Hire by Technology

SERVICES

Stablecoins are processing trillions in transfers, and transaction volumes only seem to be increasing year-over-year.

The US GENIUS Act, signed July 18, 2025, established the first federal licensing framework for payment stablecoins and subjects issuers to Bank Secrecy Act obligations, mandatory sanctions compliance programs, and reserve requirements.

Its implementation rules are being finalized, with an effective date targeting January 2027.

On top of that, MiCA's crypto-asset service provider provisions became fully applicable in the EU on December 30, 2024, and the transitional period for legacy-registered firms expires July 1, 2026.

If your fintech is adding stablecoin payment capability, cross-border settlement, remittances, on-chain treasury, and merchant checkout, the biggest engineering challenge is building a regulated, scalable payment system that runs on on-chain rails.

This means OFAC screening before crediting a stablecoin receipt, Travel Rule data flowing alongside each transaction, custody architecture that meets institutional security standards, and stablecoin selection criteria grounded in reserve quality and regulatory standing.

The pool of engineers who can do all of this, who understand both the blockchain mechanics and the AML and KYC compliance layer, is narrow.

This guide maps the three vetting pillars for a stablecoin payment integration hire, with technical interview questions for each.

At Trio, we do all of the vetting on your behalf, so you can find the right people for your project in as little as 3-5 days, assessed by people who understand what the industry really requires.

A crypto generalist has probably built wallets, integrated web3 libraries, and understands ERC-20 token mechanics.

That background is very necessary, but not sufficient for a regulated stablecoin payment integration.

What separates the two is the regulatory compliance layer, which, in a fintech context, is engineered into the payment flow from the start.

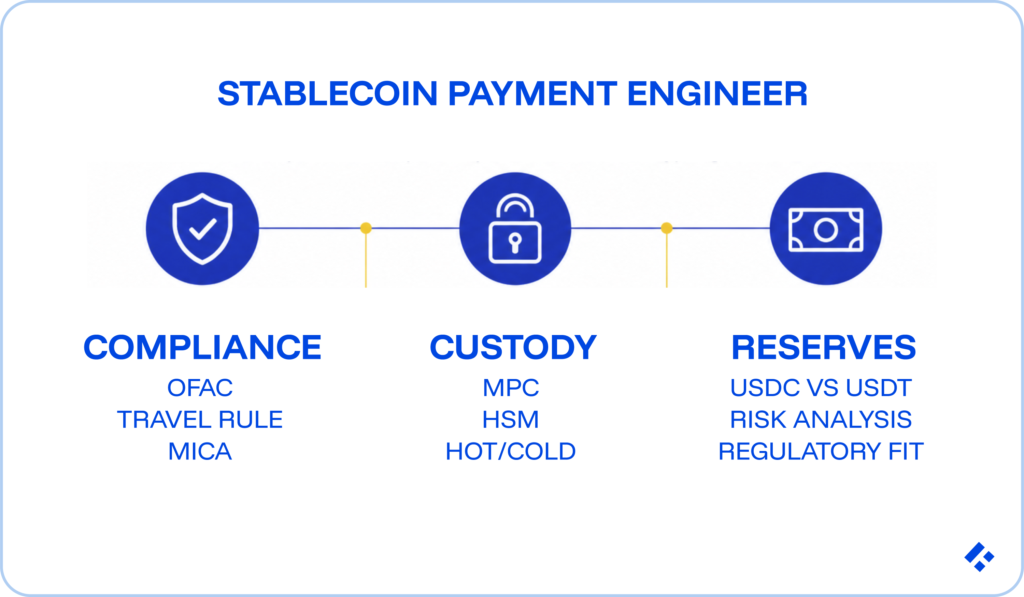

Three knowledge domains mark the line:

Let’s go into each of these in more detail.

There are several things a developer should know in order to ensure successful compliance integration when working with stablecoins.

The GENIUS Act establishes the first federal regulatory framework for payment stablecoins in the US, treating permitted payment stablecoin issuers (PPSIs) as financial institutions under the Bank Secrecy Act.

The framework mandates AML/CFT programs, mandatory sanctions compliance programs, customer due diligence, and, notably, the technological capability to block, freeze, burn, or prevent the transfer of stablecoins in response to lawful orders.

Engineers building payment integrations (not issuing stablecoins themselves) must treat compliance controls as design requirements, not feature additions.

Wallet screening, transaction monitoring, and sanctions checks at both send and receive need to be in the architecture from the start.

MiCA classifies fiat-backed stablecoins as e-money tokens. USDC (Circle, French EMI licence granted July 2024 by France's ACPR) and EURC are MiCA-authorized.

However, Tether did not seek MiCA authorization for USDT. Major EU venues, including Coinbase, Binance, Kraken, and Crypto.com, delisted USDT spot pairs for EEA users between December 2024 and March 2025.

MiCA's transitional period for legacy-registered service providers ends July 1, 2026, and your stablecoin selection should be partly a regulatory decision.

