Hire by Technology

SERVICES

If you work in fintech, you already know that onboarding can make or break your app. Those first few moments from sign-up to verification carry real weight. They define how much users trust you with their financial data and how confidently your team can scale.

Even a small delay or a confusing form can trigger user drop-offs, and the data backs that up: over 74% of companies now maintain a dedicated customer onboarding team. But it's not just about the customer journey.

For fintech companies, developer onboarding carries just as much weight. When engineers can quickly set up secure environments and integrate APIs safely, your fintech onboarding process builds into a long-term competitive advantage.

At Trio, we've worked with fintech startups and enterprises to build onboarding flows that are proven to convert, as well as ensure compliance.

Onboarding in fintech is a cross-functional process that connects design, development, and compliance into one experience that feels simple to the user but runs deeply secure underneath.

This is also where your major compliance work needs to start.

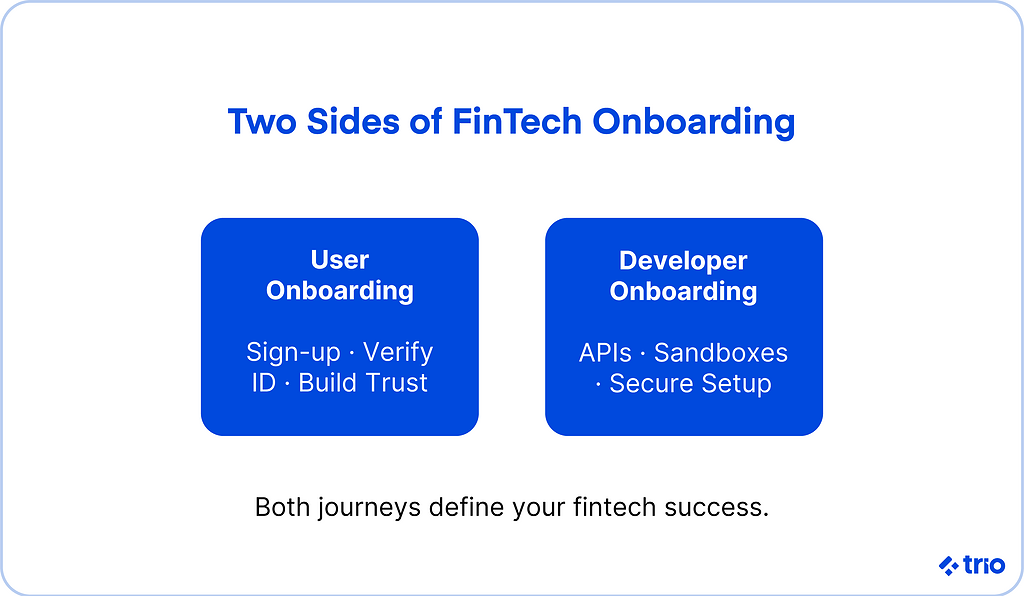

The term fintech onboarding covers both user onboarding and developer onboarding.

For new customers, the onboarding flow takes them from sign-up to activation, often including identity verification and consent.

For developers, this is the process of starting developers out in your team and providing a structured way to introduce them to your APIs, data models, and compliance frameworks.

You need to consider both of these sets of fintech onboarding to make sure that you can continue to scale in a competitive market by gaining and keeping both new clients and the skill set to continue providing services to them.

Most fintech onboarding flows, whether for a budgeting app, a crypto platform, or a lending product, follow a pretty similar sequence, which users have started to expect. Understanding each step helps you identify where friction tends to accumulate.

From a user's point of view, a smooth onboarding process makes it easy to get started with your product and conveys information about the quality of your product and your attention to detail.

Clients want to create an account, verify their identity, and make their first deposit without friction.

For software developers, onboarding covers understanding how to maintain security measures, manage sensitive information such as Social Security numbers, and comply with AML requirements.

It's what minimizes the chances of them making mistakes and decreases the time it takes for them to start contributing productively.

Companies that prioritize developer onboarding early tend to ship features faster and with fewer incidents, and the connection to user experience runs more directly than most teams expect.

As we have already mentioned, the way in which you onboard your clients can create an impression of your product.

