Hire by Technology

SERVICES

Legacy system modernization is one of the most significant challenges that we see established fintech and banking teams face today.

The industry keeps evolving, and working with outdated systems can significantly hinder your progress, causing you to fall behind your competitors and accumulate even more technical debt.

Additionally, a lot of legacy platforms are more vulnerable to security breaches. Since you're likely handling sensitive financial data, even a single, small breach can prove enough to damage your clients' perception of your trustworthiness and threaten your entire company.

Understanding the challenges legacy systems present and choosing the right modernization approach for your situation matters for the continued success of your fintech company.

Let’s take a look at everything you need to know to transition your legacy infrastructure into more modern core systems, including AI-assisted modernization, common strategies such as rehosting and replatforming, refactoring legacy code, adopting a microservices architecture (including the strangler pattern), API-led modernization, and best practices for cloud migration.

At Trio, we've helped countless financial services organizations migrate to new systems and supported the modernization of legacy software. Our developers carry industry experience and understand the unique business needs that arise in the financial technology sector, so your modernization doesn't introduce new compliance gaps while closing old ones.

Through agile development, they collaborate with your existing team to build solutions you can adapt over the long term.

When people talk about a legacy system in a fintech context, it generally refers to outdated technology that ultimately limits the performance of user-facing features or some sort of backend financial system.

Think of the core banking infrastructure that banks built decades ago, or the payment systems the stock exchange still runs on. These systems were built for stability and batch processing, not for the always-on, API-first digital banking world customers expect today.

McKinsey estimates that 70% of the software used by Fortune 500 companies was developed 20 or more years ago.

From what we have seen in financial services, that figure likely runs higher because the cost and risk of replacing revenue-critical systems has historically led institutions to defer modernization in favor of a bunch of small patches.

Most legacy systems run on a monolithic architecture, which can make it difficult to make small changes without rewriting the entire codebase.

Many banking platforms also struggle with legacy software built on outdated frameworks, those that no longer receive support and updates, COBOL-based infrastructure, or siloed, on-premises databases.

These types of technology create problems in the fintech landscape because they cannot integrate with today's cloud-native tools, and their real-time capabilities may be severely limited.

A core banking system that processes transactions in overnight batches cannot support the instant payment expectations that modern customers carry.

The fintech industry is one of the most heavily regulated in the world, which makes sense considering the information that you are dealing with.

To receive the necessary certifications and approvals to work in certain regions, systems must remain secure, audit-ready, and flexible.

The latter matters because the regulatory compliance landscape keeps shifting, which requires continuous adjustment.

It’s also important to note that PSD2, GDPR, and evolving AML requirements all apply throughout a migration, not just after it's complete, which adds another element of difficulty to the modernization process.

Legacy systems often struggle with performance and data-handling issues. If any of these are further affected by the migration process, it can lead to downtime or other problems that damage your company's reputation and user perception of your trustworthiness.

There are several reasons that make transitioning to modern banking systems essential for fintech companies:

The original calculation around legacy modernization included several years of planning, months of downtime risk, and hundreds of thousands of dollars in consulting fees, which have changed materially because of AI.

The newer technology has made it faster and less disruptive, allowing more companies to consider modernization instead of a complete rebuild.

One of the most consistent blockers for legacy modernization projects involves institutional knowledge gaps.

You need people on your team who understand the system and why it does what it does.

However, we work with many companies where nobody has this information because the original developers left years ago, and the documentation was never updated.

AI and machine learning models can now analyze legacy codebases, map dependencies, identify hidden relationships between components, and generate documentation automatically.

AI can also generate refactored versions of your code, propose modular rewrites, and create automated test suites for validating that modernized components behave identically to the systems they replace.

For fintech modernization specifically, automated test generation addresses one of the highest-risk phases of migration: confirming that payment processing logic, AML monitoring, and audit trail generation all work exactly as intended.

Manual testing alone used to take months. AI-generated test suites can cover a significantly higher proportion of code paths in a fraction of that time.

COBOL-based core banking systems present a particular challenge because the talent pool that understands them shrinks every year.

Generative AI can now translate COBOL into modern languages at a level of accuracy that makes AI-assisted translation a viable starting point for core system migration, rather than a curiosity.

The output still requires expert review, particularly for compliance-critical payment processing logic, but it compresses the migration timeline substantially.

It’s important to note that, while AI handles pattern recognition, code analysis, and test generation well, it tends to struggle with business logic that requires a regulatory context to interpret correctly.

A payment workflow that behaves in a specific way because of a jurisdictional compliance requirement doesn't always declare itself as such in the code.

Human oversight from developers who understand both the technical and regulatory environment is still absolutely critical, which is one reason generative AI works best as a force multiplier for experienced fintech engineers rather than a replacement for them.

Before your team can start the modernization process, you need to identify which portions of your legacy systems may hold you back the most, so you understand where to focus your initial efforts.

There are three main types of tech debt: intentional, accidental, and legacy. Each of these carries different implications for how you prioritize.

Once you understand where your systems hold your app back the most, you need to decide the order of remediation.

You could prioritize based on risk, frequency, or a value matrix.

In our experience, it’s best to start with systems that create compliance exposure or that directly affect payment processing or audit trails.

Rehosting, replatforming, refactoring legacy code, adopting microservices architecture, API-led modernization, and cloud migration all have their place.

Instead of there being a one-size-fits-all solution, the right choice depends on how outdated your legacy core is, what your compliance obligations look like during migration, and how much disruption your business can absorb.

Rehosting moves your app over to a new infrastructure environment without changing your existing code.

Replatforming involves only a couple of changes to ensure your product performs well in the new environment.

When our developers have assisted in replatforming, some of the changes have included moving to containerized deployments or a cloud-based system.

