Hire by Technology

SERVICES

Embedded finance refers to the integration of financial services, usually things like payments, banking, lending, insurance, and investing, directly into non-financial platforms and digital products.

This means that, rather than redirecting users to a bank or a separate financial application, the financial experience happens within the app they're already using, reducing bounce rates.

For fintech companies and technical leaders in non-financial businesses, it’s important to note that embedded finance has become a baseline expectation.

Users who encounter a checkout flow in 2026 and find themselves redirected to a bank's website to complete a payment will likely not stick around.

Let’s look at how embedded finance works technically, the ecosystem components involved, the specific use cases driving adoption, the compliance and security obligations that come with it, and how to build an integration strategy that scales without creating regulatory exposure.

At Trio, we work with fintech teams and non-financial companies navigating embedded finance integration.

Our staff augmentation and outsourcing models mean you can bring in engineers with direct experience in payments infrastructure, KYC workflows, and banking API integrations without committing to full-time headcount before you know exactly what you need.

Embedded finance lets you integrate financial solutions that have already been built and licensed, directly into your platforms through APIs and Banking-as-a-Service (BaaS) infrastructure.

This is very appealing because you don't need to go through all the steps of getting your own banking license or building a payment network.

Instead, you connect to existing, already-regulated infrastructure, to allow you to deliver the financial experience inside your product.

Integrating well-designed embedded finance products typically takes weeks, instead of the potential months it takes to create them, depending on complexity. These solutions also transfer much of the regulatory risk to licensed providers who carry it as their core business.

However, embedded finance doesn't mean zero compliance obligations on your side.

How you handle user data, how you screen for fraud, and which jurisdictions you operate in still create obligations that you own regardless of which provider you've integrated.

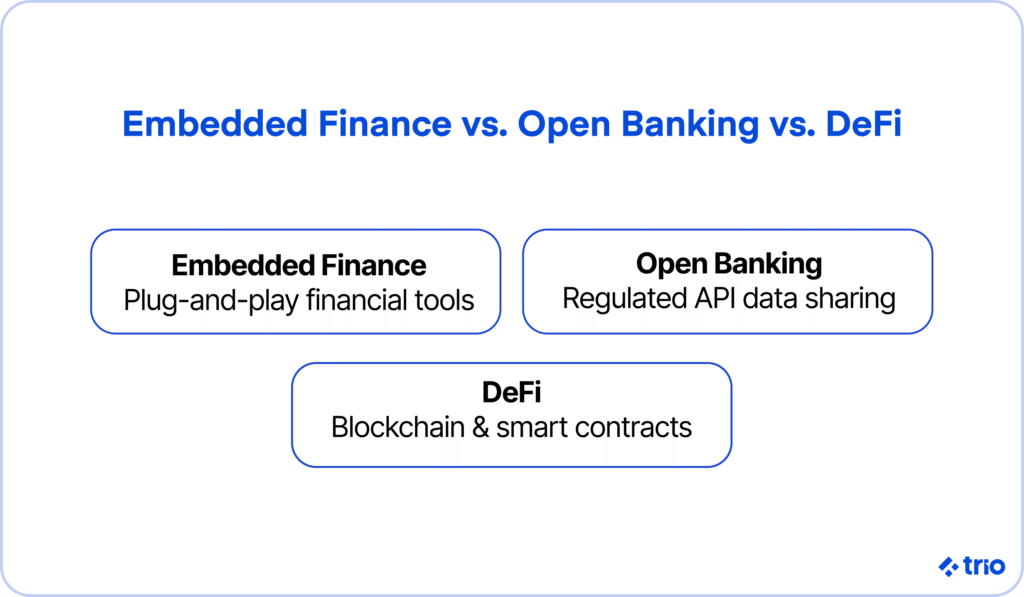

Embedded finance, open banking, and decentralized finance are sometimes confused. There are some similarities between them, but there are also some key differences that are important to be aware of.

Embedded finance describes the delivery mechanism where financial products are delivered through non-financial platforms. It focuses on the user experience and the distribution layer.

Open banking, on the other hand, describes the data-sharing infrastructure that often powers embedded finance. In open banking models, banks expose customer account data and payment initiation capabilities through regulated APIs.

Decentralized finance (DeFi) rounds these off nicely by removing intermediaries entirely through smart contracts on blockchain networks.

DeFi transactions execute programmatically without banks, brokerages, or payment processors in the chain.

