Hire by Technology

SERVICES

Brazil's central bank chief reported that around 90% of the country's total crypto flow is stablecoin-related. In Argentina, USDT and USDC together account for 72% of all crypto purchases. Mexico received $61.8 billion in remittances in 2025, with stablecoins handling a growing share of that corridor.

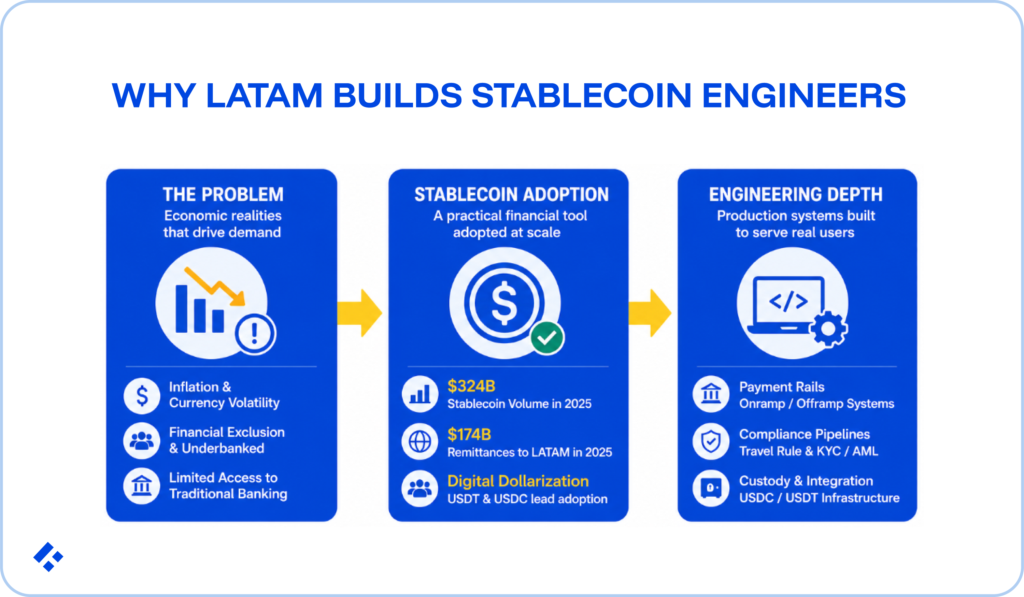

Every billion dollars of stablecoin volume required engineers to build onramp and offramp systems, payment state machines, Travel Rule compliance pipelines, custody architectures, and USDC/USDT integration layers.

LATAM is quickly becoming a stablecoin engineering hub because these developers have built these systems as production infrastructure for real users whose financial stability depended on them working correctly.

This talent is available to global fintechs if you know how to access it. But you need to understand the LATAM stablecoin landscape and what to look for in developers in order to fully take advantage of the region’s growth.

At Trio, we provide developers from these regions, pre-vetted and placed based on your specific requirements, allowing you to access them in as little as 3-5 days.

LATAM's stablecoin adoption emerged from three structural economic conditions that made stablecoins a practical survival tool and that drove engineering investment at a pace and depth no other region matched.

Over the past 15 years, average annual inflation across LATAM's five largest economies ran at approximately 13%, compared to 2.3% in the US over the same period.

In Argentina, the Argentine peso lost roughly 95% of its value against the US dollar in the five years through 2025, with peak annual inflation exceeding 200% in 2023 before President Milei's stabilisation program began taking effect.

In Venezuela, inflation reached 65,000% in a single year. This meant that holding savings in local currency created massive losses for ordinary people.

Stablecoins pegged to the US dollar offered a reliable store of value, borderless transferability, and access without the dollar bank accounts that most residents couldn't obtain.

Argentina became the region's most stablecoin-saturated market, with USDT accounting for 50% of crypto purchases and USDC for 22%. Bitcoin made up just 8%.

This is digital dollarisation, or the systematic substitution of dollar-pegged stablecoins for a currency that reliably loses value.

In Brazil, the pattern has played out differently. Lower inflation makes local currency more viable, but over 90% of the country's crypto flow still runs through stablecoins.

This is largely driven by payments, cross-border purchases, and institutional use.

Latin America and the Caribbean received a record $174 billion in total remittances in 2025.

The US-Mexico corridor, the single largest remittance corridor in the world, handled $61.8 billion of that total.

Traditional wire transfers charge 4–7% fees and take one to three business days. Stablecoins charge fractions of a cent and settle in seconds, creating a strong economic argument for using them.

Bitso, Mexico's first Bitcoin exchange, now has 9M+ users and processes $6.5 billion annually in stablecoin-based remittances, handling roughly 10% of all US-Mexico money transfers.

Building that infrastructure required engineering real onramp/offramp systems, idempotency controls, cross-border compliance pipelines, and failure-handling logic for a corridor where reliability means a family's rent arrives on time.

The stablecoin share of remittances across LATAM reached 40% in 2025, and we would not be surprised to see that share continue growing as fee differentials and settlement speed advantages compound.

Argentine fintech companies took the cross-border integration further by linking crypto rails directly to Brazil's PIX instant payment system, so users can pay Brazilian merchants in pesos while stablecoins settle the transaction behind the scenes.

Approximately 49% of Mexicans over 15 hold a traditional bank account. However, significant portions of Colombia's and Peru's populations remain outside the formal financial system.

For these users, stablecoins offered what banking couldn't: a dollar-denominated account accessible by smartphone, no credit history required, instant settlement, no minimum balance.

