Hire by Technology

SERVICES

Circle announced Circle Payments Network on April 21, 2025, with the mainnet going live roughly a month later. Growth since then has been fast.

CPN has added fiat payout corridors in Brazil, China, Colombia, Hong Kong, Nigeria, and across parts of Latin America, working with BFIs like Alfred, TazaPay, and Yellow Card.

If your fintech is building cross-border payment capability, CPN solves the many-to-many correspondent relationship problem. Instead of negotiating bilateral agreements with payout partners in every new market, you connect to CPN once.

This allows you to reach BFI payout markets globally through a single API and agreement.

What CPN doesn't solve is the engineering complexity of the integration itself.

Any fintech connecting as an OFI still has to build the fiat-to-USDC onramp, implement the CPN API flow, handle on-chain USDC signing, integrate Travel Rule data exchange, and manage the chain-routing logic that gets USDC onto whatever blockchain the BFI supports.

That is exactly the kind of talent we keep in our pre-vetted pool at Trio.

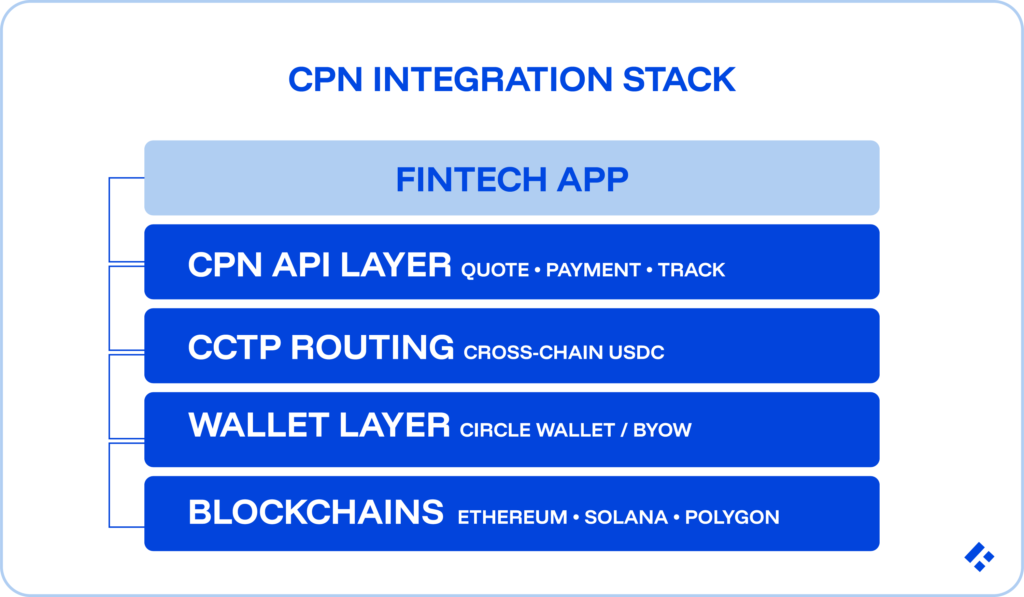

Circle Payments Network is a coordination protocol that uses USDC as the settlement medium.

Circle Technology Services (CTS) operates CPN as the technology service provider, but Circle isn't holding or moving the funds.

Instead, CPN just acts as the orchestration layer that routes payment messages between OFIs and BFIs, coordinates Travel Rule data exchange, and tracks settlement status as a payment moves through the network.

A custody solution (the fintech still holds its own USDC in its own wallet), an onramp (the OFI handles fiat-to-USDC conversion on its own).

A blockchain (CPN runs above Ethereum, Polygon, and Solana, with broader EVM-compatible support expanding).

A replacement for blockchain transaction mechanics, signing, gas, and finality still sit squarely on the OFI's plate.

CPN adds an API coordination layer on top of a raw USDC integration, not in place of one.

This means that an engineer building on CPN needs both the blockchain mechanics and the CPN protocol understanding; having only one or the other leaves a real gap.

CPN has two participant roles, and which one a fintech fills determines which engineering responsibilities it actually owns.

Most fintechs connecting to CPN start by building as OFIs, since that's the path to reaching global payout markets for whatever payment product they're building.

Some eventually build BFI capability too, to capture inbound flow rather than only sending it out.

The CPN API is the primary surface against which OFI integration is built. Circle's developer documentation lays out four steps that sequence a complete cross-border payment.

CPN's Travel Rule pre-check endpoint lets an OFI programmatically confirm the exact Travel Rule data requirements for a given geography or BFI before sending the payment.

Travel Rule data is one of the most common reasons a new corridor's first integration attempts get rejected, specifically when the pre-check catches that before the payment goes out, rather than after.

