Hire by Technology

SERVICES

The more complex global finance becomes, the harder it is for organizations to keep up with ever-changing compliance expectations.

In order to address each effectively, it is important that you understand what actually separates AML from KYC compliance, and why that distinction matters for how you structure your program.

More often than teams expect, getting that answer wrong shapes everything downstream, especially how they hire, what technology they invest in, and where the gaps appear when a regulator starts asking questions.

The two terms get used interchangeably, and there is some degree of overlap. The distinction is that they cover different stages, different obligations, and different failure modes. Both paths have trade-offs.

In short, KYC runs at onboarding, before a customer ever transacts. AML takes over after that and monitors throughout the entire lifecycle.

Having a software developer on your team who is familiar with KYC and AML, and who understands how they can bake those controls into your software from the ground up, is essential to ensure the long-term success of your financial applications.

If you are ready to start hiring and want guaranteed fintech security experts through outsourcing or staff augmentation, talk to an expert.

Getting the distinction right starts with understanding what each framework covers on its own, before looking at where they connect. Let’s take a look at exactly what each term covers.

AML is short for anti-money laundering. It refers to the framework of laws and systems designed to stop money laundering and terrorist financing all around the world.

Financial institutions and fintech companies are required to run transaction monitoring, flag suspicious activity, and maintain detailed audit trails to help mitigate the risk of these crimes and identify unusual behavior before it becomes an issue.

The tricky part is that what might be considered unusual can look very different across markets, products, and customer types. A payment pattern that triggers an AML alert at a US retail bank might look entirely routine at a crypto exchange operating across multiple jurisdictions.

KYC, or Know Your Customer, covers the process of verifying who your customers really are.

To do this, you will usually start by collecting identity documents, running identity verification checks, validating addresses, and running customer due diligence (CDD) before any onboarding takes place.

That verification step forms the foundation that everything else gets built on, which makes it essential to get this right. If you cut corners here, your whole AML program starts on shaky ground.

Related Reading: Verification of Payee (VoP)

The clearest way for you to think of the difference between KYC and AML is to consider that KYC sits inside AML. It does not necessarily run alongside it, though.

AML functions as the broader regulatory framework. This means that it covers everything from transaction monitoring and suspicious activity reports (SARs) to sanctions screening and enhanced due diligence.

KYC is only one very specific process within that framework that is focused on identity verification at the start of the customer relationship.

Here is where they actually diverge:

Research suggests that around 70% of fraud takes place after KYC checks have already passed. This makes AML more essential than ever.

Several major regulators set the tone globally.

The Financial Action Task Force (FATF) publishes international AML standards. In the EU, the AMLD directives guide national AML and KYC frameworks. The FCA leads regulatory compliance in the UK, while FinCEN does so in the US, and MAS in Singapore.

While there are some small differences, most of these regulators now expect near real-time monitoring, clear escalation paths, and board-level accountability.

The sixth EU Anti-Money Laundering Directive (AMLD6), for instance, expanded criminal liability for AML failures to legal entities, not just individuals.

In the US, the Bank Secrecy Act (BSA) has governed AML compliance since 1970.

KYC requirements fall specifically under the Customer Identification Program (CIP) framework, introduced through the USA Patriot Act in 2001.

The Anti-Money Laundering Act of 2020 significantly expanded those BSA requirements, and in 2024, FinCEN issued a specific alert targeting deepfake fraud at financial institutions, a signal of how fast the threat landscape has shifted.

So, now that you understand the difference between KYC and AML, the practical question becomes how to actually manage each one in a fintech environment.

