Hire by Technology

SERVICES

In July 2025, the UK's Financial Conduct Authority fined Monzo £21 million for failures in AML controls. As the bank underwent exponential growth, its financial crime controls failed to keep pace. Monzo had accounts opened with implausible addresses. Their ongoing transaction monitoring had gaps. High-risk customers weren't subject to enhanced due diligence proportional to their risk profile.

If you have a neobank of your own, failure to prepare the architecture for scaling early on can put you at risk of similar regulatory pushback and even direct losses to your clients.

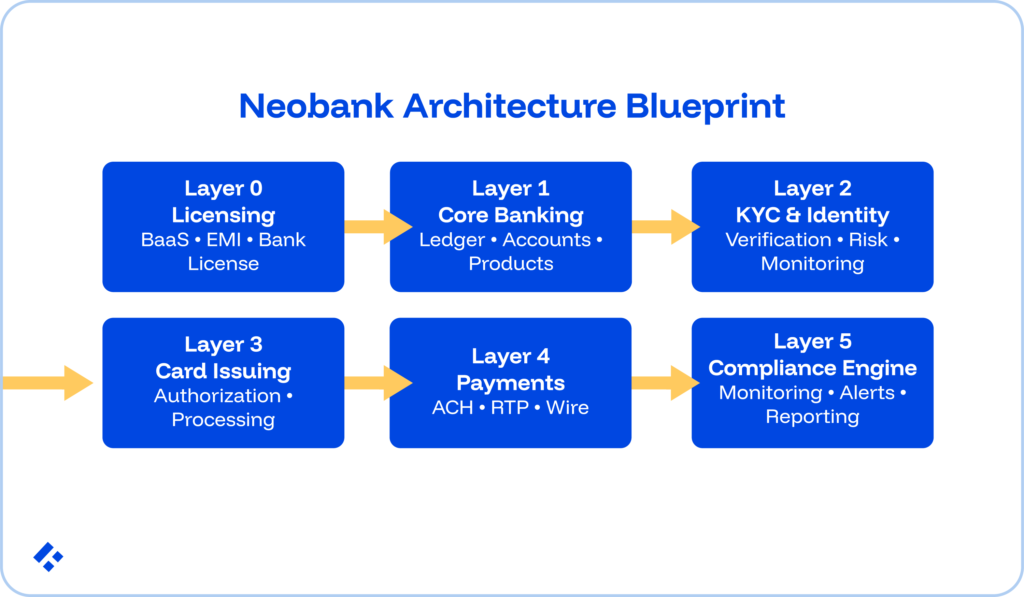

A neobank's architecture is made up of several layers, including the licensing model that determines what you build versus operate through a sponsor bank or BaaS provider, the core banking system (ledger, accounts, products), the KYC and identity pipeline, card issuing infrastructure, payment rails orchestration, and compliance as embedded engineering infrastructure. Each layer has a build-versus-integrate decision that changes as the neobank scales.

Let’s look at what each layer contains, the build-versus-integrate decision at each stage, and what specifically breaks when the decision gets made incorrectly.

Our specialist neobank developers, with proven experience helping financial institutions scale successfully in similar projects, can provide valuable insight and practical development.

Before writing a line of neobank code, the licensing model needs to be decided. This will determine which parts of the architecture you own, which you operate through a third party, and what regulatory obligations attach to every subsequent engineering decision.

Major fintech firms use this model, allowing their neobank to operate under the license and FDIC or DGS insurance of a partner bank.

The bank holds deposits, provides access to payment rails, and maintains the core regulatory compliance framework. This means the neobank just builds the product layer, which is composed of things like the mobile app, the UX, the product features, and the brand.

Chime is one of the better-known examples of this and uses The Bancorp Bank and Stride Bank. Most US neobank startups launch under this model.

Using BaaS licensing means your engineering team can stay smaller, with the tradeoff being that your vendor dependency risk runs higher.

The EMI holds an e-money license from a national regulator like the FCA, BaFin, and the Central Bank of Ireland.

