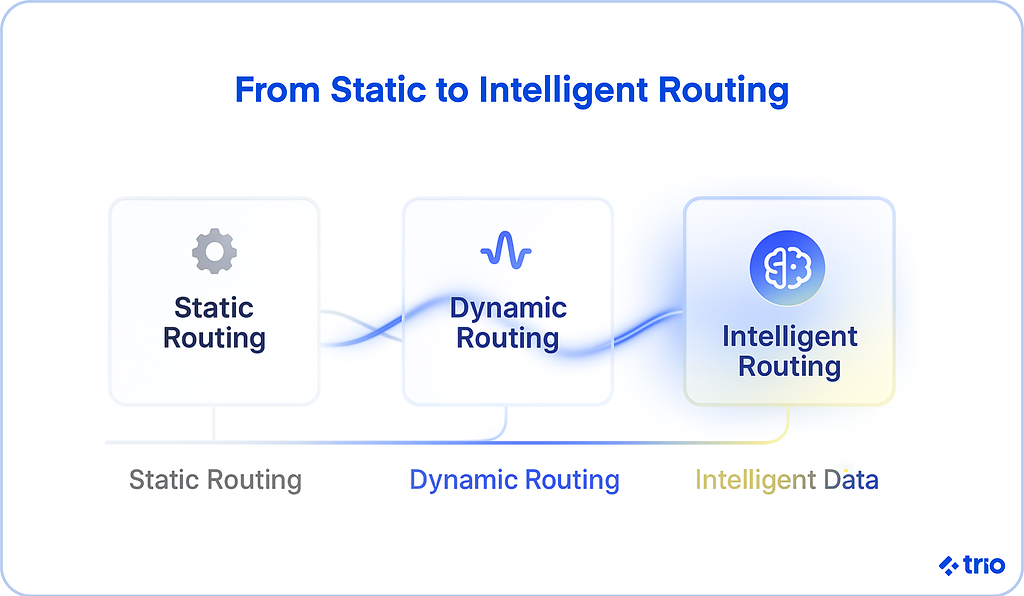

Many companies start with static routing rules. "Send everything to Stripe." "All EU cards go to Processor A."

The problem we often see these companies run into is that issuer behavior fluctuates, network performance varies, and certain card types tend to perform better with different payment service providers.

Dynamic routing reacts instead of assuming. It checks live performance indicators, evaluates factors like card type and geography, and adjusts routing decisions to achieve the higher approval rates we mentioned above.

Static routing also creates a single point of failure.

If your sole processor experiences elevated decline rates or a brief technical outage, every transaction in that window takes the hit. Dynamic routing helps you avoid being affected.

Related Reading: AI for Payment Modernization

Treating payments as a real-time system and adjusting is often referred to as intelligent routing, although we have also seen this called smart payment routing.

Here, your routing logic learns patterns. It predicts which route will perform best for a specific card issuer or region.

Certain BIN ranges authorize more reliably with a local acquirer, or that retrying a Visa card on a specific processor first thing Monday morning converts at a meaningfully higher rate than Friday evening, etc.

How is this different from the dynamic payment routing we already discussed? In short, dynamic routing reacts to real-time conditions. Intelligent routing adds a predictive layer based on historical payment data.

To get the best results, you really need to blend both.

Smart routing systems combine:

They also factor in dynamic acquirer logic, which involves routing each transaction to the acquirer most likely to have a strong connection to that specific issuing bank.

Over time, intelligent routing optimizes payment experiences by increasing the likelihood of successful authorization. You also decrease overall processing costs since you don’t waste your money on failed transactions.

Global merchants often see a 2 to 4 percentage point lift in approval rate after adopting intelligent payment routing. While this seems like a very small number, it can be an incredible amount at large transaction volumes.

Local acquisition usually drives the largest share of that improvement.

Local acquirers present transactions domestically. It’s pretty well known by this point that issuers favor this approach.

Routing European cards to a European acquirer rather than sending them across borders often reduces payment failures noticeably, particularly if you are working in markets where cross-border processing carries implicit risk flags.

Network tokenization also plays a role, particularly if you are working with stored-card business models, since issuers recognize tokens more reliably over time and extend more trust to recurring authorization requests on a known token than on a raw PAN.

The important thing that you need to keep in mind is that you cannot always optimize for approval and for cost at the same time.

Sophisticated routing strategies can help you separate these two objectives, optimizing for approval rate during peak checkout windows and weighting cost more heavily during periods where failure recovery matters less.

Regional variation adds further complexity.

US debit routing sits under Durbin Amendment requirements that give merchants the right to route debit transactions over at least two unaffiliated networks, creating a direct optimization opportunity based on per-network approval rates.

PSD2 requirements in Europe affect authentication flows and, in turn, routing decisions for transactions that trigger strong customer authentication.

Our fintech payment specialists are familiar with all of these regulations, and many more, having actively worked in the industry for some time and dealt with these first-hand before.

