Hire by Technology

SERVICES

Every year, billions of euros move between accounts that were never meant to receive them. Sometimes this is because of honest mistakes, but there are also many instances where it’s part of a scam that looks convincing until it's too late.

Either way, those in the fintech industry understand that the result is the same, with lost money, regulatory pressure, and shaken trust.

That's where Verification of Payee (VoP) comes in. It's a name-account matching framework designed to confirm that the person you think you're paying actually holds the account receiving the money.

The VoP framework became a mandatory requirement in the EU as of October 2025, and it appears to be quickly becoming the baseline globally.

As the world moves toward full instant payments, VoP may well prove to be the missing link that protects users from both mistakes and fraudsters.

If you work with payments, compliance, or infrastructure, this change matters.

Payment Service Providers (PSPs) across the EU need to integrate VoP checks. If you operate in the EU or expect to expand into the region, you need to consider the regulations.

Getting implementation right is going to be critical for compliance going forward. An expert fintech developer who understands both the technical and regulatory sides of VoP can help you avoid costly mistakes.

At Trio, we provide cost-effective developers familiar with the regulatory environment of both the US and the EU, through outsourcing and staff augmentation.

Book a security-ready consult.

Before we take a look at why this matters, it helps to know what VoP actually does under the hood.

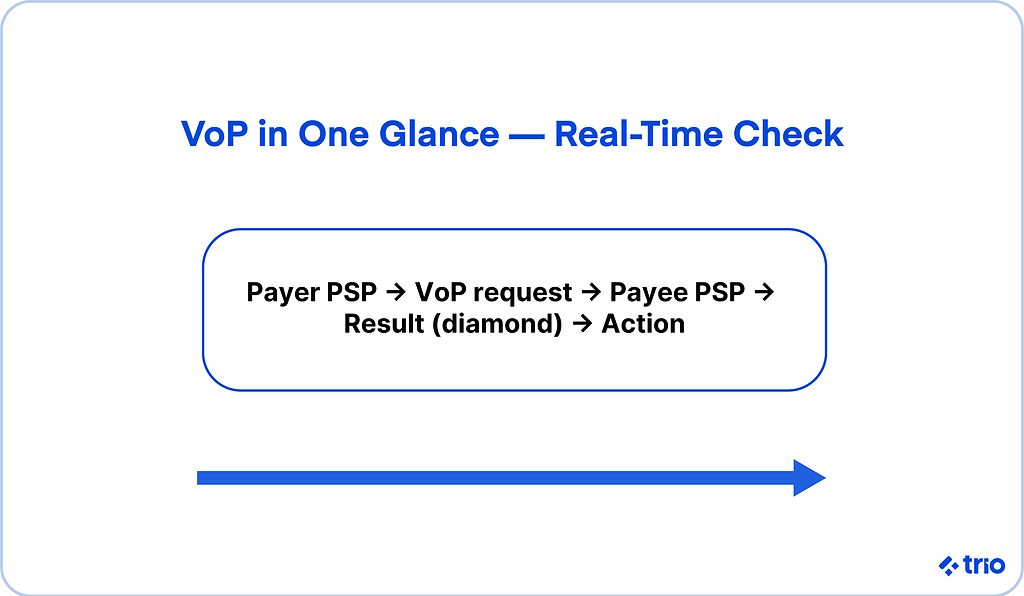

Verification of Payee, or VoP, runs a payee name matching check before a transaction executes.

When one of your customers enters an International Bank Account Number (IBAN) or account number, the sending PSP sends a VoP request to the receiving PSP to confirm whether the registered account name matches what was entered.

If everything looks good and the account name matches, the payment proceeds. If it's a "close match," the payer gets a notification to review the details. If it's a "no match," the transfer stops before any funds move.

The idea behind VoP is to prevent issues like misdirected payments and authorized push payment (APP) fraud before they happen, instead of cleaning up after the fact.

In doing so, you get to increase user trust, without needing them to verify everything all the time.

Regulators tend to focus on compliance, but for many companies, the real benefit of VoP comes down to confidence, for both institutions and customers.

There are a couple of different ways that this is done.

APP (Authorized Push Payment) fraud has grown sharply in recent years. Unlike in the past, though, you now face the added risk of fraud leading to instant transfers that can't be reversed.

In the UK, where a similar system called Confirmation of Payee already exists, banks reported double-digit drops in payment fraud after rollout.

The data varies by institution, but the trend of reduced fraud success is pretty consistent.

Under the Instant Payment Regulation (IPR), PSPs had to implement VoP by 9 October 2025.

This requirement ties directly to SEPA instant credit transfers and SEPA credit transfers. PSPs offering SCT Inst, the SEPA instant credit transfer scheme, faced the earliest compliance obligation.

This more recent regulation gives EU banks and fintechs a set of simple compliance requirements while genuinely improving operational security.

Customers lose patience with friction, which means they are more likely to abandon their transactions.

But VoP, when done well, won't slow down your payment processes. In fact, users might even find the overall experience of sending money smoother.

Real-time validation means fewer failed transactions, less confusion, and fewer calls to customer support.

One of the primary reasons why we have seen cross-border payments break down is because of mismatched data and different standards.

Adding a VoP check improves payment accuracy and helps keep transfers flowing between EU countries and even across other continents.

Unfortunately, we aren’t at a point where VoP has reached full interoperability beyond the SEPA zone yet. But it represents a clear step toward consistent payment securitization.

Getting VoP live requires a technical project that touches APIs, data flow, and security policies. Having experts with real production experience in financial applications is one of the best ways to ensure that things go smoothly.

Here are some of the different components that you will need to consider.

As we have already alluded to, VoP is probably not going to stop at domestic payments. But how quickly it spreads will likely depend on how well the SEPA zone rollout holds up in practice.

The EU aims to extend VoP across cross-border instant payments within the SEPA zone.

This approach will likely build on existing SWIFT GPI and ISO 20022 data standards to ensure data consistency and interoperability.

On top of that, when every payer knows that recipient identities undergo verification before money moves, confidence grows.

That trust makes instant payments more attractive and cuts reliance on intermediaries who add cost and delay.

SWIFT GPI already tracks payments globally with improved transparency. Combining that with VoP systems and ISO 20022 message formats could standardize payment verification from initiation to settlement.

That alignment demands serious technical work, but that technical groundwork is exactly how interoperability gets built across the payments landscape.

Consistency is the only thing that is going to make VoP scalable. The fewer format differences between PSPs, the faster payments clear.

Our developers have already started thinking about what happens when on-chain identity meets regulated finance.

In theory, blockchain-based identity systems could carry verified credentials that interact with traditional payment rails.

Early-stage work in this area hints at a world where verifying ownership of a wallet address could mirror how IBAN-based bank account verification works today.

Smart contracts could eventually enforce VoP-like logic by releasing funds only if a payee's name matches verified credentials.

Some of the developments we've touched on seem more likely to arrive in the near term than others.

Verification of Payee (VoP) is a great move towards ensuring payment security in Europe.

We hope that it will continue to help fintechs and EU banks prevent fraud, reduce manual payment checks, and bring a level of payee name verification that should have existed years ago.

The 9 October 2025 deadline has already passed, so if you aren’t already using VoP in your own payment systems, you are at risk for compliance issues.

If you need to hire fintech developers to help you implement VoP, reduce fraud, and ensure regulatory compliance across the EU, get in touch to talk to an expert.