With this licence, it can issue electronic money, provide payment services, and maintain payment accounts, but cannot take deposits that count toward capital requirements or make loans from its own balance sheet.

This is a good starting point, especially if you are validating your concept before moving to a full banking license.

If a neobank holds a full banking license, it basically means that it can operate as a bank without any external assistance.

You can hold deposits, make loans, and directly participate in payment systems.

Architecturally, this does mean that you need to operate your own core banking system.

You also own the full regulatory stack, which means you need an AML compliance program and have to maintain capital requirements.

The engineering scope expands significantly, but so does your product capability.

Related Reading: Beyond DevOps in Fintech: Engineering Culture and Agility

The core banking system manages the accounting and product logic of the neobank:

There are three different approaches that exist.

Cloud-native core banking systems provide a pre-built ledger, product configuration engine, and API surface.

In this case, your product rules get configured rather than coded.

Speed is the biggest benefit, as time to market runs 3 to 6 months versus 12 to 24 months for a custom build.

Be prepared for the fact that your product differentiation will be bound by what the platform's configuration model supports, though.

Here, the neobank builds its own double-entry ledger while using BaaS provider APIs for regulated banking services, like deposit-holding and payment network access.

You get maximum control over the accounting layer and product logic, while everything related to regulation runs through the partner bank.

There is definitely a higher engineering investment here, but you get a lower long-term vendor dependency.

For a full custom build, you will need to create in-house ledgers, accounts, product engines, and payment processing.

This option only works if you have full banking licenses that must operate their own core by regulatory necessity.

We don’t recommend this option for MVPs due to the excessive overhead it creates. Instead, we recommend that you start with one of the above options and gradually move over as the need arises.

KYC is one of the most compliance-critical layers of a neobank and the one that most commonly sees being under-engineered.

The Monzo fine traces directly to KYC implementation failures.

A customer's identity verification status isn't binary (verified/not verified). It moves through states with defined transitions and regulatory requirements at each step:

INITIATED → DOCUMENT_SUBMITTED → DOCUMENT_VERIFIED → LIVENESS_CHECK

→ SANCTIONS_SCREENING → RISK_SCORING

→ APPROVED / REJECTED / PENDING_EDD / SUSPENDED

Each state has specific entry conditions, permitted exits, and regulatory requirements at the transition.

A customer whose document verification passes basic checks but whose sanctions screening returns a potential match must not proceed to APPROVED, but instead to PENDING_EDD (Enhanced Due Diligence review).

A customer applying with an implausible address should fail document verification entirely.

If the KYC state machine permits that transition without validating address plausibility, the failure is architectural.

The FCA's criticism of Monzo wasn't only about initial onboarding, but also about monitoring.

Things like large, unusual deposits, changes in transaction patterns, or connections to high-risk jurisdictions should trigger re-verification or EDD.

This requires an ongoing KYC event stream where every significant transaction event evaluates against the customer's risk profile.

Changes in risk level need to trigger state transitions. For example, they might move from APPROVED_STANDARD to APPROVED_EDD_REQUIRED to SUSPENDED_PENDING_REVIEW.

Most neobanks integrate with specialist identity verification providers like Jumio, Onfido, Veriff, or Sumsub. These assist with document capture, liveness detection, and database screening.

That leaves you to own the state machine that interprets the provider's result and determines the next state. The provider's output is an input to the KYC state machine.

Card issuing seems simple, but beneath the surface, it requires a card processor, a BIN sponsor, the payment network, and the neobank's authorization and dispute management systems.

A neobank's payment capability runs across several rails. Each of these rails will be accessed differently depending on previous decisions like the licensing model and stage of the neobank's development.

The payment orchestration layer receives payment instructions from users, determines the appropriate rail based on amount, speed requirement, and recipient, submits to the rail through the sponsor bank or direct connection, and tracks payment state through to settlement.

Your payment state, which is usually something like initiated, submitted to rail, pending settlement, or settled, needs to be modeled explicitly.

