Hire by Technology

SERVICES

Hidden costs add 30–50% to fintech outsourcing contracts beyond headline rates. This can be incredibly detrimental to smaller firms with limited funding or to those who need to justify costs to investors.

The costs that push rates up most often include QA exclusions and financial-specific test cases, security review and penetration testing, compliance remediation after audit findings, DevOps and infrastructure setup, regulatory scope-change penalties, knowledge transfer and re-training overhead, and timezone-driven decision latency compounded over a full engagement.

These excluded factors are largely compliance-critical ones.

Let’s look at each in more detail, quantify what each typically costs, and describe how to check whether a proposal you are evaluating has excluded them.

At Trio, we specialize in fintech software development. When hiring our pre-vetted developers for outsourcing or staff augmentation, costs range between $40-$80 per hour, with no hidden fees.

Hidden costs exist in all software outsourcing.

The generic categories are well-documented: scope creep drives 20–30% budget overruns, rework rates average 27% on outsourced code, knowledge transfer costs 10–15% of total contract value, and timezone delays add 20% productivity overhead on offshore engagements.

Those figures apply to general software. However, in fintech software development, four structural characteristics amplify each one of these:

This is the most commonly excluded line item in fintech outsourcing proposals that our clients encounter, and arguably the most consequential.

A base proposal covers QA as a percentage of development time, usually 15–20% of developer hours. This covers functional testing: does the feature work as specified?

When the base contract's QA allocation is not enough, and these additional tests are unexpectedly required during security review or a compliance audit, two outcomes tend to follow.

Either the vendor charges an additional change order for extended testing scope (typically 15–25% of the development contract value for financial-specific test coverage), or the client hires a separate QA team to verify the work.

This latter option doubles the testing cost and adds 4–8 weeks to the timeline.

Proposal red flag: A QA allocation below 25% of total development time on a fintech project. Financial-specific QA, like idempotency, concurrent load, decimal precision, and ledger integrity, requires more time per feature than general functional testing.

This is the compliance-critical cost that appears in almost no base fintech development proposal.

Security best practices are described in proposals but rarely costed as a separate line item.

The penetration test fee ($12,000–$25,000, depending on scope), remediation engineering (typically 2–4 additional weeks of development work at full contract rates), delayed go-live, and potential SLA penalties if a banking partner's integration timeline has already been committed to, should all be considered.

As already mentioned, there is also a loss of income that you can factor in as well.

Proposal red flag: No line item for penetration testing, no QSA engagement, no mention of PCI DSS scope determination.

Compliance remediation is an exceptionally expensive hidden cost in fintech outsourcing, partly because it arrives after the engagement has ended.

This means that the vendor's engineers are off the project. Institutional knowledge of the codebase has dispersed. Remediation requires rebuilding context before beginning the fix.

A QSA engagement or regulatory examination identifies a finding in code that has been delivered by an outsourcing vendor, often 6–18 months after project completion.

Common findings that we have encountered include a logging configuration that captures card data in debug logs (PCI DSS violation), a KYC flow that stores a verified boolean rather than maintaining a stateful audit trail (AML examination finding), or a fraud detection model deployed without adequate documentation of the model's decision logic (a finding that matters under SR 11-7 and similar guidance).

Re-engaging the original vendor, if they are still available and willing, typically costs 15–25% of the original contract value just to remobilise the team and re-establish context.

If the vendor is unavailable or does not want to be contracted for this work, then a new engineering team's onboarding into code they didn't write adds another 10–15% of the remediation contract value before any actual fixing begins.

The cost and timeline of the remediation engineering itself depend on the severity.

A surface-level logging fix is a small patch, but remediating an architectural gap, like replacing a boolean flag with a properly stateful KYC audit trail, is a multi-week re-architecture that has to be done very carefully.

Regulatory examination delays further compound this.

If findings surface mid-examination, they can pause the process, generating additional examiner time charges and delaying approvals that the fintech may be depending on to move forward with licensing or a banking partnership.

Building compliance-correct architecture during development costs roughly 15–25% more than the shortcut. Remediating a compliance gap post-delivery consistently costs 100–200% of the original development cost for that component, plus the regulatory exposure cost on top.