Even with well-tuned routing logic, you can never guarantee that there will be no failures at all.

Smart retries give you a second chance to recover that revenue without irritating issuers or degrading the customer experience.

Basic retry logic usually works like this: payment fails, try again.

That handles temporary network blips, but in other scenarios, it can actually make things much worse.

Card networks track retry behavior, and issuers may treat repeated identical submissions as suspicious activity. If there is a borderline transaction, a basic retry might just be a thing to push it over the edge.

Smart retries, as the name suggests, are able to consider why the payment failed, when to retry, and which route to use next.

A decline due to insufficient funds may warrant a delayed retry timed to a likely payroll date rather than an immediate second attempt. A technical decline may suggest shifting to a secondary acquirer right away.

Smart retries also take issuer-specific patterns into account here since some issuers apply aggressive risk holds late in the month and others show elevated decline rates on weekends.

Here is a framework for structuring smart retry logic based on decline category:

| Decline category | Typical signals | Next action | Timing guidance |

| Temporary technical | Timeouts, unavailable, unclear errors | Fail over to a healthy acquirer on the first retry; stop if the issue persists | Immediate or within seconds |

| Insufficient funds | Code 51, NSF wording | Retry on the same or alternate route; notify customers of subscriptions | 6 to 24 hours, then 2 to 3 days, aligned to local pay cycles |

| Do not honor/suspected risk | Codes like 05, 65 | Consider adding 3DS or additional authentication signals, then switch acquirer if history supports it | 30 to 120 minutes after adding authentication |

| Hard stop | Lost, stolen, expired, or invalid PAN | Do not retry; request updated credentials or an alternate payment method | No further attempts |

As routing logic grows, payment orchestration is essential to facilitate scaling.

Rather than managing routing decisions across individual gateway integrations, a payment orchestration platform centralizes routing rules, retry workflows, analytics, and monitoring in one place.

When a single hub coordinates everything, it gives you the ability to test new routing rules safely, add a payment method without rebuilding the integration layer, and see exactly how transactions behave across processors in one view.

You can either consider building a custom routing engine in-house, which gives you maximum control over routing logic and payment stack architecture.

A lot of the companies that we work with need this control, but underestimate the maintenance cost, since each connected processor requires ongoing API version management, and the operational surface area grows with each new provider added.

For fintech teams where payment routing sits at the absolute core of the product's competitive differentiation, the custom path may justify that overhead.

But, in our experience, for almost everyone else, configuring routing rules on top of an orchestration platform tends to recover engineering time that compounds into faster product velocity elsewhere.

ProcessOut, Spreedly, and Primer are some of the most well-established options.

Related Reading: Payment Facilitation Explained: What is PayFac

To figure out if your system is running well, you need to track decline patterns, success rate segmented by region and BIN range, latency across processors, and cost per successful transaction.

It can be tempting to look at aggregate approval rates across all transactions rather than segmenting by card type and geography, but these can look stable while a specific market or card scheme quietly degrades.

Smart teams make incremental routing improvements and run controlled experiments rather than rewriting the entire routing setup at once.

Modern payment routing sets up a payment flow that scales with your business, adapts when markets shift, and protects customer trust.

Smart payment routing and smart retries provide that control, especially when combined with a thoughtful payment orchestration layer.

A mature routing system is a lot easier to manage when the engineers working on it already understand how payment stacks behave in production rather than learning the domain from scratch.

If you want help building intelligent payment routing, implementing smart retries, or designing a modern payment orchestration layer, Trio can connect you with engineers who have done this before.

Intelligent payment routing selects the best payment path for each transaction based on card type, issuer behavior, and real-time acquirer performance. It improves authorization rates and reduces processing costs by adapting based on predictions made from historical data.

Smart routing improves payment approval rates by directing each transaction to the processor or acquirer most likely to authorize it based on live performance data and historical patterns.

Static routing follows fixed rules set at configuration time. Dynamic payment routing adjusts routing decisions in real time based on processor performance, card type, geography, and other live signals, which tends to produce higher authorization rates.

Smart retries classify failed transactions by decline code to determine whether recovery makes sense, when to retry, and which processor to use next. They recover revenue from soft declines without triggering issuer risk flags, the way undifferentiated retry attempts tend to do.

Dynamic acquirer logic routes each transaction to the acquiring bank or processor with the strongest historical relationship to that specific issuing bank, rather than sending everything through one fixed acquirer. It addresses the reality that authorization likelihood often depends on the acquirer-to-issuer connection rather than anything about the transaction itself.

Payment orchestration platforms help with intelligent routing by centralizing routing rules, retry logic, multi-processor connectivity, and payment analytics, which makes intelligent routing significantly easier to configure and maintain.

Improving your payment routing setup usually starts with segmenting your authorization rate data by geography, card scheme, and BIN range to identify where declines concentrate. From there, testing routing changes that direct underperforming transaction types to alternative processors tends to produce the clearest gains.