A direct deposit that arrives at the ACH network doesn't appear in the user's available balance until the sponsor bank confirms the credit, which may differ from the moment the ACH credit message arrives. Collapsing these states into a single "received" status just won’t work.

The Monzo fine is a very clear example of what happens when compliance is treated as a process owned by a compliance team rather than infrastructure owned by the engineering organisation.

At a small scale, a compliance team can manually review flagged transactions, conduct enhanced due diligence, and manage suspicious activity reporting. But when you start servicing millions of accounts, making several transactions a week, the same manual processes fail.

Transaction monitoring needs to be able to evaluate all account activity against AML risk indicators continuously.

This means it needs to consider structuring (splitting large transactions to avoid reporting thresholds), unusual transaction patterns for the account's profile, transactions to or from high-risk jurisdictions, and sudden changes in transaction volume or value.

The best way to do this is to set everything up as an event-driven service subscribed to the payment event stream.

This allows you to evaluate every transaction in near-real time against a rule engine and, increasingly, an ML model.

On top of all of that, you can set up your alerts to generate automatically, triage by risk score, and route to the compliance team only when they exceed a defined threshold.

Your compliance team just needs to review genuine exceptions.

Every customer onboarding event and every payment instruction must screen against current sanctions lists in a variety of different regions, all while running payment instructions.

The sanctions screening service integrates via API with providers like Refinitiv World-Check, Dow Jones, or LexisNexis Risk Solutions.

When a transaction or pattern exceeds the threshold for a Suspicious Activity Report, the neobank must file with FinCEN (US), the National Crime Agency (UK), or the jurisdiction's equivalent.

Filing has regulatory timing requirements, typically within 30 to 60 days of identifying the suspicious activity, and must include specific documented evidence.

To do this efficiently, you need to engineer your evidence collection, investigation routing, regulatory filing generation, and submission tracking.

This is often referred to as the compliance-as-infrastructure principle

Neobank architecture evolves as your product scales, regulatory obligations change, and strategic differentiation clarifies.

Like with Monzo, the correct architecture for a 10,000-customer MVP differs materially from the correct architecture for a licensed bank at five million customers.

Your goal gradually shifts from getting your product on the market as soon as you can with as little overhead as possible before validating your concept, to building operational resilience.

Related Reading: How Fintechs Can Scale Engineering Cheaply and Sustainably

There is a characteristic build-versus-integrate pattern that varies by stage, for each of the layers that we have discussed above.

| Layer | MVP Approach | Growth Approach | Scale Approach |

| Licensing model | BaaS sponsor bank or EMI | EMI or progress toward a banking license | Full banking license |

| Core banking | White-label platform (Mambu, Thought Machine) | Hybrid: platform for deposits, custom ledger for products | Custom core or heavily configured platform |

| KYC / identity | Third-party provider + basic state machine | Custom state machine + preferred providers | In-house risk scoring + third-party for verification mechanics |

| Card issuing | Card processor via BaaS (Marqeta, Galileo) | Direct card processor integration + in-house disputes | Own BIN (for licensed banks) + full disputes platform |

| Payment rails | Sponsor bank rails via BaaS API | Direct FedNow/RTP connectivity; expand ACH relationships | Direct payment network participation, where licensed |

| Compliance infrastructure | SaaS transaction monitoring (ComplyAdvantage) | Custom rule engine + SaaS for screening | In-house monitoring platform + automated SAR workflow |

Each of the six layers produces a characteristic failure mode when it is built incorrectly.

Neobank engineering teams typically need core banking engineers who understand double-entry ledger design and account lifecycle management.

They can also benefit from dedicated KYC/AML engineers who have built state machines, transaction monitoring rule engines, and SAR filing pipelines.

The important thing is to get people who have worked on similar projects before, so you can rest assured that they understand the technical nuances of the financial technology industry and that they understand the heavy regulations of the industry.

At Trio, we maintain a pre-vetted bench of engineers with neobank and digital banking production experience across all layers.

Since they don’t need to be assessed from the ground up and simply need to be hand-picked based on your requirements, they can be placed in 3 to 5 days.