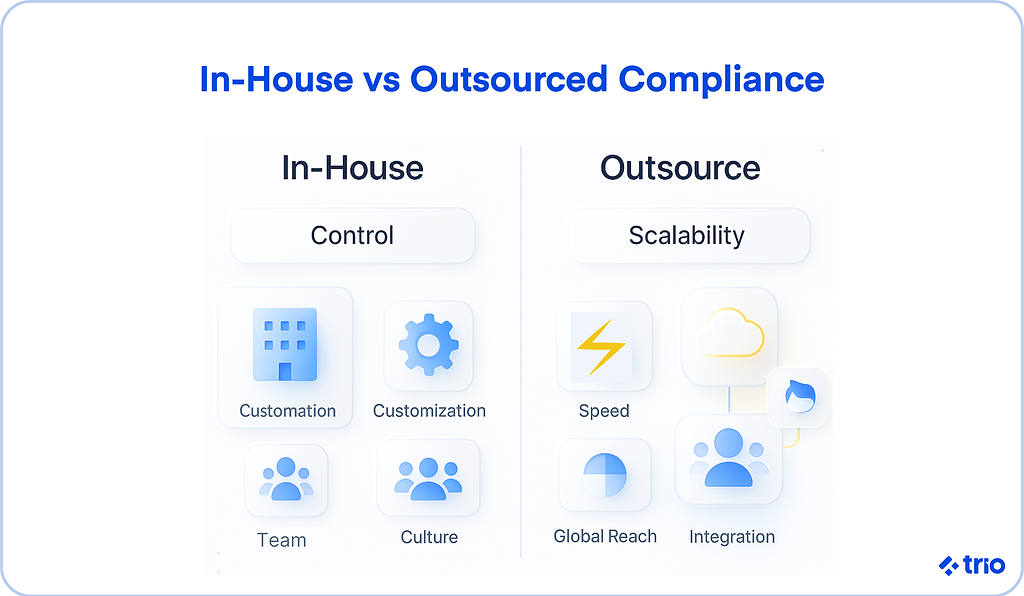

There are two primary options people consider. Compliance can either be managed internally, or you can consider outsourcing KYC and AML.

The reality is that there's no one-size-fits-all approach, and your choice depends on cost tolerance, risk appetite, and internal expertise.

This is one of the many reasons we insist on a consultation before helping our clients hire fintech developers.

Running compliance internally means developing your own policies, tech stack, and governance systems.

To do this, you'll need to hire analysts, legal experts, and system engineers who understand both finance and regulation. The overhead runs high, but it gives you full visibility into how AML alerts are generated and resolved.

This can be essential when auditors start asking questions.

If your financial institution handles very high-risk clients or operates across strict data jurisdictions, that level of control tends to justify the added overhead.

Outsourced AML and KYC models delegate some or all of your compliance functions to specialized third-party providers or RegTech platforms.

Partnering with third-party providers or RegTech platforms often means that you get access to tools like automated screening, AI-based risk scoring, and continuous regulatory updates.

All the pressure is taken off your shoulders to deliver, which re-energizes your internal team to work on other features.

The issue here is that most vendors integrate with your existing systems and workflows through APIs. You still need developers to make sure the integrations are secure and compliant. And you open yourself up to additional risks if the vendor has any issues on their side.

In-house compliance systems can work incredibly well, but you need to be aware of certain advantages and disadvantages before you start the hiring process to ensure that it's the best fit for your firm.

Faster policy adjustments and tighter customization often justify the overhead for organizations with complex or unusual compliance requirements.

An internal compliance team can fine-tune workflows for your specific products, adjust policies to match particular jurisdictions, and implement changes without waiting on a vendor to ship an update.

These added controls and customization tend to prove especially valuable when you are trying to stand out in a competitive market like fintech or when you are dealing with edge cases that do not map neatly onto off-the-shelf KYC solutions.

Hiring and training experts, paying for software licenses, and running internal audits add up, which often puts it beyond the capabilities of smaller fintechs.

Adapting to new AML regulations presents another recurring challenge. When AML rules change, internal teams often struggle to pivot quickly, especially if legacy systems are involved.

The same applies to scalability. If your customer base or transaction volume doubles, scaling manual reviews and due diligence checks can become a bottleneck.

Outsourcing offers efficiency and access to technology that many organizations can't justify building in-house. But it does shift some control out of your hands.

Cost savings and faster time-to-deployment are some of the biggest benefits, especially for smaller firms.

Vendors use the same technology to serve multiple clients, which means they can spread costs and offer AML compliance services at lower prices. Deployments are typically faster, too, weeks instead of months.

