Hire by Technology

SERVICES

For many businesses, card networks and intermediaries quietly eat away at margins through things like payment processing fees. On top of the fees, going through these middlemen means settlement takes longer than it should, and every extra step in the chain is another point of friction for customers who want to pay and move on.

There are also additional frustrations that come with a lack of control. You’re subject to their rules and their limits on what data you can actually access. If you’re building platforms or scaling internationally, that lack of visibility makes planning harder and compliance riskier.

Account-to-account (A2A) payments are often held up as the alternative.

The idea of A2A payments is that your customers can move money directly between bank accounts, bypassing card networks altogether.

But while the concept appears straightforward, the execution can be anything but.

Not all banks support real-time transfers, and the regulations around integrations that facilitate this can vary widely by region. You also only reap the benefits, like lower costs and faster settlement, with correct implementation.

Let’s walk through what A2A payments are, why they’ve become a bigger part of the conversation in global payments, and where the real opportunities (and challenges) lie for businesses considering them.

At Trio, our expert developers specialize in difficult implementations and developing the latest technology available in fintech.

As we have already mentioned, the simplest way to think about A2A payments is just money moving directly from one bank account to another.

No card networks. No intermediaries skimming a fee along the way.

If you want to increase efficiency or decrease costs, it’s a good option to consider.

You may have also come across the term “Pay-by-Bank”, particularly if you are in e-commerce.

A lot of people use the term interchangeably with A2A, but there are a couple of differences you need to think about.

All A2A payments are technically Pay by Bank, but not all Pay by Bank implementations are true A2A transfers. Some Pay by Bank instances still route through intermediaries that add cost and latency.

On the other hand, true A2A bypasses card networks entirely, which is where the cost and speed advantages actually come from.

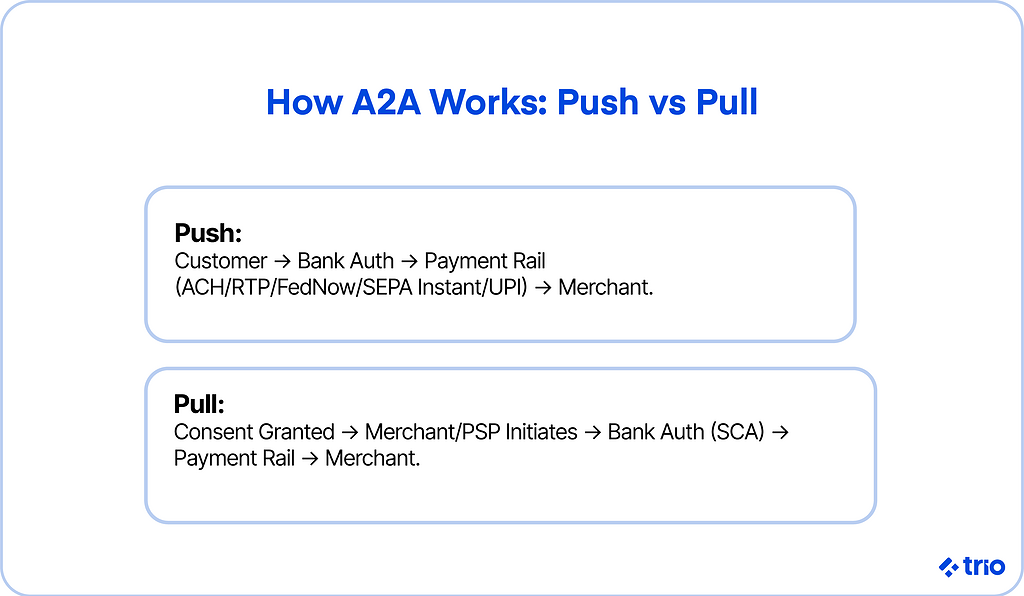

There are a couple of ways we have seen A2A transfers executed practically.

In some cases, the payer initiates payments directly from their bank account (a “push” payment). Think of a customer authorizing a one-off bank transfer for a large purchase.

