Hire by Technology

SERVICES

For many SaaS teams, the shift toward embedded finance feels complex, and they aren’t sure how to go about it. The challenge is that embedded payments aren’t just about adding a “Pay” button.

Instead, they touch licensing, risk management, underwriting, and customer experience all at once. Missteps here can slow your time-to-market or expose you to compliance risk, which can affect your customer relationships negatively and discourage future business.

The good news is that the tools and payment infrastructure have matured a lot in recent years.

You don’t need to become a bank to build a financial layer into your product. You just need to understand the basics of the embedded finance landscape and how to apply them to your business.

Our specialist fintech developers have worked with a variety of embedded financial services, including payment solutions.

View capabilities.

Before diving into embedded payments specifically, it helps to step back and understand the broader idea of embedded finance. Let’s take a look at what it actually is and how it works.

Embedded finance refers to the integration of financial services, like payments, lending, insurance, or card issuing, directly into non-financial software products.

The most common example of this is things like Stripe or Klarna, integrated into checkout.

Users don’t have to open a separate banking app or payment processor to finish their transaction. It’s all integrated directly into your app.

For SaaS providers, this shift has opened up new ways to create value by empowering customers through your payment services.

Under the surface, embedded finance depends on a network of APIs and partnerships that bridge regulated financial infrastructure with software platforms.

Banks hold the licenses and handle custody of funds, while fintech enablers provide compliant APIs, and SaaS providers integrate those APIs into their products, allowing them to take advantage of the services without needing to go through any licensing of their own.

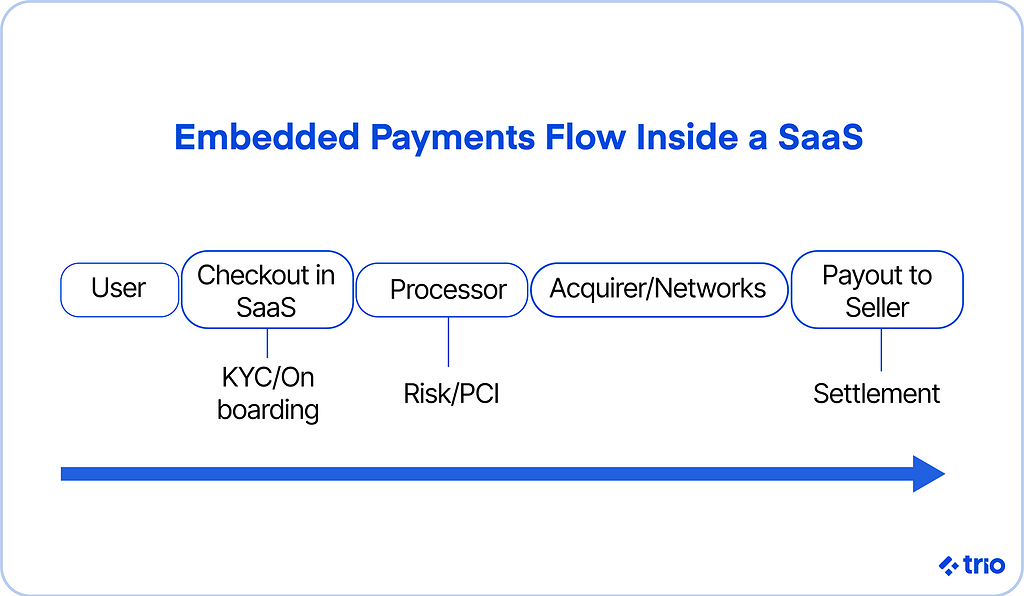

When a user initiates a payment or requests a card, the action moves through several layers.

The process starts on the app interface, moves through the payment processor, the acquiring bank, the card network, and sometimes even a sponsor bank.

Each step needs to be compliant with all relevant regulations and needs to keep user data secure.

Fortunately, you don’t need to build any of this. You just need to have a basic understanding of which layer of the stack you’ll own, and what someone else’s development responsibility is.

The embedded finance ecosystem typically involves three key players.

Banks and financial institutions provide the regulatory foundation and handle fund movement and compliance. This includes any KYC/AML processes.

Fintech infrastructure providers (like Stripe) act as intermediaries. These platforms offer APIs and SDKs that abstract away the complexity of financial systems.

Lastly, there are the SaaS platforms that integrate those capabilities, creating a tailored experience for their users.

The whole chain is beneficial to all players, so treating this as a partnership network rather than a vendor list tends to produce better outcomes.

Most SaaS platforms start out by redirecting users to a third-party processor at the point of payment. This could be something like a hosted Stripe page or external gateway.

It works, but the experience feels disjointed and can be frustrating, acting as a barrier that may discourage completion of the checkout process.