Colombia received approximately $11.84 billion in remittances in 2024, with fintech platforms like Nequi (24M+ users, a record 66M transactions in a single day) and DaviPlata (19M customers) building the digital payment infrastructure that stablecoin products can layer on top of.

These platforms trained engineers on building financial services for users with thin documentation, non-standard identity, and limited connectivity.

Consumer adoption at LATAM's scale and urgency required engineering infrastructure. The companies that served this demand built production stablecoin systems that processed billions of dollars for users for whom the system's reliability had direct financial consequences.

The infrastructure demand this created covers five categories:

The engineers who built this infrastructure now carry production experience that engineers in markets with less urgent stablecoin demand simply don't have.

While it is often spoken of as a singular location, LATAM's stablecoin engineering hub is not a single market.

Four countries produce distinct engineering talent with specific stablecoin specialisms, and that distinction matters more in fintech than in any other industry.

Argentina's sustained currency crisis produced a country where stablecoin engineering is mainstream fintech engineering, not a specialist domain.

The companies serving this market include Lemon Cash, Belo, Bitex, and the crypto arms of Ualá and Mercado Pago. Many of these built consumer stablecoin wallets, exchange infrastructure, and dollar-denominated savings products at national scale.

Argentina overtook Brazil in total crypto activity in the 2023/2024 period, with $91.1 billion in transfers, driven almost entirely by stablecoin use.

As we have already mentioned, the engineering talent from this ecosystem has built production stablecoin systems.

The urgency of the deployment context, engineers building for users who held their savings in USDT because the peso wasn't a viable alternative, produces a different kind of engineering instinct than building for speculative use cases.

Argentina also offers the best English proficiency in LATAM and UTC-3 timezone alignment, meaning strong daily overlap with US East Coast teams and creating practical collaboration conditions.

Brazil dominates the LATAM region with $318.8 billion in crypto value received in the Chainalysis reporting period. This represents roughly one-third of all regional crypto activity.

As discussed, over 90% of the country's crypto flows are stablecoin-related.

The institutional layer here is further advanced than anywhere else in the region:

Brazil's regulatory environment is also one of the most institutionally mature in LATAM.

The 2022 Virtual Assets Law established KYC and transaction reporting requirements under Banco Central do Brasil oversight.

A series of 2024 consultations produced licensing requirements effective in 2025, and EU adequacy proceedings produced a positive EDPB opinion in October 2025.

Mexico's stablecoin engineering depth concentrates around the US-Mexico remittance corridor.

Bitso, Mexico's first Bitcoin exchange with 9M+ users, processes $6.5 billion in annual stablecoin remittances and handles roughly 10% of all US-Mexico money transfers.

The engineering required to build and maintain that system is precisely the cross-border payment engineering that Circle's CPN is designed to coordinate at global scale.

From what we have seen, many of Mexico's engineers have built the complete cross-border stablecoin payment stack from both ends of the corridor.

If your US fintech is building on CPN or adding a LATAM payout corridor, Mexican engineers carry the production experience of the world's most active remittance market.

Colombia's stablecoin engineering story runs through its payments and digital banking infrastructure rather than a single corridor.

As discussed, the country struggled with peso devaluation and limited access to dollar bank accounts. The fintech infrastructure engineers built to serve this demand provide the high-throughput digital payment foundation that stablecoin products integrate into.

Colombia's most distinctive advantage for US fintech teams is the time zone.

Colombia Standard Time (UTC-5) is identical to US Eastern Standard Time, offering full working-day overlap, allowing for real-time collaboration on compliance decisions or payment architecture.

LATAM's stablecoin engineering depth has become globally valuable, facilitating development in US and EU fintechs.

CPN expanded into Brazil, Colombia, and Latin America as early payout markets. This happened partly because the BFI infrastructure to offramp stablecoins to local fiat already existed there.

Engineers who have built LATAM fiat onramp/offramp systems understand the BFI side of CPN flows from production experience, not documentation. The corridors CPN is building toward are corridors LATAM engineers have already built on.

Nubank's 100M+ account base has been called the most powerful stablecoin distribution channel in Latin America by analysts tracking the sector.

Its crypto product integration normalises stablecoin access for users who wouldn't necessarily have gone looking for it independently.

Engineers who have built on stacks like this understand the transaction volumes, system reliability requirements, and compliance monitoring that consumer-finance-scale stablecoin systems demand.

US and EU fintechs building stablecoin payment products in 2026 must implement Travel Rule compliance. This is a FATF requirement that originators and beneficiaries of crypto transfers above certain thresholds be identified and the information transmitted.

LATAM engineers building for cross-border remittance flows have navigated this in live production for years, including all the nuances of KYC onboarding for unbanked users with non-standard documentation, AML monitoring for the high-frequency small transactions characteristic of remittance corridors, and cross-border reporting obligations to both CNBV and FinCEN simultaneously.

A common hesitation about LATAM as a technology hub is regulatory fragility. However, it seems like the region’s regulations are stabilizing to a certain degree.

The direction of travel across these four markets runs toward institutional convergence, not away from it.

At Trio, we place pre-vetted LATAM fintech engineers, including engineers with production stablecoin experience from Argentina's crypto ecosystem, Mexico's remittance infrastructure, Colombia's high-volume digital banking platforms, and Brazil's institutional stablecoin layer.

The production experience in US and EU environments is what makes LATAM engineers valuable for stablecoin payment work and is what our vetting process confirms.

Since these developers are already vetted, they only need to be matched based on your requirements and can be placed in 3–5 days at $40–$80/hr.