Other times, the payee can pull funds from the payer’s account once permission has been granted. This is usually used in something closer to a subscription model or recurring bill, where taking the payment out of the user’s hands increases general efficiency.

Different types of A2A transfers, and the rails that they are built on, also allow payments to occur at different speeds.

What you might think of as traditional A2A transfers, like ACH in the United States, often take a couple of days to settle. Real-time payment schemes, which are gaining ground in regions like Europe and parts of Asia, promise near-instant transfers.

For decades, account-to-account transfers were little more than a background process: direct deposits, bill pay, ACH, all familiar, but hardly exciting.

A couple of things have happened recently that are causing these kinds of payments to gain momentum overall.

In markets like the EU and UK, adjustments to open banking rules have forced banks to expose APIs. This is making it easier for third parties to initiate secure transfers and has effectively lowered the barriers for fintechs and merchants to plug directly into bank rails.

Similar efforts are trickling into other regions, though the speed and enthusiasm vary, as is to be expected.

Payment schemes are rolling out faster than most businesses can keep up as well.

The U.S. now has FedNow alongside ACH and RTP.

India’s UPI has been an example for some time and has shown us all what’s possible when an entire population adopts instant A2A payments. They represent serious attempts to modernize money movement.

Even if the changes aren’t going to be drastic in Western markets any time soon, ignoring these technological developments is a sure way to put yourself behind.

Related Reading: Modernizing Core Banking Systems

Customers have gotten used to instant payment services.

They don’t see why a bank transfer should be any slower than a peer-to-peer app, and they’re less tolerant of hidden fees since they can jump ship at any moment in favor of a bunch of alternative options.

That impatience puts pressure on merchants to offer cheaper, faster options, or risk abandoned carts and lost trust.

The promise of lower costs and faster settlement only matters if you can point to real situations where it makes a difference.

There is a good reason why adoption is happening in areas where the pain of cards or slower bank rails is most apparent. Solving actual problems that users face is what’s most important.

Online retailers, especially those with thin margins, are drawn to A2A because it avoids interchange fees.

For a marketplace processing millions in monthly volume, shaving off even a fraction of a percent in fees can translate into meaningful savings.

Faster settlement also helps these platforms manage payouts to sellers without sitting on risk for days at a time. This, in turn, encourages the sellers to stay on the platform, resulting in more transactions overall.

Utilities, subscription services, tuition payments, and even mortgage installments are all scenarios where predictability is quite important.

If you can set up pull-based A2A transfers that don’t require any action on the user’s side beyond initial approval, you can reduce late payments and minimize administrative overhead.

You also provide customers with a greater sense of control than you would in something like card-on-file setups that may expire or fail.

From what we have seen, working with fintech companies all over the world, card penetration is quite uneven.

In markets like India or Brazil, A2A schemes are not just alternatives but the dominant rails for everyday transactions, which means that people don’t need cards at all.

If you already offer services in the U.S. or European countries, but are planning on expanding abroad, supporting A2A may not be optional.

Of course, the infrastructure to support A2A payments isn’t uniform either. While it may be rock solid in one country, it can also be frustratingly incomplete in the next.

Related Reading: Instant Cross-Border Payment Trends

It’s tempting to treat account-to-account payments like the perfect solution for dealing with clients who don’t have cards, and even improving legacy bank transfers.

As we have already alluded, the reality is more complicated.

A2A comes with clear advantages, but it also comes with an entirely new set of challenges that you are going to need to factor into your decision-making.

Deciding to accept account-to-account transfers requires you to consider a bunch of factors.

You need to think about what underlying rails may be available. And then, incorporating those payment rails into your payment strategy requires trade-offs and careful planning.

Related Reading: Real-Time Rail Modernizing the Canadian Payment System

Plugging into multiple bank and payment service provider APIs can get complicated. Each one speaks a slightly different dialect regarding direct debit and payment solutions.

Some follow open banking payments standards closely, others take liberties.

If your development team isn’t ready for that level of maintenance, you’ll need an orchestration layer or a provider that manages those inconsistencies.

Without a fintech expert to ensure you do this compliantly, this could expose you to a bunch of regulatory risks on top of the potential technical debt you would be piling onto your payment infrastructure.