On top of that, these specialized providers have the resources to work with compliance experts who stay on top of new AML and KYC regulations.

Multi-market compliance also becomes significantly more manageable when you outsource for the same reason. The vendor takes on responsibility for maintaining local regulatory intelligence on your behalf.

Vendor lock-in can be a massive issue when you start growing. Switching later can be expensive or disruptive.

We always recommend that clients considering this option make sure to negotiate exit clauses before they sign.

This is always worth the extra effort, because the cost of changing providers mid-growth cycle almost always exceeds the cost of getting the contract terms right upfront.

Your customers' personal data may pass through other jurisdictions, raising data security and privacy concerns, so make sure to pay attention to GDPR and ISO standards.

Outsourcing also doesn't remove your responsibility. Regulators still hold the financial institution accountable, even if a third-party service fails, which means you are taking on any additional risks for yourself.

Whether internal or external, risk management forms the cornerstone of effective compliance.

Scalability has a way of testing every compliance model. If you have hired individual developers, then your internal teams get stretched thin. Sometimes, though, even external providers struggle to adapt to unique organizational needs.

Hiring experienced analysts can be quite tough, given how competitive fintech hiring has become. You are competing with major institutions for the same people.

If you hire someone without the industry experience or the necessary skills, then training them takes time, and you run an increased risk of them making mistakes.

As workloads grow, you may find your team buried under repetitive reviews or struggling to keep up with new AML requirements and KYC compliance expectations.

Bringing in outsourced support or staff augmentation at specific pressure points often makes more practical sense than trying to hire your way through every volume spike.

This is especially viable when you partner with a firm like Trio, with fintech specialists on hand, vetting all potential candidates to ensure they are a good fit for your project.

A well-matched RegTech partner can quickly scale operations for new markets or regulatory jurisdictions.

That flexibility can be incredibly beneficial for fintechs and financial institutions that move fast or operate across global footprints.

Modern compliance technology relies heavily on cloud-based platforms and real-time APIs.

These tools streamline workflows across client onboarding and compliance functions, including sanctions list screening and customer due diligence.

When systems communicate seamlessly, scaling up becomes far less painful.

Over time, many organizations that we have worked with find balance in a hybrid approach.

Policy oversight and key risk decisions stay internal, while third-party tools handle automation and volume-heavy AML checks.

We often help clients set up this model, sometimes adding developers to their team through staff augmentation to bridge the gap between what their existing compliance infrastructure handles and what the business actually demands at scale.

Before landing on a direction, start with a few honest questions.

What's your transaction volume and customer risk level? How complex are your AML and KYC regulatory obligations across markets? Do you have the internal expertise to run an AML compliance program efficiently?

As we have already mentioned, smaller institutions are probably going to find outsourced AML services the most practical, while established ones often prefer direct oversight.

Realistically, you are probably going to end up combining both, internal governance backed by external automation.

Regular performance reviews also tend to produce the best balance between control and flexibility. The organizations we have seen struggle most make this decision once and never revisit it as their transaction volumes and regulatory exposure grow.

The industry is always changing, but there are a couple of things that we can already see coming up, which are unlikely to halt.

These trends include using AI and machine learning to recognize transaction anomalies and spot patterns humans might miss.

We are also seeing an increase in regulators expecting ongoing risk assessments that adapt to behavior in real time.

Blockchain is also being used more frequently, and is showing potential for identity verification, with distributed ledgers potentially allowing customers to share verified credentials across financial services institutions without repeating KYC checks at every step.

On the enforcement side, there's growing cooperation between regulators, especially in the EU.

We are also seeing even massive companies getting fined for failure to comply with KYC/AML regulations.

Understanding the difference between AML and KYC compliance shapes more than terminology. It affects how you staff your team, what technology you buy, and how you respond when something goes wrong.

The real goal worth working toward involves building a compliance structure that scales with your growth, adapts to changing AML regulations and KYC requirements, and quietly does its job, protecting your customers and your reputation.

If you need fintech software developers who are familiar with all the intricacies of AML and KYC compliance processes, we can connect you with our experts through outsourcing or staff augmentation.

Book a security-ready consult.