Circle has also automated the request-for-information (RFI) loop between OFI and BFI, and added an automated reversals endpoint for exception handling without the usual support-ticket cycle.

CPN currently supports Ethereum, Polygon, and Solana as named settlement chains, with broader EVM-compatible support continuing to expand.

This means that whichever chain the BFI supports determines which blockchain the OFI needs to deliver USDC on.

When the OFI's own USDC sits on a different chain than the target BFI requires, the engineer needs to bridge first using Circle's Cross-Chain Transfer Protocol before initiating the CPN payment at all.

The routing pattern looks like this in practice: figure out which chain holds the OFI's USDC balance, figure out which chain the target BFI supports on CPN, and if those two chains differ, use CCTP to burn USDC on the source chain and mint native USDC on the destination chain.

Only once the USDC actually sits on the BFI's supported chain does the CPN payment get initiated.

CCTP itself has moved fast. CCTP V2, which adds Fast Transfer for faster-than-finality settlement and Hooks for post-transfer automation, is now the canonical version going forward, with CCTP V1 being phased out starting July 31, 2026.

This means that you will need an engineer who understands both the CPN API flow and the CCTP burn-and-mint mechanism together.

The OFI's operational USDC wallet, which actually holds the balance and signs on-chain transactions, gets provisioned one of two ways.

Circle manages key custody and transaction signing on the OFI's behalf.

Your engineer integrates against the Programmable Wallet API for balance management, signing requests, and confirmation monitoring, without ever touching the blockchain directly.

Onboarding moves faster this way, since custody is delegated entirely to Circle.

In this option, the OFI manages its own key infrastructure, typically through an MPC provider like Fireblocks or Copper, or an HSM-backed signing setup.

Your developers will need to implement direct blockchain interactions for signing, gas management, and event monitoring.

The primary benefit here is that you get full custody control, but there is meaningfully more engineering complexity to get right.

Most fintechs starting a CPN integration go with Option 1 to reduce time-to-live, then migrate to Option 2 later as transaction volume grows and custody control becomes more important.

Travel Rule compliance sits embedded directly in the CPN protocol rather than bolted on afterward.

For cross-border payments above the applicable threshold (€1,000 in the EU under the Transfer of Funds Regulation, $3,000 in the US under FinCEN rules), originator and beneficiary identifying information have to travel alongside the transaction.

The CPN then handles that data exchange between OFI and BFI with end-to-end encryption throughout.

The engineering work on the OFI side covers collecting complete originator data at the payment creation step (full legal name, account number, address, date of birth, national ID where required), using the pre-check API to confirm exactly what's required for a given corridor before payment initiation, handling BFI requests for additional information if the initial data submission isn't enough, and handling Travel Rule-related rejections gracefully.

Arc is Circle's own enterprise-grade layer-1 blockchain. It is built specifically for institutional financial applications, deterministic finality, compliance-aware transaction handling, and native USDC support.

Right now, CPN's integration with Arc has been described as in progress, with support expected once Arc reaches mainnet.

We suspect that Arc will become a supported settlement chain, and native USDC on Arc should mean faster finality than Ethereum for certain corridors and tighter integration with Circle's broader product stack, USYC, EURC, and partner-launched stablecoins among them.

Arc is EVM-compatible, so engineers already comfortable with Ethereum's ERC-20 mechanics and tooling like ethers.js or viem carry that knowledge straight across.

The chain-selection logic built into CCTP routing today will need to account for Arc as a destination once BFIs start onboarding to it.

Pulling all of this together, an engineer who can build a production CPN OFI integration needs the following skills:

CPN's payout market expansion into Brazil, Colombia, and across Latin America creates a fairly direct alignment with where LATAM fintech engineering talent has actually been building.

Engineers who've worked on remittance infrastructure along the US-Mexico corridor, on stablecoin payment products in Argentina at companies like Lemon Cash and Belo, or on high-volume digital banking infrastructure in Colombia at places like Nequi, have already built the foundational skills a CPN OFI integration draws on.

If you are adding CPN capability, these engineers don't need to learn cross-border stablecoin payments from a standing start. They bring the domain context already, so the CPN-specific API layer is a relatively easily learnable surface that sits on top of that.

At Trio, we place pre-vetted LATAM fintech engineers with stablecoin payment and cross-border payment experience, engineers who've built inside the same ecosystems that CPN's LATAM payout corridors are designed to serve.

If your fintech is building a CPN OFI integration, that means sourcing engineers with production USDC payment integration experience.

Through our staff augmentation model, these engineers can be placed in 3-5 days at $40-$80/hr, with timezone overlap running 4-8 hours against US teams and full-day overlap.