Users land on another brand mid-workflow. You lose visibility into the handoff. Any customization you want, branded receipts, in-platform reporting, and real-time balance updates require working around the processor rather than through it.

With embedded payments, the transaction happens inside your product.

You own the user interface in its entirety, giving you control over the entire experience. Your users never leave your platform, and you gain access to transaction-level data that can inform product decisions downstream.

The shift can also let you capture a portion of the processing fees rather than passing that revenue to a third party.

Our developers often utilize embedded payments to give non-fintech companies like SaaS platforms an entry point into embedded finance.

Now that you understand embedded finance as a whole, we can look at how embedded payments are payment capabilities built natively into a software platform.

Following the same principles from above, these capabilities allow users to send or receive money without leaving the product.

Think of a booking platform where service providers get paid directly through the app, or a B2B tool that lets companies pay invoices in a few clicks. The transactions are just a natural part of the workflow.

Integrating payments into your product isn’t a one-size-fits-all process. You will need to carefully consider what your existing tech stack is made up of and what you want to control.

If you just want a lightweight integration, you might use a white-label provider’s API to handle everything end-to-end. If you have a more mature platform and need a little bit more control, you might take on underwriting and sub-merchant management yourself.

The goal is to align integration depth with business goals.

There are several models for embedding payments. Each of these has trade-offs in control, compliance, and revenue share.

In our time in the industry, we’ve noticed that most non-fintech companies tend to land somewhere between the API model and PayFac-as-a-Service, depending on how quickly they need to ship and how much compliance overhead they can realistically absorb.

While the user experience might look simple, several layers make up a functioning embedded payment system, making the back end seem quite complex if you don’t know what you are doing.

Before merchants can accept payments, they need to be thoroughly vetted to ensure that they are a legitimate business.

This process, called underwriting, also assesses if they are compliant with financial regulations.

In an embedded model, your SaaS becomes part of this flow, often collecting business details and verifying identity through an API connection to a payment facilitator (PayFac) or sponsor bank.

The smoother you can get this process, the better it is for the overall customer experience.

This covers the technical core of the payment process and involves things like capturing payment details, authorizing transactions, routing funds, and settling payouts to the proper accounts.

Payment processors handle much of the heavy lifting on the technical side here, but your platform controls the flow and experience.

You might display transaction statuses or need to update account balances on the client interface.

Embedded payments bring you closer to financial data, which also brings you closer to risk and makes you liable for fines if regulatorybodies do not believe your systems are secure and compliant.

Chargebacks, fraud detection, PCI compliance, and dispute resolution all need to be accounted for.

Fintech partners can handle some of this, but you’ll still need visibility and governance to protect your brand and your users.

Our developers firmly believe that it is best to ensure transparency in your processes from the start. Integrating auditable reporting later is often more difficult and also more expensive.

Related Reading: Fintech Vendor Risk Management

We have already alluded to many of the benefits, like improving the experience of users, but there are many other reasons why you should consider embedding payments in your SaaS platform.

By facilitating payments directly, you can capture a portion of each transaction’s processing fees. That may sound minor, but at scale, even a small take rate translates into meaningful revenue.

A SaaS platform processing $10 million annually at a 3% blended fee might retain roughly 0.5% after interchange and provider split, generating $50,000 in new revenue without adding a single user. Many SaaS platforms evolve from flat subscription pricing toward hybrid models, where transaction-based income smooths out cash flow and fuels reinvestment.

When payments happen within your platform, you control every touchpoint from onboarding to settlement.

You also gain richer data about customer behavior, which can inform product design and help personalize future services.

Embedding payments lets users start transacting faster. They don’t have to create separate accounts with a third-party processor or navigate complex setup flows.

When done well, payment onboarding feels like a natural extension of signing up for your app, a subtle but powerful way to boost activation rates and early retention.

SaaS markets are crowded, and differentiation is hard to sustain. A built-in financial product can set your platform apart, especially in vertical SaaS, where payment flows often reflect niche workflows.

Once users start running revenue through your platform, churn drops naturally. Payment processing creates what’s sometimes called “stickiness by necessity,” but the best companies turn that necessity into value.

The principles of embedded finance apply across industries, but they show up differently depending on your vertical and customer needs. Let’s take a look at some of the most common instances that we come across.

Marketplaces are classic candidates for embedded payments.

You need to deal with payouts to the relevant party while dealing with platform fees. You can also automate escrow-like flows. The most important thing here is transparency to ensure all parties feel safe using your features.

Subscription-based SaaS products also benefit from built-in recurring billing and real-time reporting, with no third-party dashboards required.