A confusing or slow onboarding flow makes users question your reliability.

If there weren't many options, it wouldn't be a problem, but in a competitive market where comparable fintech products often exist, this can lead to an instant loss.

A transparent, end-to-end secure onboarding process signals that your fintech app values safety and user experience equally.

Building a strong onboarding process means combining UX simplicity with technical rigor. There are several key components and best practices for each of those that you need to consider.

Identity verification and Know Your Customer (KYC) requirements form the backbone of any secure fintech onboarding process.

Anti-Money Laundering (AML) regulations aim to prevent fraud, but they can take extensive time and effort to ensure they are compliant. Automation can assist in lightening this load.

Tools like real-time document verification and two-factor authentication can verify users while keeping friction low.

Outside of automation, another technique we've seen consistently decrease onboarding time is to implement API-driven KYC checks with progressive validation. In doing this, users only see the next requirement after completing the current one.

For higher-risk profiles, enhanced due diligence steps may be required. Instead of creating entirely different flows, we recommend that you build those flows so they feel like a natural continuation of the existing onboarding journey.

We have found that a sudden escalation tends to reduce abandonment among users who are legitimately high-value but happen to trigger AML risk signals.

Every interaction inside a fintech app involves sensitive information. Being upfront about how you handle it costs nothing and tends to build meaningful trust, but that only works if you are handling information in a compliant manner.

Clear messaging like "your data gets encrypted," "we comply with GDPR," or "you can revoke consent anytime" reassures users. This is critical since it is when providing their information that they will likely hesitate.

Small transparency cues like visual locks during data entry and plain-language explanations of why each piece of information gets requested all contribute to additional trust, too.

A budgeting app might focus on linking a bank account, while a crypto platform emphasizes wallet verification. Assuming that every user has similar needs and using a standardized template often leads to less-than-ideal results.

Instead, we recommend personalized prompts, contextual help, and in-app guidance to help make the onboarding flow feel more tailored.

Personalized messages triggered by specific user behavior, like a gentle push notification when someone pauses mid-verification, can recover onboarding sessions that would otherwise end as abandoned drop-offs.

Related Reading: Hire AI Developers

Consumer fintech onboarding and B2B fintech onboarding share the same compliance requirements but operate quite differently in practice.

When a fintech platform onboards an enterprise client, the onboarding journey typically involves multiple stakeholders on both sides. You might need to onboard a technical contact, a finance approver, a legal reviewer, and often a compliance officer. This means that one sign-up form isn't going to work.

B2B fintech onboarding that tends to convert well usually involves:

Enterprise clients tend to provide enough business to make this added work worthwhile for you.

Developer onboarding in fintech carries specific weight that general onboarding guides tend to understate.

A developer who understands your compliance context from day one makes fewer architectural decisions that need reversing later. One who doesn't tends to create rework at the worst possible moments.

The stakes are also retention-related.

Research consistently shows that developers who go through structured onboarding are significantly more likely to stay with a company long-term.

In fintech, where a developer builds institutional knowledge about your payment flows, KYC logic, and AML implementation over months, that retention gap has a real cost that shows up in delivery speed and compliance risk.

We often see the administrative and access side of developer onboarding get underinvested in. This creates friction on day one that reverberates for weeks.

Before your new developer starts, make sure they have access to everything they need to be productive without having to ask for it.

This includes:

The first conversation with a new fintech developer should set expectations in both directions.

We recommend that you include things like what the company needs from them and what they can expect from the company.

For fintech specifically, this means covering:

Regardless of how strong a hire someone is, dropping a new developer directly into compliance-critical payment code during week one tends to go poorly.

We recommend that you give new fintech developers a first week or two of smaller, non-critical tasks, like a well-scoped feature, a documentation update, or a test suite improvement.

This lets them build familiarity with the codebase and the compliance conventions without the cost of a mistake being high.

Once they've demonstrated they understand the patterns, moving them into more sensitive areas of the codebase carries less risk.

A clear developer fintech onboarding process usually starts with:

Make sure every new developer has documented access to:

Pairing a new fintech developer with a more senior engineer who knows the codebase accelerates ramp-up in ways that documentation alone can't.