Your integration should also be designed for stablecoin substitution in case compliance status changes.

FATF's Travel Rule, extended to crypto transfers by the EU's Transfer of Funds Regulation, with application from December 30, 2024.

It requires the originator and beneficiary VASP information to accompany transfers above €1,000.

For US transfers, FinCEN's equivalent applies to amounts above $3,000. An engineer must know how to integrate a Travel Rule provider, Notabene, Sumsub, VerifyVASP, not just know the rule exists.

Overall, Travel Rule is a data-pipeline problem. The identifying information must flow alongside the on-chain transaction through off-chain messaging infrastructure, integrated into the payment flow.

OFAC sanctions screening for incoming stablecoin payments must happen before crediting the customer's account, not as a post-processing batch job.

This timing distinction is one of the most common gaps in generalist engineers' compliance architecture.

Two distinct screening problems also need separate handling:

These are different lists, updated on different schedules, and require separate query logic.

"Walk me through how you'd implement OFAC screening for incoming USDC payments. Where in the flow does screening happen, what happens when a payment arrives from a blacklisted address, and how do you distinguish between the Circle blacklist and the OFAC SDN list?"

A qualified answer covers screening before ledger credit, using a blockchain analytics provider for OFAC SDN screening, separately querying the USDC contract's blacklisted address mapping, handling the rejected payment by returning or freezing pending compliance review, and logging the event with sufficient detail for regulatory reporting.

Custody architecture is also quite complex when it comes to stablecoin integration, and can be split into several key knowledge sets that developers need to know.

A stablecoin payment integration holds funds in motion (a hot wallet, connected to the internet, for outbound payments and operational liquidity) and funds at rest (a cold wallet, offline or air-gapped, for reserves beyond the operational threshold).

The engineering decision is what percentage of total holdings stays in the hot wallet, and what signing threshold protects disbursements from it.

From what we have been able to observe, we have noted that institutional practice typically keeps the hot wallet holding enough for 24-48 hours of expected outflows, with everything above that in cold storage.

Multisig (multi-signature) requires M-of-N private key signatures to authorize a transaction; each key is a separate entity.

MPC (Multi-Party Computation) splits a single private key into shares distributed among parties, so no single party holds a complete key at any time. It’s become the modern institutional standard, and Fireblocks, Coinbase Prime, and Copper all use MPC.

Hardware Security Modules provide tamper-resistant key storage and signing operations for hot wallets.

An engineer building institutional stablecoin custody must understand HSM integration because most keys are generated and transactions signed inside the HSM.

Circle's CCTP burns USDC on the source chain and mints fresh, native USDC on the destination chain, currently supported across 12 chains.

This is the correct mechanism for cross-chain USDC movement.

An engineer building a multi-chain USDC integration who doesn't know CCTP is working with 2022-era knowledge.

"What's the difference between a multisig and an MPC wallet? In what scenario would you choose MPC over multisig for a regulated fintech's stablecoin custody solution, and what's the specific engineering reason?"

A qualified answer distinguishes the on-chain key shard exposure of multisig from the off-chain computation of MPC.

You’ll also want them to explain that MPC reduces the on-chain attack surface because no complete key or key fragment is ever broadcast, and note that MPC requires trust in the MPC provider's implementation.

Also consider if the developer acknowledges the CASP licensing implications of custodial architecture under MiCA.

There are three major components to reserve risk literacy at the present moment, although more may appear in the coming months.

Circle backs USDC 1:1 with cash and short-duration US Treasuries, held in segregated accounts.

Under the GENIUS Act framework, which requires 1:1 reserve backing in cash or permitted liquid assets, USDC's structure aligns well.

Circle's French EMI authorization under MiCA means USDC operates under both the US and EU regulatory frameworks. As of mid-2026, it's the only top-ten stablecoin with that dual status.

Tether's USDT offers deeper liquidity, particularly on Tron (TRC-20), making it dominant in certain remittance corridors and emerging market settlement applications.

Tether has improved reserve disclosure under regulatory pressure, but was historically less transparent than Circle. Tether also declined to seek MiCA authorization.

The CEO cited MiCA's requirement to hold 30%-60% of reserves in European bank deposits as incompatible with Tether's reserve model.

Major EU venues completed USDT delistings between December 2024 and March 2025, but it’s still viable with appropriate due diligence documentation.

An engineer building a stablecoin payment integration for a regulated fintech needs to treat stablecoin selection as a compliance and risk decision.

Artifacts need to include a documented stablecoin selection rationale covering reserve quality, regulatory standing across relevant jurisdictions, chain coverage, and risk profile, the kind of document a compliance officer can sign off on before the integration goes live.

"A compliance officer at a regulated EU fintech asks why you'd recommend USDC over USDT for the stablecoin payment integration. Walk me through the technical and regulatory reasoning."

A qualified answer covers MiCA compliance status, reserve transparency, chain coverage, and the concentration risk argument for supporting both stablecoins for resilience while designating USDC as primary for regulated flows.