While these strategies work quickly and efficiently, they don't suit systems that are too outdated to benefit from a new environment alone.

A COBOL-based core banking system on modern cloud infrastructure is still going to be a COBOL system, just hosted differently.

Refactoring suits legacy systems built on a monolithic architecture.

It usually involves modularizing code, replacing weak logic, and addressing imminent tech debt to shift outdated systems toward modern expectations in preparation for something like service extraction or cloud migration.

This process can assist greatly with efficient data handling, automation, and handling traffic peaks.

AI-assisted refactoring tools have significantly reduced the manual effort this process historically required, particularly for dependency mapping and initial code restructuring, as we have mentioned above.

Microservices architecture enables fintech companies to break their apps into modular, independently deployable services.

It's typically the next step after refactoring, and it changes the failure model significantly.

With everything in individual pieces, you can iterate on individual components rapidly, scale faster, and your app becomes generally more resilient since only one component fails at a time.

The Strangler pattern is one example of how you can transition to a microservices architecture. Essentially, you build a new service that mimics the function of the legacy system and slowly takes over for it.

This means your team can rewrite smaller sections at a time and validate each piece before moving forward, which keeps the migration auditable and reduces compliance risk during the transition.

APIs let you integrate third-party services by allowing you to expose your core business logic without opening yourself up to potential security risks.

Getting outdated systems ready for API integration means that you can isolate functionality and take advantage of third-party integrations to support faster innovation going forward.

OpenLegacy and similar platforms now offer automated API generation that can surface legacy core system functions as modern REST APIs without requiring a complete rewrite, which makes this approach available to institutions whose legacy core is too complex to refactor quickly.

Migrating data from legacy systems to cloud platforms becomes necessary for any real-time fintech features. But the data needs preparation before migration becomes possible.

You need data classification, audit readiness, and reliable testing.

A good strategy is to start with non-critical services. You can also consider using simulations to validate that migration has occurred successfully, which substantially reduces risk.

Just make sure that the platform you are moving to is fintech-compliant.

GCP (Google Cloud Platform) is generally a popular option, but AWS (Amazon Web Services) may suit specific workloads too.

Both offer cloud-native architecture options that support regulatory compliance requirements, though your specific obligations under PSD2, GDPR, or other frameworks should shape which environment you choose for each component.

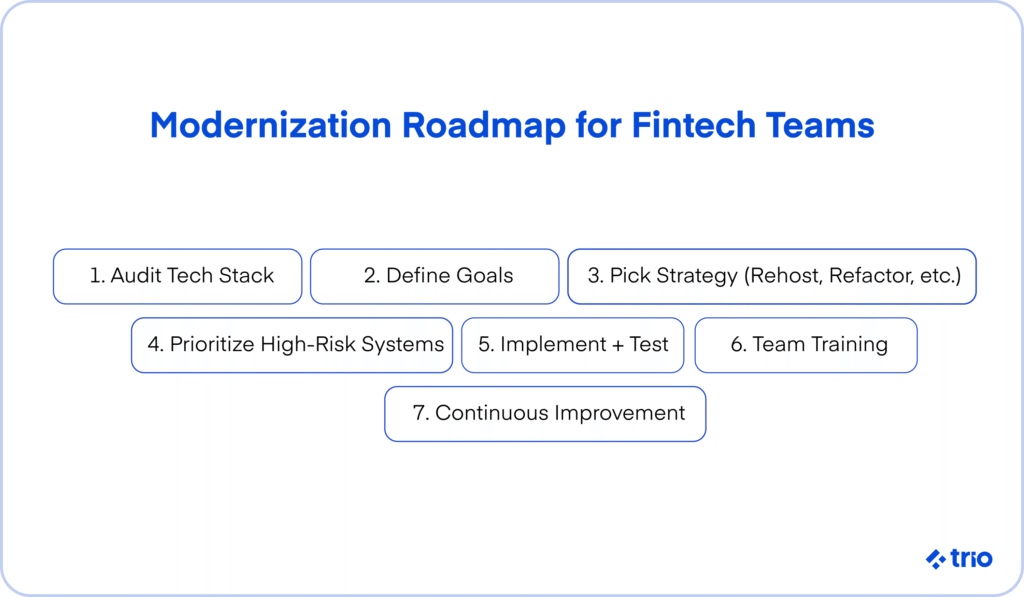

Upgrading legacy systems can feel overwhelming. Here is a step-by-step roadmap to guide you through the modernization process.

Regulatory compliance and audit readiness both improve immediately when your core systems can generate the audit trails, access logs, and real-time monitoring outputs that modern regulators expect.

Legacy infrastructure that processes transactions in batches and stores logs in proprietary formats creates genuine compliance exposure under GDPR and PSD2, which cloud-native alternatives handle natively.

Customer experience transformation follows from real-time data access. A digital banking app built on modern core banking systems can show a pending transaction within seconds.

Then you need to consider how the cost of ownership drops over time despite the upfront modernization investment. Modernized cloud-native infrastructure is typically far cheaper, freeing up your budget for other development.

Finally, scalability and flexibility improve in ways that support both growth and regulatory adaptation.

When regulations change, your teams can update compliance logic in a specific microservice rather than touching monolithic code that no one fully understands anymore.

AI and machine learning have changed the modernization equation by making code analysis, documentation, and test generation faster and more reliable than the purely manual approach allowed.

That doesn't eliminate the need for experienced engineers, particularly in regulated fintech environments where compliance obligations don't pause during migration. It makes those engineers significantly more productive.

If you want additional talent to help ensure the modernization of your legacy fintech systems goes smoothly, we can help.

Our developers integrate well into your existing team, giving you everything you could want from a permanent hire without the commitment of one.

If you want more information or are ready to get started, request a consult.