The senior developer provides the new hire with useful context, a backlog of institutional knowledge about why certain decisions were made, and a low-friction way to ask questions that don't belong in a ticket.

Even a lightweight structure, like a daily check-in for the first two weeks and then weekly as needed, delivers significantly better results than leaving a new fintech developer to figure things out independently.

Fintech apps often depend on integrations, from open banking to identity verification to payment gateways. Developers need clarity on data flow and failure states.

Documenting each API's purpose, rate limits, expected response codes, and error handling reduces confusion for engineers new to the platform.

API-first onboarding, where you provide example payloads in the developer dashboard, is one technique that we often use to speed up integration and reduce the risk of compliance errors.

Developers need to build their understanding of the security context.

Introduce encryption protocols, key management standards, and audit trail expectations at the start of the onboarding process, not as an afterthought once they've already built something non-compliant.

When they understand why a rule exists, your developers will be more likely to implement it correctly.

A new developer who doesn't know their teammates, doesn't understand the communication norms, and isn't sure what's acceptable to ask questions about will underperform relative to their actual capability.

It can be helpful for you to announce new developers to the team, make introductions to the people they'll work most closely with, and be explicit about communication norms rather than leaving them to figure it out.

In regulated environments specifically, being clear about when to escalate a concern versus handle it independently saves real problems downstream.

Weekly 1-on-1s in the first few months, which we have already mentioned, could be a great way to implement the buddy system, give you a consistent channel to catch problems early, celebrate early wins, and adjust pace if needed.

In a fintech context, these check-ins also let you catch compliance-relevant misunderstandings before they manifest in code.

A new developer who is slightly uncertain about how your AML pipeline works but doesn't raise it will often make a decision that seems reasonable to them and creates a problem you discover much later.

When product, legal, and engineering teams work together, compliance stops feeling like a roadblock and starts feeling like a shared mission.

This means that you need developers with the soft skills to be able to communicate between teams in ways that everyone can understand.

This shift in framing tends to produce fewer last-minute compliance delays before launch, because the legal requirements get absorbed into the engineering workflow early rather than imposed on top of it.

Fintech moves fast enough that a developer's knowledge depreciates meaningfully within a year or two if they don't stay current. Regulatory frameworks change, payment standards evolve, and security requirements tighten.

Creating a learning plan for your fintech developers, one that targets both their current skill gaps and the domain knowledge that's most relevant to your product, keeps the team sharp and signals that you're invested in their long-term growth.

From what we have seen, developers who feel like they're growing with a company tend to stay as well.

You can't improve what you don't measure, and fintech onboarding flows produce more measurable signals than most teams fully use.

The most actionable onboarding analytics tend to track:

Amplitude and similar product analytics platforms let fintech teams track these signals at a granular level.

Most user drop-offs occur during verification or when users encounter unexpected friction, such as additional ID requests or slow document uploads.

Fraudsters represent a separate but related problem.

Well-designed KYC flows deter many fraud attempts simply by being thorough, but they can also create false positives that reject legitimate new customers.

Calibrating that balance requires both risk analysis and ongoing review of verification rejection rates.

Developers experience their own version of drop-offs when internal APIs lack documentation or sandbox data becomes outdated.

You can reduce drop-offs with thoughtful UX details:

Some fintech apps now use machine learning to personalize onboarding steps in real-time.

If a user hesitates on a certain page, the system can offer instant customer support or reduce the number of visible fields to help them continue.

Analytics, when used alongside AI, helps identify early friction signals, such as repeated verification retries or slow uploads, and provides gentle guidance before the user decides to abandon the process entirely.

Fintech onboarding requires a shared effort between design, engineering, and compliance teams to get the best result.

If done correctly, the fintech onboarding process becomes an opportunity to build trust, reduce friction, and support long-term retention. That applies equally to user onboarding and developer onboarding.

We've seen this firsthand at Trio. When fintech teams invest in well-structured developer onboarding, they also deliver better user onboarding. Faster integrations, fewer drop-offs, stronger compliance alignment: it all starts there.

However, for any successful software development, you need experts on your team.

If you're ready to start hiring and onboarding developers for your fintech projects, book a security-ready consult.