Our developers have often helped clients clean up this mess, but it is far easier and less expensive to fix these issues proactively.

Even if the backend is flawless, the checkout flow can make or break adoption.

Customers asked to leave your site, log in to their online banking app, and complete multiple steps may abandon the process. And that’s even if all goes well and each system works perfectly.

That friction is especially costly in e-commerce, where conversion rates are already sensitive.

You need to test flows and simplify authentication to make A2A feel natural. We also recommend that you consider explaining your security measures or at least give your users some indication of those measures to encourage trust.

We’ve also seen that it can be helpful to include multiple payment options so that users can choose one that they may already be familiar with.

Lower chargeback risk doesn’t mean zero risk.

Fraudsters are creative, and regulators are watching the types of A2A payments being made.

In some regions, consent management and audit trails aren’t optional; they’re legal requirements. Ignoring them can cause bigger problems than the fees you were trying to avoid in the first place.

Users have always relied heavily on trust to make decisions regarding the financial institutions that they use, and the payment systems that they are happy to entrust their details to.

The reality is that what works in one market may flop in another. In Europe, customers are used to authorizing bank payments.

In the U.S., cards remain dominant, and persuading consumers to switch from this more traditional payment method may be difficult because of the amount of trust required.

Expanding into markets like Brazil or India, meanwhile, almost requires A2A because that’s how people already pay.

Doing your research and getting someone on your team who can provide additional insight into these nuances ahead of time can save both money and embarrassment.

In the U.S., card fees are a stubborn line item that merchants struggle to shake.

On average, interchange fees come to around 1.8% of each transaction.

However, when you factor in additional costs like processor markups or anything related to gateways and network assessments, your business might actually end up paying closer to 2–3% overall.

For high-ticket payments, or for a bunch of smaller payments where you might already not have made much, this can drag on margins even further.

Account-to-account (A2A) transfers cut out card networks entirely. That means no interchange, though there are still costs to consider, such as scheme fees, bank charges, and whatever you spend building or integrating the connections.

Even so, industry estimates suggest U.S. businesses that adopt A2A can reduce payment costs by 1–2 percentage points per transaction.

Let’s put that in practical terms.

If your company processes $50 million annually through cards at an effective cost of 1.8%, you’re spending about $900,000 a year to move money. Dropping that cost by a single percentage point could save around on direct debit transactions. $500,000.

And the ROI isn’t only financial.

Real-time rails like RTP and FedNow mean funds settle faster than ACH, which improves liquidity and working capital.

Fewer chargebacks also free up operational resources, and better access to the transaction data streamlines reconciliation processes.

All of this encourages vendors and buyers to use you rather than your competition.

The catch is that the break-even point isn’t universal. If you have low card volume or high development costs, A2A may take longer to justify.

The conversation around A2A isn’t standing still. A few signals suggest where it might be headed:

Account-to-account payments are becoming a real possibility in the U.S., thanks to the combination of new rails, regulatory shifts, and customer expectations. Taking advantage of the change could improve profitability.

Still, success depends on how you implement A2A.

If you’re weighing whether it fits into your strategy, getting experts on your team who understand the underlying technology and who can assist you with implementing these payments successfully is a strategic move.

Request a consult!

A2A payments are direct bank-to-bank transfers, meaning money moves directly between accounts without the involvement of card networks, allowing you to settle the payments faster and to avoid fees associated with cards.

Yes, A2A payments using real-time rails like RTP or FedNow can settle instantly, unlike ACH, which takes days. Issues with integration can lead to delays, as well as security risks, though.

Yes, A2A payments support pull-based models where businesses debit customer accounts for recurring services. This makes A2A payments ideal for subscriptions, tuition payments, or anything else that occurs on a recurrent basis.

A2A payments are safe because they rely on bank authentication and regulated rails, though fraud risks still exist and it is generally a good idea to get an expert on your team who can ensure integrations are secure and compliant.

Open banking APIs enable faster account verification for A2A payments by allowing third-party providers to verify a customer's bank account in real time, pulling balance and ownership data directly from the bank.