In vertical markets, payment workflows tie directly to industry-specific processes. When it comes to HealthTech, PropTech, and EdTech, examples include patient billing, rent collection, and tuition payments, respectively.

Embedding payments directly into these systems simplifies compliance and reduces friction for end users.

It also opens doors to adjacent financial services like credit lines or insurance, further deepening user engagement. We often set up embedded payments with the flexibility to allow for this kind of expansion later.

If your software manages expenses or reimbursements, embedded finance can handle payouts at scale. Commissions might also fall into this category.

You can issue virtual cards and track spending in real time.

This not only improves user experience but can become a key selling point in procurement and finance departments, especially if you have added features like approval automation.

Accounting and ERP tools have a natural fit for embedded payments.

Allowing users to pay invoices, reconcile transactions, or manage vendor payments inside the same interface streamlines workflows and reduces manual errors.

The result is that traditionally passive systems are turned into active financial platforms.

As your embedded payment volume grows, so does its financial contribution to your business. Potentially, so do your expenses. This isn’t a big deal if you only handle a couple of hundred transactions, but most companies want to get to the stage where they handle millions.

Understanding how this volume translates into revenue and how to optimize it matters for long-term success.

Every transaction you facilitate generates a small fee. Typically, you would share this between you and your payment provider.

As your total processing volume increases, that share compounds.

Even if you have a relatively modest SaaS app processing $10 million annually, it could generate tens of thousands in new revenue through payments alone.

This income, and the opportunity for scalability that it provides, often makes it more attractive than subscription revenue because it grows directly with customer success.

Your take rate is the portion of payment fees you retain. Depending on your model, this could range from a few basis points to several percentage points.

Established SaaS Platforms have the luxury of negotiating favorable fee structures with payment partners.

Eventually, you could also start taking on more of the PayFac responsibilities yourself, which can significantly impact profitability. Higher margins often come with higher compliance overhead, so this trade-off deserves careful modeling before you commit.

Skilled fintech developers with a good understanding of compliance requirements can be a massive asset here.

Embedded payments can also improve cash flow visibility.

With direct settlement data, you can gain real-time insights into when money moves through your ecosystem.

For many of the clients that we have worked with, this information is invaluable, especially if you have the systems in place to route it into manageable dashboards or other parts of the analytics stack.

That transparency can help you forecast revenue and plan growth investments.

Building a smooth checkout experience is one thing; handling money on behalf of others is another entirely.

Financial compliance is the foundation of embedded payments, without which the whole system would likely fall apart.

Depending on your model, you may need to register as a Payment Facilitator (PayFac), operate under a Money Transmitter License (MTL), or partner with an entity that already holds these licenses.

All of these are viable options; you just need to consider what capabilities you have on your team or what you would be willing to augment your staff with long-term.

Regulations vary by region and by activity. Simply holding funds is going to have a different set of regulations than if you were facilitating cross-border payments or aggregating funds.

If you are not willing to keep fintech talent with this knowledge on your team indefinitely, you could partner with a regulated provider.

These providers can let you borrow their compliance framework while still offering an integrated experience.

Just remember that retrofitting compliance into an existing product tends to be far harder than designing it up front, so evaluating this early pays off.

Handling payments means handling sensitive financial data.

PCI DSS compliance, tokenization, encryption, and secure data storage are baseline requirements.

You also need to think about fraud management very early. Even legitimate users can trigger chargebacks through mistakes, while bad actors may try to exploit your onboarding flow for card testing or other abuse, even in your earliest stages.

Modern fraud detection tools use AI and machine learning to analyze massive quantities of data, and then use that data to identify and flag anomalies in real time. But they’re only as effective as your integration design, and you need clear escalation paths for your support team.

Every payment ecosystem faces disputes. Double charges and fraud are just scraping the surface. Even basic dissatisfaction can lead to disputes.

As the SaaS provider, you’ll often be the first line of contact, even if your partner handles the backend process.

Your reputation, and ultimately customer loyalty, depends less on avoiding disputes altogether and more on how you handle them.

You need to establish clear workflows for dispute resolution ahead of time. We recommend automating the notification process as much as possible.

The underlying API design plays a major role in making the payment process feel native to your app. Clean, modular integration helps you scale faster and experiment with new financial features over time.

Design and engineering teams tend to work best when they treat payments like any other core feature. Fintech experience makes this easy.

Now that you understand everything about embedded payment systems, here is a practical approach to integrating these systems into your own app.

You can use this step-by-step guide as a checklist to ensure that you have not forgotten anything.

Begin by mapping your current stack and identifying what capabilities you already have and what you’ll need to outsource.

Then, choose a partner that matches your scale, geographic reach, and compliance requirements.