If you are using embedded finance, DeFi offers a route to cross-border financial services that doesn't sit under the same regulatory frameworks as traditional banking.

These three terms are not mutually exclusive, and complex embedded finance architectures often draw on more than one.

Understanding who does what in an embedded finance integration helps clarify where risk concentrates and where your obligations begin.

Technology providers, sometimes called fintech middleware or BaaS providers, offer the API infrastructure through which embedded finance products get delivered.

In other words, they handle the technical integration layer between the financial infrastructure and your platform.

The range spans from narrow specialists to broad multi-product platforms.

A provider like Stripe (probably one of the better-known names in the industry) covers payments extensively.

On the other hand, Unit and Treasury Prime focus only on banking-as-a-service. Marqeta specializes in card issuance.

Some platforms offer multiple embedded finance products through a single API, while others go deep in one vertical.

This variety means that the right choice for your project depends on your specific use case, the geographic markets you operate in, and how much flexibility you need in the underlying financial logic.

Not all technology providers carry equivalent compliance depth, either.

A provider with strong payment processing infrastructure may have limited experience with the KYC requirements that activate when you add account issuance.

Balance sheet enablers are the licensed banks and lenders that actually hold the money, issue the cards, and take on the regulated financial risk.

They provide the banking charter, the deposit insurance, and the capital reserves that make the financial services that you need to provide possible in the first place.

If your embedded finance strategy includes offering bank accounts, issuing debit cards, or providing credit, you either need a balance sheet enabler directly or your technology provider needs to operate with one.

There are a couple of reasons why you might want to know which bank sits behind your BaaS provider.

It determines which regulatory frameworks apply to your services. It also affects your ability to pass certain compliance audits, and it determines how exposed you are if the bank relationship changes.

Embedded finance involves integrating financial services that both your business and your end users interact with. This puts most platforms in a B2B2C distribution role.

You end up being the middle layer, receiving the embedded financial tools from a provider and delivering them as an experience to your customers.

Shopify, Uber, and Toast all do this at massive scales.

In each of these cases, the platform's existing user relationship ends up being the distribution channel for financial products that users might not have thought to look for on their own.

If neither your technology provider nor your balance sheet enabler fully owns the compliance layer, and you don't have in-house regulatory expertise, embedded RegTech fills that gap.

As the name suggests, these tools handle specific compliance functions through APIs, including KYC identity verification, AML transaction monitoring, and fraud detection.

Alloy is one popular option that handles KYC and identity decisioning across multiple data sources. This allows you to run structured onboarding checks without building the logic from scratch.

Unit21 is also a good option that specializes in fraud detection and AML monitoring, while many companies use Persona to handle identity verification at the point of user onboarding.

What is great about these tools is that you can use them as modular compliance components rather than building equivalent systems in-house, which typically delivers faster compliance coverage and lower long-term maintenance costs.

If this is the way that you want to go, we have noticed that compliance facilitators work best when integrated early.

The cost of retrofitting a KYC workflow into a payment system that didn't include one at launch tends to exceed the cost of building it correctly the first time by a significant margin.

Embedded finance products can be classified into several categories. However, some companies may offer more than one type of service.

Embedded payment services are one of the most widespread categories of embedded finance, and likely the one your users encounter most often.

Most online users have encountered embedded payment options like Stripe, PayPal, and Square. These aren't built individually by every merchant that accepts them. They're embedded.

The differentiation at this layer, where there are plenty of options and functionality is not really your primary concern anymore, is conversion rate, fraud rates, and the ability to optimize routing for specific card types and geographies.

For more sophisticated platforms, embedded payment infrastructure connects to intelligent routing logic, smart retry systems, and multi-acquirer setups that improve authorization rates beyond what a single payment provider delivers.

Embedded banking platforms offer core account features, including branded debit cards, deposit accounts, and direct deposit, without operating a bank.

If you already have a captive user relationship, embedded banking changes the economics of the product. You can capture transaction data that you wouldn't otherwise see, earn interchange revenue on card spending, and even create a stickier product relationship.

The same logic applies to gig economy platforms that deposit worker earnings onto branded cards rather than through traditional bank transfers.

Buy Now Pay Later is quickly becoming a user expectation.

Users encountering a BNPL option at the point of highest purchase intent, during checkout, appear to convert at significantly higher rates than users who must seek financing separately.

Embedded credit products work on the same principle, where the financing appears exactly when the user needs it, inside the workflow where the need becomes apparent.

However, lending carries heavier regulatory obligations than payments or basic banking.