Development proposals generally price developer time.

Any additional systems and technologies required to run the code are usually treated as the client’s responsibility, including cloud infrastructure, CI/CD pipelines, monitoring, alerting, secret management, and environment provisioning.

In some cases, we have also seen these listed as optional add-ons.

DevOps and infrastructure setup for a fintech product runs $15,000–$40,000, depending on complexity, cloud platform, and regulatory requirements, based on current market data from fintech DevOps specialists.

For products requiring multi-region deployment for GDPR data residency or financial data sovereignty, that range extends to $40,000–$80,000.

Growing fintech startups should budget $15,000–$30,000 annually for ongoing DevOps operations once the initial setup is complete.

Proposal red flag: No mention of cloud costs, CI/CD setup, monitoring infrastructure, or environment provisioning. Ask specifically and in writing: "Is DevOps setup included, and if so, what does it cover?"

Fixed-price contracts offer budget certainty when the scope is stable. But, due to the nature of the industry, the fintech scope is rarely stable.

Regulatory requirements surface during development that weren't visible during scoping, and each one triggers scope changes.

If a fintech startup contracts an outsourcing vendor for a payment integration on a fixed-price basis, but it is discovered that the product's user base includes customers in three EU jurisdictions, GDPR data residency requirements are triggered.

These need a regional database deployment, not in the original architecture.

The vendor's contract usually specifies that scope changes beyond 10% of the original contract value require a new statement of work.

Added regional deployment adds six weeks of engineering, which can be estimated at approximately 30% of the original contract value.

Often, the client did not budget for this because the regulatory discovery happened during execution.

In our experience, each regulatory scope-change event typically adds 15–40% to the original contract value on a fixed-price engagement.

Projects encountering two or three discovery events can reach 50–80% above the original quote before a single line of code has been changed for any reason related to features.

We always recommend that clients working with other partners allocate 10–15% of the total contract value to knowledge transfer and onboarding for generic outsourcing projects.

This is the industry baseline for structured transition costs.

In fintech, the actual figure runs higher because financial engineering knowledge is harder to transfer than general software knowledge. The compliance reasoning behind architectural decisions needs to be documented along with the code.

Fintech enterprises that outsource their core payments stack and then replaces its outsourced team may find a high percentage of engineering spend is going toward re-training rather than product delivery.

Each new cohort of developers required extensive onboarding on complex workflows, which slowed releases and increased defect rates.

The savings from lower hourly rates that were gained in the initial outsourcing agreement end up being consumed by the re-training costs of those rates generated.

An engineer joining a fintech codebase mid-engagement needs to understand not just the code but the compliance reasoning behind every significant architectural decision.

To do this, you need to document why the KYC state machine has this specific set of states, why the idempotency key is generated client-side rather than server-side, as well as how the PCI DSS scope boundary was drawn and which systems sit outside it.

Knowledge transfer costs significantly less when the engineering team is embedded in the client's team from the start, in a staff augmentation model, rather than managed separately under traditional project outsourcing.

In an embedded model, like the kind we offer at Trio, knowledge accumulates inside the client's team rather than the vendor's team. When an engineer leaves, the knowledge stays with the rest of the team and can be passed on to the new developer.