Don’t just evaluate their documentation. The best way to prevent issues later is to assume that things will go wrong and to assess things like partner responsiveness ahead of time.

Sandbox tools can also be incredibly helpful.

Decide how money will move through your platform. Will users pay each other, or are you collecting on their behalf? Will you charge platform fees or markups?

These decisions define your flow of funds diagram, which partners and auditors will expect to see.

They also determine your monetization strategy, whether you earn a percentage of volume, a fixed markup, tiered fees based on user activity, or something else entirely.

Once the flow is defined, you’ll integrate your provider’s APIs or SDKs.

This is where having fintech-experienced developers on your team is incredibly beneficial.

These developers need to focus on modularity, separating the core payment logic from your app logic so you can swap providers or expand later without needing to overhaul major sections of code.

If you’re building in-house or customizing heavily, prioritize robust webhooks for event handling, for example, payment succeeded, payout delayed, dispute opened. They’ll save you countless support tickets later.

Before you go live, most providers require certification testing to confirm your integration handles edge cases correctly, refunds, partial captures, timeouts, and chargebacks.

This is where the sandbox environments we touched on earlier can be incredibly useful, as you can start the testing process without needing to go live.

Run these tests rigorously. Simulate real-world transaction volumes, latency spikes, and user behavior.

Once you’ve passed, roll out gradually with a pilot group before scaling to full production.

Most SaaS teams underestimate the complexity of fintech integrations and see the use of an embedded product as the easy way out. But, even though it is relatively simple in comparison to building your own system, it is still incredibly complex.

Payment data has to flow cleanly between your product, your provider, and your accounting systems.

Using event-driven architecture or a message queue prevents data drift and ensures payouts always match ledger records.

Another frequent pain point is UX consistency, especially if the payment provider’s hosted components don’t match your app’s design language.

Building lightweight custom wrappers around SDKs can keep the experience cohesive without sacrificing compliance.

For most SaaS teams, becoming a registered PayFac or licensed financial entity is overkill. That’s where PayFac-as-a-Service and Banking-as-a-Service (BaaS) platforms come in.

PayFac-as-a-Service providers offer a turnkey way to embed payments without taking on the full regulatory or operational load of becoming a PayFac yourself.

The important thing here is that you still control the user experience, but your provider manages everything that goes on in the background.

Essentially, you get the benefits of a PayFac model without any of the burdens that come along with it.

Building your own PayFac infrastructure is a multi-year project. Most small SaaS companies don’t have the time or the resources required to do this properly.

You’d need legal counsel, compliance officers, risk teams, and banking relationships before processing a single transaction.

PayFac-as-a-Service means all you need to do is integrate their APIs, and you instantly gain access to everything you need.

By leaning on a compliant provider, you can launch faster and focus on what differentiates your product rather than navigating regulatory paperwork.

All of that is for nought if you end up choosing the wrong provider, though, which is where having some experience on your team can help.

The right approach depends on how fast you need to ship and how much compliance risk you can realistically absorb.

The wrong choice of provider can lock you into a plan that will ultimately limit your growth. It is important that you assess potential payment providers thoroughly before making your decision.

When evaluating providers, make sure that you assess their:

Request references from similar SaaS platforms if at all possible. This is the best way to get insights that will be directly relevant to you.

Each major provider is slightly different, and thus slightly more suitable in certain circumstances:

The choice depends on your target market and technical maturity, not just pricing.

If you’re planning to expand internationally or layer additional financial features later, consider how each platform’s roadmap aligns with yours.

In general:

For many SaaS companies, a hybrid approach works best: start with a PayFac-as-a-Service partner, then gradually bring parts of the stack in-house as you scale.

The embedded finance landscape continues to evolve, like all other aspects of fintech. What works as a differentiator today may well become a best practice for most SaaS platforms in a couple of months.

SaaS 2.0 is defined by platforms that facilitate economic activity.

Credit issuance and transaction data are becoming core performance metrics alongside basic volume, ARR, and churn.

This means that the information you gather can be used as part of your long-term strategy.

Cross-border payments remain one of the hardest challenges in fintech. Differences in regulations and currency changes make the process incredibly complex, especially if you are trying to get payments done as quickly as possible.

However, new networks and partnerships, particularly in Europe, Asia, and LATAM, are closing these gaps, and it is always a good idea to plan for future expansion.

Embedded payments are no longer optional if you want to have a good chance at growing your SaaS platform.

But getting there requires some level of understanding of the fintech industry.

The complexity of building payment infrastructure correctly, especially in regulated verticals, tends to surface faster than teams expect.

Having engineers with genuine fintech means you can embed payments correctly from the start, preventing costly mistakes that lead to regulatory fines and even a loss in user trust.

Request a consult.