You need to deal with things like credit decisioning, disclosure requirements, and fair lending, all of which come with their own regulations that apply. Many of these vary a great deal by jurisdiction, too.

Which entity sits on the balance sheet for the loan, your platform or your provider, determines how much of that regulatory exposure you carry directly.

Embedded insurance integrates coverage directly into a purchase or service workflow, activating when your users probably need it the most.

Think of examples like travel insurance appearing during flight booking, device insurance offered at smartphone checkout, shipping protection embedded in e-commerce checkout, and even rideshare insurance activated when a driver begins a trip.

The conversion argument for embedded insurance runs on context. However, even users who don't purchase embedded insurance see that the option exists, which appears to affect trust signals around the overall product.

Robo-advisory tools, micro-investing features, and savings automation have begun appearing inside banking apps, payroll platforms, and personal finance products.

The goal is to meet users where their financial activity already concentrates rather than requiring them to open separate investment accounts.

For fintech platforms specifically, embedded wealth management features can deepen the product relationship and increase data richness without requiring a registered investment advisor license in all cases, depending on the specific feature and jurisdiction.

The benefits of embedded finance compound differently for platforms, users, and the underlying financial providers. It’s important to know where you fall.

Embedded finance's benefits come alongside challenges. We have already mentioned a couple of them, but they are worth examining in detail.

Regulatory complexity across jurisdictions is one of the most persistent challenges for platforms scaling internationally.

Your payment product might comply fully with US regulations, but may require significant architecture changes to meet PSD2 requirements in Europe or RBI guidelines in India.

Planning for multi-jurisdictional expansion at the architecture level rather than retrofitting compliance for each new market tends to produce substantially lower total cost.

Third-party risk and SLA structuring are also important to note since your vendor's outage affects your users' ability to pay, withdraw funds, or access credit.

Your vendor's security gap is your security incident. Negotiating clear SLAs with meaningful remedies, requiring SOC 2 Type II certification, and understanding your provider's incident response process become a critical part of your basic risk management.

Legacy system interoperability introduces technical complexity when integrating modern embedded finance APIs into existing platforms.

Abstraction layers, middleware, and in some cases, significant refactoring might need to happen for integrations to be realistically possible. Engineers who have built these integrations before are essential.

Finally, there seems to be a consistent tension between speed and security.

Data security, authentication, and fraud prevention systems take time to build correctly, and the consequences of getting them wrong in financial products differ from getting them wrong in other software categories. User funds and personal financial data are at stake.

A well-planned technical architecture for embedded finance reflects three priorities: security, modularity, and compliance from day zero.

An API-first architecture using REST, GraphQL, or event-driven webhooks creates the decoupled communication layer that embedded finance integrations require.

Third-party financial APIs connect to your platform without tight coupling, which makes updates or provider changes expensive. This layer also provides the abstraction needed when integrating multiple providers for different financial products.

Encrypted data handling in both transit and at rest, with clearly scoped access controls, sits at the regulatory requirement level for most embedded finance implementations.

This isn't optional based on sensitivity preference. PCI DSS, GDPR, CCPA, and equivalent regional frameworks mandate specific encryption and access control standards for financial and personal data.

Modular, cloud-native architecture with containerization and observability tooling provides the operational flexibility that embedded finance systems need.

Individual components can be updated, tested, or rolled back without touching the full system. Observability tools surface anomalies in transaction patterns or API behavior that may signal security issues before they escalate.

DevSecOps practices, including continuous integration and deployment pipelines with automated security scanning, compliance checks, and audit logging built in, make embedded finance systems maintainable at scale.

A good CI/CD policy treats security validation as a standard step in the deployment process rather than an intermittent audit event.

A few metrics appear consistently in well-run embedded finance operations as leading indicators of both business health and compliance posture.

Finding engineers with genuine embedded finance experience requires more targeted sourcing than a general software engineering search.

The domain-specific knowledge, how KYC workflows integrate with account issuance, how payment state machines handle idempotency, and how AML monitoring connects to transaction data, tends to be acquired through direct project experience rather than formal education.

At Trio, we specialize in placing fintech engineers with direct experience in payments infrastructure, embedded banking, and compliance-adjacent product development.

Our 97% placement success rate and the ability to place engineers in as little as 3-5 days reflect the depth of our vetted network rather than a generic staffing model.

If you're working through an embedded finance integration and want engineers who already speak the language of the domain, get in touch to request a consult.