Outside of the three pillar questions, you can use these additional six to determine whether an engineer has genuine production experience in stablecoin payment systems.

"How does a USDC transfer on Ethereum differ from a native ETH transfer at the protocol level, and why does this matter for payment reconciliation?"

Correct answer: ERC-20 transfers don't change the ETH balance returned by eth_getBalance. They emit a Transfer event in the token contract log.

A reconciliation system that monitors ETH balance changes misses every incoming USDC payment.

Production systems must subscribe to token contract Transfer events, filter by recipient address, and parse the log to extract amount and sender.

"How many block confirmations do you require before crediting a USDC payment on Ethereum, and how does this differ on Solana and Tron?"

Correct answer: Ethereum typically requires 12-32 confirmations for high-value payments (roughly 2.5-6 minutes).

Solana achieves near-instant finality (~400ms), typically requiring only 1 confirmation, and Tron requires 19-27 blocks (~60 seconds). An engineer who applies the same confirmation threshold across all chains hasn't operated cross-chain payment systems in production.

"Who pays Ethereum gas fees on outbound USDC payments, and how do you handle gas price spikes that make small stablecoin payments uneconomical?"

Correct answer: Gas is paid in ETH, not USDC. The sending wallet must hold ETH for gas. Under EIP-1559, the cost is a base fee plus priority tip, and can spike dramatically during high-network load.

For small payment amounts, gas can exceed the payment value itself, requiring either a minimum payment threshold, a gas sponsorship mechanism (EIP-4337 / account abstraction), or routing to a lower-cost chain, such as Solana, Base, or Polygon, for small-value flows.

"What happens to a USDC payment your system has already credited if the Ethereum block containing it is reorganised?"

Correct answer: The transaction becomes orphaned, removed from the canonical chain. The previously credited amount must be reversed or suspended pending re-confirmation.

Production systems watch for re-org events and implement a waiting period before final credit confirmation, or use a higher-confirmation threshold for irreversibility to reduce re-org exposure.

"How do you prevent crediting the same incoming USDC transaction twice if your payment webhook fires multiple times?"

Correct answer: The transaction hash (txHash) functions as the idempotency key, globally unique on a given chain. Before crediting, the system checks the database for the txHash. If present, the processing is skipped.

The idempotency check must happen atomically with the credit write within the same database transaction to prevent race conditions. This is the same write-ahead-log idempotency principle from traditional payment systems applied to on-chain transactions.

"A customer wants to send USDC from Ethereum to Solana for settlement. What's the correct mechanism, and what's the risk of using a bridge instead?"

Correct answer: Circle's CCTP is the correct mechanism. It burns USDC on Ethereum and mints native USDC on Solana with no wrapped token involved.

Bridges create a wrapped token (e.g., Wormhole-bridged USDC) that is not the canonical issuer's token and carries additional smart contract risk; bridge hacks have resulted in significant losses.

For a regulated fintech, CCTP is the only defensible mechanism. Wrapped-token bridges introduce counterparty risk that is difficult to justify in a compliance or audit context.

The LATAM fintech ecosystem produces engineers with genuine production stablecoin experience, driven by real consumer demand rather than academic interest.

The mechanism differs by country, but the result is similar in that engineers have built and operated stablecoin systems under pressure.

Argentina's high-inflation environment drove one of the world's highest stablecoin adoption rates. Companies like Lemon Cash, Bitex, and Belo built production stablecoin wallets and exchange infrastructure to serve this demand.

Mexico's story runs through Bitso, the country's first Bitcoin exchange, which built cross-border stablecoin remittance infrastructure on the US-Mexico corridor, the world's largest remittance market by volume.

Engineers who have worked on that infrastructure have built the kind of high-throughput, compliance-aware stablecoin payment systems that most US fintechs are still trying to build for the first time.

These engineers have shipped stablecoin wallets, exchanges, and remittance rails into production for users whose financial security depends on them working correctly.

At Trio, we place pre-vetted fintech engineers from LATAM with US and EU fintechs through staff augmentation, including engineers with stablecoin payment integration experience from Argentina's crypto ecosystem and Mexico's remittance infrastructure.

Trio's vetting for stablecoin integration roles covers compliance integration knowledge (GENIUS Act implications, MiCA stablecoin authorization status, Travel Rule implementation, OFAC screening architecture), custody architecture (MPC vs multisig trade-offs, HSM key management, hot/cold wallet split design), and reserve risk literacy (USDC vs USDT selection criteria for regulated integrations across jurisdictions).

We also focus on finding engineers with genuine production stablecoin experience, so you know that the person you are working with will have seen edge cases and the reality of stablecoin development expectations.

Placement can happen in as little as 3-5 days at rates of $40-$80/hr. You get the added benefit of full-day time-zone overlap with US teams from Colombia, as well as 4-8 hours of overlap for developers from Argentina and Mexico.