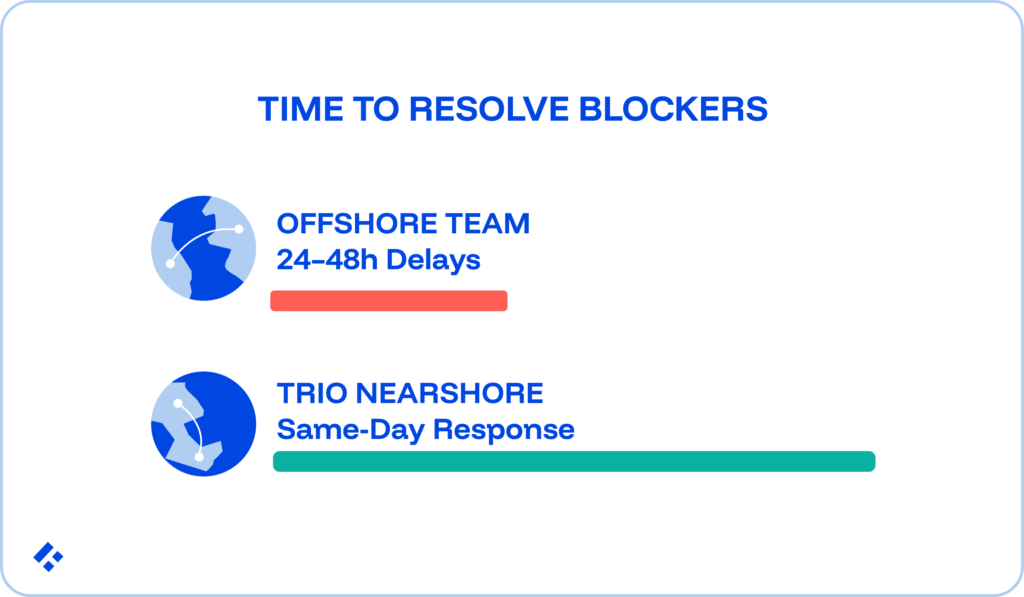

For offshore engagements with a 12-hour timezone gap, productivity overheads run higher than they would with in-house teams.

Each architectural question, code review request, or compliance clarification that arrives at the end of the day requires a 24-hour wait before a response can be actioned, and often another 24 hours before the implementation can be reviewed.

Compliance decisions delayed by timezone gaps can cause your fintech to miss deadlines that have external consequences.

A regulatory deadline that the team could have met with real-time collaboration becomes increasingly difficult to meet when every compliance clarification cycle takes 48 hours.

Even simple banking partner integrations that depend on cleared penetration test findings get pushed when remediation review takes two days per round instead of two hours.

LATAM nearshore engineers provide 4–8 hours of US working-hour overlap.

It is a valuable tool to take advantage of outsourcing’s cost-savings, while reducing effective decision latency from 24–48 hours to same-day responses.

At Trio's LATAM rates of $40–$80 per hour, the productivity overhead is substantially lower than at equivalent offshore rates once the timezone penalty is factored into the true hourly cost.

If you are evaluating a portfolio, the following table can guide you through the assessment process. The fintech-specific notes explain why each range runs higher than the general software baseline.

| Hidden Cost Category | Typical Range (% of contract) | Fintech-Specific Note |

| QA exclusions / financial-specific testing | +10–25% | Idempotency, ledger integrity, and decimal precision testing are not in the base QA allocation |

| Security review and penetration testing | +8–15% (or $15K–$50K absolute) | PCI DSS pen test $12K–$25K; scoping $3K–$8K; SOC 2 preparation additional |

| Compliance remediation (post-delivery risk) | +25–100% of affected component cost | Occurs 6–18 months post-delivery; re-engagement fee 15–25% of original contract |

| DevOps and infrastructure setup | +10–20% | Multi-region for GDPR/data residency adds an additional 10–15% |

| Regulatory scope-change penalties | +15–40% per discovery event | 2–3 events put the total 50–80% above the headline |

| Knowledge transfer and re-training | +10–15% (recurring per team change) | Higher in fintech due to compliance reasoning transfer, not just code transfer |

| Timezone-driven decision latency | +15–27% productivity overhead | Offshore 12-hour gap; LATAM 4–8 hour overlap significantly reduces this |

| Conservative hidden cost total | +30–50% on top of headline | Hiring expert fintech developers through staff augmentation can minimize these costs. |

Any proposal that lacks explicit treatment of these items is incomplete.

At Trio, our staff augmentation model prices differently from project outsourcing by design.

Senior fintech specialists with many years of production experience go for $40 to $80 per hour. These costs include the engineer's full productive capacity.

Since the engineer is embedded in your team rather than managed through a separate project structure, most of the hidden cost categories above either disappear or reduce significantly.

There are no change order mechanisms for regulatory scope changes, no re-engagement fees for compliance remediation, and no scope-change penalties built into the contract structure.